Micron’s AI Rally Is Built On Earnings Growth, Not Enthusiasm

Micron (MU) has rallied more than 140% over the past six months, prompting concerns that the rally may have run too far.

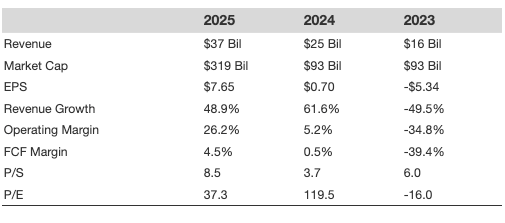

But here’s the rub: while the stock soared, its P/E multiple actually compressed to 21.3x trailing earnings, and the stock, in fact, trades at a mere 8x forward earnings.

What gives when a stock doubles but gets cheaper on an earnings basis?

What Is Fueling The Rally

- Stronger Bet Than Monolithic Power Systems Stock: NVDA, MU Deliver More

- Stronger Bet Than Broadcom Stock: NVDA, MU Deliver More

- NVDA, MU Top Texas Instruments Stock on Price & Potential

- Does Micron Technology Stock Still Have Room to Run?

- Pay Less, Gain More: MU Tops MACOM Technology Solutions Stock

- Does Micron Technology Stock Have More Upside?

Micron’s recent growth comes from high-bandwidth memory (HBM) chips, the specialized, ultra-fast memory that powers AI data centers. This is one of the fastest-growing segments in semiconductors, and Micron is one of the companies at the center of it.

The March earnings call made the scale of this opportunity concrete. Management guided for Q3 FY’26 (August fiscal year) revenue of approximately $33.5 billion, up from under $10 billion last year, alongside a massive 81% gross margin.

Adding to the conviction: Micron’s entire HBM supply is sold out through calendar year 2026, giving the company significant pricing power for the foreseeable future.

The effects are spilling into the broader memory market, too. HBM production requires approximately three times the wafer capacity of standard DRAM, which pulls supply away from the wider market. DRAM prices rose an estimated 90% to 95% in the first calendar quarter as a result.

The numbers don’t lie, and they paint a picture of explosive, fundamental growth, not just speculative hype.