Oracle Q3: Cloud Continues To Surprise

Oracle (NYSE:ORCL) reported its fiscal Q3 results on Thursday, March 14. The company beat expectations on revenue and EPS, driven by traction in cloud. We note that excluding FX, the net growth for Oracle continues to hover around 3-4%. While the size of the company’s revenue base and lower market share versus the larger public cloud vendors is likely to require a few quarters before the intended churn in revenue quality comes about, if the net growth does not start accelerating beyond the current low single digits within 2019 (as claimed by Larry Ellison), investor excitement could begin to wane.

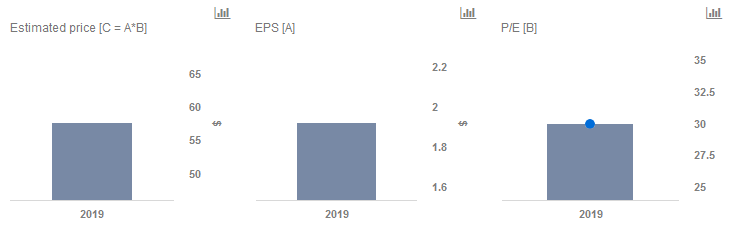

We have a price estimate of $58 per share for Oracle, which is around 15% higher than the current market price. Our interactive dashboard on Oracle’s Price Estimate outlines our forecasts and estimates for the company. You can modify any of the key drivers to visualize the impact of changes on its valuation, and see all of our technology company data here.

Key takeaways from Q3 include:

- Cloud services and license support: Revenue increased to $6.66 billion (+1% y-o-y) and was impacted by 3% by currency headwinds.

- Cloud license and on‐premise license: Revenue decreased to $1.25 billion (-4% y-o-y) and was impacted by 4% by currency headwinds.

- Hardware: Revenue decreased to $915 million (-8% y-o-y) and was impacted by 4% by currency headwinds.

- Services: Revenue decreased to $786 million (-1% y-o-y) and was impacted by 4% by currency headwinds.

- Total revenue decreased to $9.6 billion (-1% y-o-y) and was impacted by 4% by currency headwinds, and non-GAAP operating margin grew to 44% (+100 bps y-o-y).

- Quarterly dividend was increased 26% from $0.19 per share to $0.24 per share.

The company’s management continues to expect that currency will likely be a headwind to the extent of 3% in Q4. Accordingly, management has guided for the following for Q4:

- Revenue growth of 0% to -2%, y-o-y

- Non-GAAP EPS of $1.05 – 1.09 (+12%-16% y-o-y)

While the total revenue remained flat, the improvement in margins seems to support management’s commentary of growth in the higher-margin autonomous database and in Gen 2 cloud, offsetting declines in legacy products. Furthermore, 20% of its Autonomous Database customers as net additions and 4,000 active trials paint an encouraging picture from a traction perspective.

Going forward, the company believes that its leadership position in database is likely to help accelerate the adoption of its cloud with tailwinds from the productivity, compatibility and cost advantages that Oracle’s products offer.

Do not agree with our forecast? Create your own price forecast for Oracle by changing the base inputs (blue dots) on our interactive dashboard.

Like our charts? Explore example interactive dashboards and create your own.