How Does Oracle Look Post-Q2 Results?

Oracle (NYSE:ORCL) reported its fiscal Q2 results on December 17, beating market expectations on revenue and EPS. Despite the impact of forex headwinds, Oracle’s results point towards potential acceleration, and the company’s management continued to exude confidence about its full-year revenue growth exceeding that of the previous fiscal year. The database giant’s Q2 results seem to have ignited hopes of its cloud momentum picking up steam going forward.

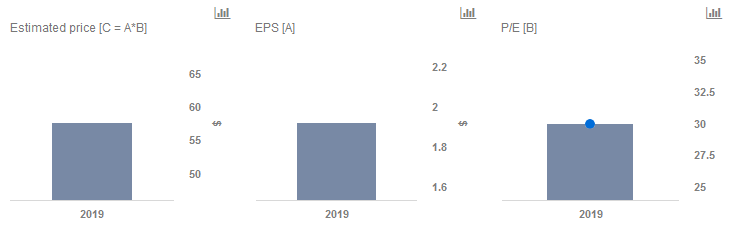

We maintain our price estimate of $58 per share for Oracle, which is around 20% higher than the current market price. Our interactive dashboard on Oracle’s Price Estimate outlines our forecasts and estimates for the company. You can modify any of the key drivers to visualize the impact of changes on its valuation.

Oracle registered its seventh consecutive quarter of double-digit EPS growth, with non-GAAP EPS of $0.80 (+19%y-o-y). The company reported total Q2 revenue of $9.56 billion, which was flat year-over-year, or up about 2% on a constant currency basis. Oracle noted that ERP and HCM have reached annualized revenues of $2.6 billion, representing annual growth of over 20%.

How Is The Cloud Business Progressing?

In terms of traction, Oracle saw nearly 200 of its ERP customers move to the cloud. On the autonomous database, the company is witnessing over a thousand trial activations per month. The company claims to have a 50% share of the database market and aims to migrate all Oracle database customers to the Oracle cloud, while expanding its share of the database market. The company’s previous lack of sufficient cloud infrastructure to support its industry-leading database technology appeared to have been holding it back. However, with the Gen 2 Cloud, Oracle now has the tools to not only compete but also win in the market. As an anecdotal example, the company notes that it takes around 15 minutes to have the Oracle cloud up and running versus the traditional timeline of 15 days. Furthermore, the company believes that the uptake towards Oracle Database and Oracle Public is likely to accelerated from the next fiscal year.

The company’s Q2 results, Q3 revenue guidance of 2-4% y-o-y growth, traction in cloud and autonomous database uptake point towards Oracle positioning itself for steady growth moving forward. However, it will be important to continue looking for incremental data points around traction to ensure that the current quarter was indeed the start of an acceleration towards a much larger cloud presence.

Do not agree with our forecast? Create your own price forecast for Oracle by changing the base inputs (blue dots) on our interactive dashboard.

Like our charts? Explore example interactive dashboards and create your own.