Navitas Semiconductor: When A 74x Sales Multiple Meets Structural Reality

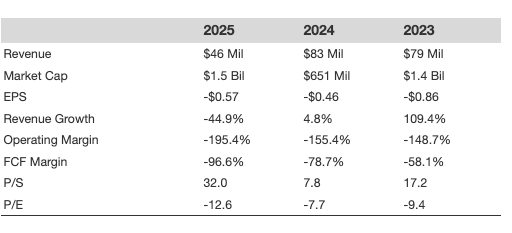

Navitas Semiconductor (NVTS) stock has surged 110% in less than four months, a breathtaking rally for any company. Its price-to-sales multiple ballooned from 26.8x to a massive 74.3x during this period. This gain happened just as revenues over the last year actually declined by -45%.

The immediate catalyst was Q1 2026 revenue guidance that beat consensus, fueling a powerful narrative of a successful pivot to AI. Investors, eager for any AI-related story, took this as proof the turnaround was complete. But is the market ignoring the bigger picture?

Is The AI Pivot Real?

To a certain degree.

- Qualcomm Stock’s Next Chapter Might Be Written In The Cloud

- Arista’s Very Good, Very Bad Year

- What Applied Materials Stock Was Shouting Before The Surge

- Fox Swings For The Fences, And Investors Duck For Cover

- Decoding LRCX Stock’s Premium Valuation

- AI Powers Arista Networks Stock, But Its Real Strength Lies Elsewhere

Navitas makes tiny, efficient power chips that prevent AI servers and electric cars from wasting energy and overheating. This technology is genuinely valuable for power-hungry applications. AI data centers consume enormous power, and Navitas’ GaN and SiC chips can cut energy losses by up to 40% versus traditional silicon, making them important to the next generation of efficient infrastructure.

The market seized on the better-than-expected Q1 guidance, which signaled a return to sequential growth after a painful decline. This was enough to reframe the company as a key supplier for the AI infrastructure buildout.

The bull case rests on this ‘Navitas 2.0’ strategy, targeting high-power markets with a reported $2.4 billion design-win pipeline. However, Navitas is a ‘transition’ archetype. This pipeline is a promise, not yet a profitable reality.

While the data center remains the focus of the AI buildout, edge AI could be the next big thing, and Qualcomm could be a big beneficiary

So Is The Valuation Justified?

Not exactly. The trailing twelve-month financials paint a starkly different picture, with revenue growth at -44.9% and operating margins at -195.4%. See how Navitas revenue and margins compare with peers such as Monolithic Power Systems (MPS) and ON Semiconductor (ON)

The company’s free cash flow margin is a deeply negative -96.6%, indicating significant cash burn.

These numbers leave zero room for error at a 74x sales multiple. Revenue over last year stood at a mere $46 million. Sure, the markets are valuing Navitas on its future potential, but there are considerable risks here, too.

Investors often assume any AI infrastructure supplier is a safe bet. Unlike NVIDIA, which commands pricing power through a deep software moat, power chip markets are commoditized and brutally price-competitive, and the company’s weak margins prove it. The core institutional risk is competitive displacement by giants like STMicroelectronics, who are already winning multi-billion-dollar deals with major cloud providers.

Investors should watch for peer commentary on SiC pricing pressure this quarter, as any market weakness could expose Navitas’ fragile position.

The story is compelling, but the numbers reveal the underlying strain. Review the historical data to see the disconnect between the stock’s trajectory and the company’s actual performance.

So, What Is The Real Bottom Line?

The ‘Navitas 2.0’ story is powerful, but the current valuation has detached from fundamental reality. The risk of competitive failure from entrenched incumbents is too high to justify the premium. The scale tips toward staying on the sidelines until the company can translate its pipeline into profitable revenue.

Your Next Move

Misreading this situation is costly. Chasing the rally ignores the profound structural risks, while dismissing the AI pivot entirely could mean missing a genuine turnaround.

Don’t get caught in the hype. Dig into the competitive landscape and watch for peer commentary on SiC pricing this quarter, a key indicator of market health. Keep a tab on it here.

Timing a volatile stock like Navitas is a high-stakes game. For a more disciplined approach to growth investing, consider our expert-managed portfolios. The Trefis High Quality Portfolio (HQ) focuses on companies with proven execution and durable moats.