What To Expect From Oracle’s Q2 Results

Ever since Amazon publicly announced that it will be moving off of Oracle‘s (NYSE:ORCL) databases moving forward, there has been some negative sentiment surrounding the company. Oracle’s business is largely expected to show some signs of peaking out when the company reports its Q2 earnings on December 17 after market close. Given the modest expectations, any positive surprise on the back of Oracle’s cloud architecture could provide some upside.

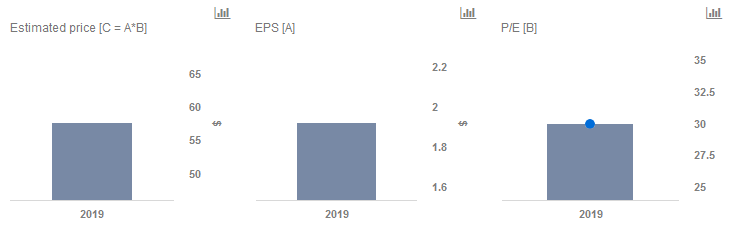

We currently have a price estimate of $58 per share for Oracle, which is around 20% higher than the current market price. Our interactive dashboard on Oracle’s Price Estimate outlines our forecasts and estimates for the company. You can modify any of the key drivers to visualize the impact of changes on its valuation.

In November, we discussed the company’s Gen 2 Cloud and management’s expectations of Gen 2 beating the competition by way of superior price and performance. Earlier this year, some experts had opined that Gen 2 may still be a skeletal structure which needed more refinement to become a commercial-grade platform. It will be interesting to hear Oracle’s commentary around traction in the cloud business given management’s prior claims. In addition to the uptake of Oracle’s cloud, we will be looking at tax benefits and cost control contributing to earnings. Further, we will be watching for the impact of forex and color on how the core database business has been benefiting from the introduction of Oracle’s own cloud.

Do not agree with our forecast? Create your own price forecast for Oracle by changing the base inputs (blue dots) on our interactive dashboard.

Like our charts? Explore example interactive dashboards and create your own.