Is United Airlines’ Balance Sheet Strong Enough To Withstand Covid-19 Headwinds?

United Airlines’ (NYSE:UAL) operations are on a standstill as the Covid-19 pandemic continues to run its course. The company’s stock dropped 70% this year, and it posted a massive $1.7 billion loss in the first quarter. The company expects to burn nearly $40-$45 million per day in Q2 2020, implying that it will need significant liquidity as it rides out the pandemic. For investors, the key question is – Can United Airlines’ stock recover? It will depend on what trajectory the demand follows and how investors’ risk perception and future growth expectations change.

We consider two demand recovery scenarios and assess how well prepared United is from a liquidity perspective. In other words, does it have enough cash to stay afloat until the demand bounces back? We find that in a pessimistic case, United will post a huge annual loss of exceeding $5 billion – implying cash outflow of nearly $2.6 billion even if it cuts its capital expenditures by 70% and doesn’t spend any money on share repurchases or dividends. Luckily, the company has a cash cushion to absorb this outflow. Our dashboard Does United Airlines Holdings Have Enough Liquidity To Survive Covid-19 Demand Shock examines the company’s cash flow generation ability and financing requirements under two different demand recovery scenarios.

- Spurred By Stellar Earnings, Can United Airlines Holdings Stock Extend Its Run?

- United Airlines Holdings Stock Looks Set For A Come Back

- Down 13% Last Week, Can United Airlines Holdings Stock Bounce Back?

- Is United Airlines Stock On The Move?

- Company Of The Day: United Airlines

- Will United Airlines Stock Rise After Recent Correction?

Scenario One: Demand Recovery Is Spread Across Q3 And Q4

Consider a scenario where the demand shock experienced by the travel industry completely fades away by the fourth quarter of this year, and United Airlines starts flying most of its routes. In this scenario, we assume a revenue decline of 30% and a 50% cut in capital expenditures in 2020. We also assume that United will not repurchase any shares. While the net loss could be around $1.9 billion on a revenue base of almost $30 billion, United Airlines’ net cash outflow for the year will be just over $200 million if it can cut its capital expenditure in half to $2.3 billion.

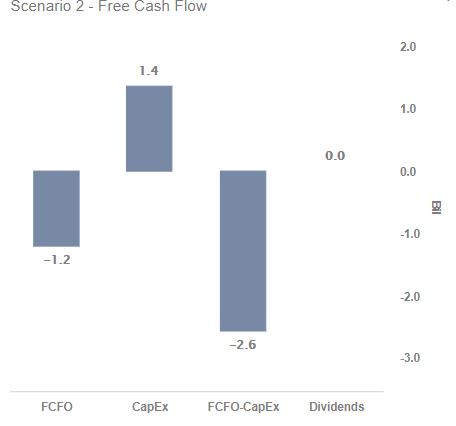

Scenario Two: Demand Recovery Incomplete With Non-Essential Travel And Discretionary Spend Pullback

Here is a more worrying scenario. Even if the pandemic is reined in by Q4 – allowing airlines to operate, there is a good chance that consumers will pull back their discretionary spending and avoid non-essential travel. Businesses are also undergoing a significant shift in how they collaborate and operate, and some of those structural changes are likely to persist and impact business travel as well. In this scenario, we assume a 50% decline in revenue and calculate that United will require additional financing of nearly $2.6 billion if it were to stay afloat, given its cost structure – even after cutting its capital expenditure by 70% to a mere $1.4 billion. United’s high fixed-cost structure makes it vulnerable to demand fluctuations.

The silver lining is that United’s current cash cushion can absorb this cash outflow. At the end of March 2020, the company’s cash and cash equivalents stood at roughly $3.4 billion. In addition, United Airlines has secured nearly $3.5 billion in government grants and $1.5 billion in a low-interest loan to address its cash burn.

While United Airlines could face a significant cash outflow, Southwest Airlines is in a much better position to weather the storm.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams