Weak US Drilling Activity To Weigh Heavily On Baker Hughes’ 3Q Earnings

Oilfield services major, Baker Hughes (NYSE:BHI), which is working with Halliburton (NYSE:HAL) to complete their proposed merger by the end of the year, faced another rough quarter due to the weak North American drilling demand. The Houston-based oilfield service contractor is likely to witness a sizeable decline in its revenue as the oil companies continue to hold back their exploration and production activities amid depressed crude oil prices. Further, we expect the world’s third largest oilfield services contractor’s earnings to experience a sharp fall both sequentially and annually driven by its large exposure to the US drilling markets, and unfavorable pricing environment suffered by the company. We take a quick look at the key trends which we expect to see in Baker Hughes’ third quarter results, which is due to be released on the 21st of October 2015. [1]

See Our Complete Analysis For Baker Hughes Here

Lower North American Drilling Activity To Drag Down Baker Hughes Revenues

- Fed Rate Hike Causes Oil Prices To Hit Their Lowest Level For The Year

- Baker Hughes Exceeds 1Q’17 Earnings Expectations; Continues To Focus On Product Innovation

- Baker Hughes To Report A Subdued Recovery In 1Q’17 Compared To Its Peers

- Baker Hughes Is On The Path To Recovery, Despite Weak 4Q’16 Earnings

- Baker Hughes’ Fourth Quarter Earnings To Witness A Rise Driven By An Improvement In Oil Prices

- Baker Hughes’ 2016 In Review: Halliburton’s Loss Is GE’s Gain

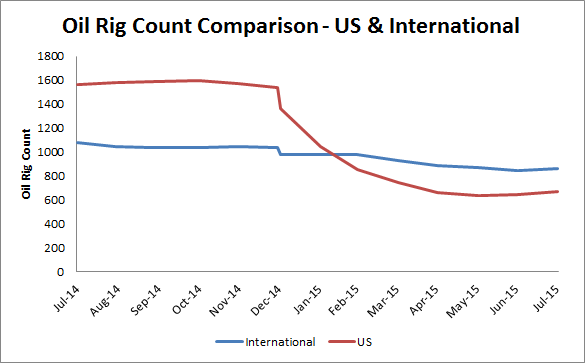

Just like Halliburton, Baker Hughes, too, generates more than half of its revenues from its North American operations. However, in the wake of plummeting crude oil prices, large US oil and gas companies continue to restrict their upstream capital spending, leading to a sharp decline in the demand for drilling services in the region. This is visible from the significant reduction in the rig count globally, particularly in North America. The US oil rig count, one of the closely watched metrics in the industry, stood at 640 units at the end of the September quarter, representing a decline of almost 60% since the beginning of the year [2]. Thus, given Baker Hughes’ large exposure in the US drilling market, which has seen a drastic fall in drilling activity, we foresee a notable drop in the company’s top line in the current quarter. On the other hand, the international drilling markets have remained resilient despite the falling crude oil prices due to their lower break-even costs. The international oil rig count has declined by only 16% since the start of the year, which is roughly one-third of the decline in the US oil rig count. However, this may not be sufficient to soften the blow of the weaker North American drilling demand on Baker Hughes’s revenue.

Source: Baker Hughes Rig Count Data

Merger Might Get Pushed To 2016

While both Baker Hughes and Halliburton have been committed towards completing the proposed merger within this year, they are facing a number of hurdles from the anti-trust authorities. To overcome the regulatory issues, the two companies plan to sell assets worth $5.2 billion before the deadline to complete the merger. Baker Hughes has announced the sale of its core completions business (packers, flow control tools, and subsurface safety systems), its sand control business in the Gulf of Mexico, and its offshore cementing businesses in Australia, Brazil, the Gulf of Mexico, Norway, and the UK, while Halliburton will divest its expandable liner hangers business, in addition to its drill bits and drilling services business worth $7.5 billion. However, the companies have not reached an agreement with any of the regulators regarding the adequacy of these divestures. Furthermore, the two companies have pushed the deadline for the US Department of Justice’s (DOJ) antitrust review to 15th December from the previous deadline of 25th November. This implies that the merger will not be complete before mid December and there are chances that the merger closure is extended to early 2016.

Source: Barclays CEO Energy-Power Conference, September 2015

New Product Offering To Improve Future Performance

Despite the challenges faced by its merger with Halliburton, Baker Hughes has been working towards improving its product offering as an insurance in case the merger does not pass through. The company announced a new product or segment called DeclineShift, which is a consulting and optimization execution service. This service will be used to improve the performance of those assets that are experiencing a decline in production, rise in operating costs, or a combination of both. At a time when the oil prices are in a free fall, large Exploration and Production (E&P) companies are looking for services that can improve their performance while maximizing their capital efficiency. Consequently, the company’s new product offering is likely to attract more customers, which can add to the company’s declining top line. In addition, the new product will be a high margin business for Baker Hughes as the oilfield contractor will be able to use the experience of its workforce to offer a value-added service to its customers. Thus, this will be a win-win situation for Baker Hughes as well as its customers. However, we will have to wait and watch if this new stream of income would be enough to offset the negative impact of the sluggish drilling demand on Baker Hughes’ earnings.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes: