As Lululemon Repositions Will It Be Able To Justify Valuations?

Lululemon’s (NASDAQ:LULU) most recent quarter was quite impressive. It saw revenues surge 25%. Providing evidence that the company’s re-positioning its omni-channel model, by enhancing its merchandising and digital footprint, has started to show signs of paying off. But will this shift be enough to justify its current valuation? Lululemon currently trades at a valuation of ~53 P/E and a forward P/E of 38.

We currently have a price estimate of $90 per share, which is 30% lower than the market price. You can use our interactive dashboard Can Lululemon Justify Valuations? to modify key drivers and visualize the impact on Lululemon’s price estimate.

- Lululemon’s Stock Down 34% YTD, What’s Happening?

- Down 9% This Year, What’s Next For Lululemon’s Stock Past Q4 Results?

- Lululemon Stock Up 52% In Past Year. What Should You Expect Now?

- Will Lululemon Stock Trade Higher Post Q2?

- Will Lululemon Stock See Higher Levels Post Q1?

- Earnings Beat In The Cards For Lululemon Stock?

In the first part of its strategy Lululemon, over the past couple of quarters, (much like its competitors), has been increasingly shifting into the e-commerce space. This shift resulted in e-commerce sales surging by 48% in the quarter . Lululemon has also increasingly focused on the athleisure space in recent times, this goes hand-in-hand with its overall strategy.

Lululemon has also increasingly used social media as a key platform to promote its brand. Allowing itself to re-position to serve Millennials, which it believes will drive its sales in the coming years. Platforms like Instagram and Twitter have been key as it partners on these platforms, with those it believes can help correctly position its brand.

Merchandising has also been a key part of this re-positioning strategy. With traditional athletic apparel in decline, Lululemon has decided to focus on the athleisure space. With the industry being worth $44 billion, Lululemon believes it can be the key driver as it looks to increase sales to $4 billion by 2020.

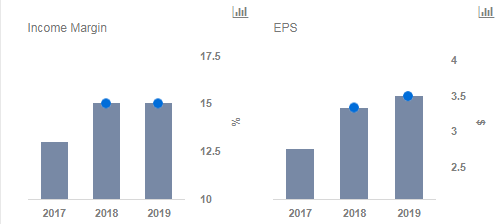

This focus has allowed Lululemon to position its brand, and therefore pricing strategy, correctly as well. Moving away from increasingly relying on discounts in the past to the current trend that allows it to be a premier brand in the market, and therefore price products much more in line with its overall brand image. This, in recent times, has paid off with margins increasing and profits almost doubling.

The coming quarters will determine whether valuations are in line with the company’s earnings. Should Lululemon execute its strategy to consolidate its brand image, correctly position its sales strategy, and successfully maintain its market position in the athleisure space, it should be able to continue the momentum it has achieved in recent quarters.

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.