Crude Oil Oversupply, Soft Margins Are Likely To Weigh on Exxon’s Profits In The Near Future

Exxon Mobil (XOM): Exxon Mobil is a multinational oil major that specializes in upstream operations, downstream operations, and chemicals. Exxon’s results for the first quarter were weaker than expected due to poor margins for its refining and chemical segments. Revenue came in at $63 billion this (down 6.7% from a year ago) while earnings came in at $2.35 billion (less that half the figure a year ago). The oil major has been struggling over recent months as the price of chemical and downstream products were softer than the same quarter last year. Per Trefis estimates, Exxon Mobil’s shares have a fair value of $84, which is 10% higher than the market price. You can view our interactive dashboard – Exxon’s 2019 Q1 Results and Outlook for 2019 – and modify the key drivers to understand their impact on the company’s valuation. Also, you can also find more of our Energy sector data here

What are the company’s various segments, and what were the key takeaways for the quarter?

Upstream segment:

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

- Down 9% Since The Beginning of 2023, What Should You Expect From Exxon Mobil Stock?

- Will Exxon Mobil Stock Trade Higher Post Q2?

- What’s Happening With Exxon Mobil Stock?

- Exxon Mobil Stock Likely To Trade Lower Post Q4

- What To Expect From Exxon Mobil’s Stock Post Q2?

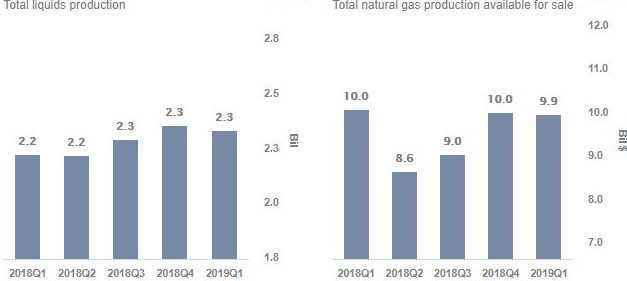

Crude oil production by Exxon Mobil’s Upstream segment was steady in Q1 2019, while natural gas production increased for the quarter. But revenues were hurt by a lower realized price. The company plans to increase output vis-a-vis its Permian and Bakken production to 1 MBOED by 2024. This implies an 80% increase in production from current levels, and will mitigate the issue of declining crude oil production for the company over recent quarters. The company faced slightly lower crude prices in Q1, but the impact of this on the top line was partially mitigated by higher natural gas prices. Our yearly outlook for the average realized price of crude oil is $60 and for natural gas is $2.8.

Downstream segment:

With the price of global composite Platts 3-2-1 falling to $6.8 in Q1 2019 from $10 in Q1 2018, margins for the downstream segment were considerably squeezed in the latest quarter. Given the oversupply in the global market, especially in Europe, we don’t expect a recovery in refinery product prices during the next few quarters.

Chemical segment:

Profits for the Chemical segment fell significantly due to softer demand from the automobile market. Additionally, a strengthening U.S. dollar also had a notable negative impact on the segment’s bottom line.

Capital Expenditure and Free Cash Flow:

Capital and exploration expenses increased from $4.87 billion a year ago to $6.89 billion this year. This coupled with weak operating figures weighed on the free cash flow and dragged it down to $2.5 billion in Q1 2019 from $6.7 billion a year ago.

What is our outlook for revenue, net income, and EPS for Exxon in 2019?

Exxon will have to contend with lower crude oil volume in the short term. This combined with issues of softer margins in the Downstream segment means that revenue and earnings for the year will be lower than that for 2018. While we believe that revenues for the Chemical segment revenue will not decline further, we also don’t expect much of a recovery. We expect full-year revenues to come in at around $34 billion, and net income to be roughly $18.5 billion. This would translate into an earnings per share of $4.21 for the year.