Read This Before Buying Cisco Systems Stock

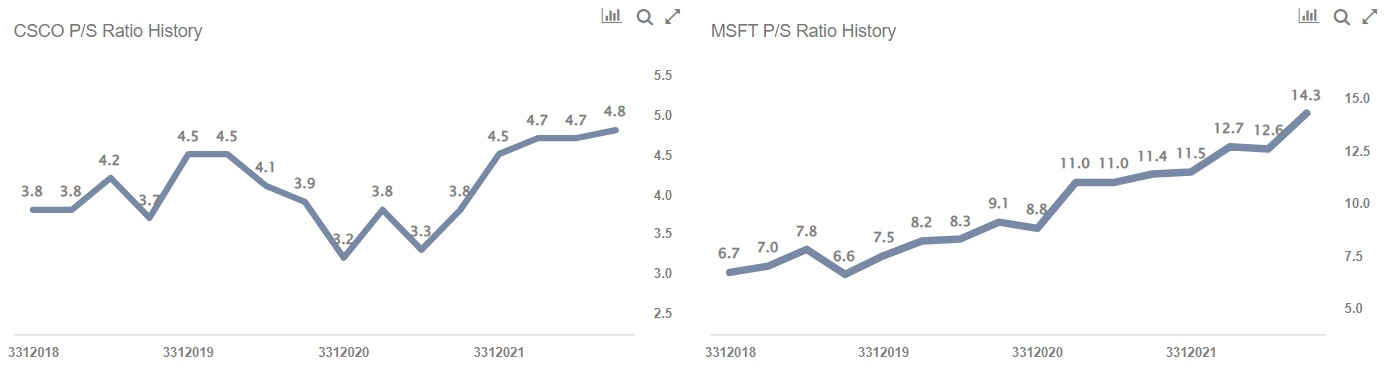

We think that Microsoft Corporation (NASDAQ:MSFT) currently is a better pick compared to Cisco Systems (NASDAQ:CSCO). Microsoft stock trades at over 14x trailing revenues, much more than Cisco’s 5x multiple. Does this gap in the companies’ valuations make sense? We believe it does, and we only expect it to increase further. While both companies have seen a steady rise in revenues since the lockdowns started being lifted, Cisco’s revenues have struggled over the past three fiscal years, while Microsoft has seen more consistent sales growth. Microsoft’s revenues have grown consistently YoY from $96.6 billion in FY ’17 to $168.1 billion in FY ’21 (Microsoft’s fiscal year ends in June). In comparison, Cisco’s revenue growth has been inconsistent, with revenues first rising from $48 billion in FY ’17 to $51.9 billion in FY ’19, then pulling back to $49.8 billion in FY ’21 (Cisco’s fiscal year ends in July). Additionally, Microsoft’s LTM operating margins currently stand at 42.1%, higher than Cisco’s 24.4%.

Having said that, there is more to the comparison, which makes Microsoft a better bet than Cisco, even at these valuations. Let’s step back to look at the fuller picture of the relative valuation of the two companies by looking at historical revenue growth as well as operating income and operating margin growth, along with the financial position. Our dashboard Cisco vs Microsoft: Industry Peers; But Microsoft Is A Better Bet has more details on this. Parts of the analysis are summarized below.

1. Microsoft Is The Clear Winner On Revenue Growth

- Will Higher Software Sales, Splunk Deal Drive Cisco Stock Back To $60?

- Is Cisco Undervalued At $46, Amid Network Recovery And Splunk Revenue Upside?

- With Product Sales Sluggish, What To Expect From Cisco’s Q3 Earnings?

- Down 6% In Last 3 Months, Will Cisco Stock See A Recovery Following Q2 Results?

- Why Is Cisco Buying Splunk?

- Why The Digital Infra Theme Continues To Outperform

Cisco has seen a compounded revenue growth of just 0.4% over the last three fiscal years, compared to a 15.1% compounded growth in Microsoft’s revenues over the same period. Even for the most recent quarter (Q1 ’22 for both companies), Microsoft’s revenues grew 22%, in comparison to Cisco’s growth of 8%.

Additionally, Microsoft is a much larger company whose revenues as of FY ’21 stand at $168 billion, more than 3x that of Cisco’s, which stand at $49.8 billion. Microsoft’s revenues grew 18% in FY ’21, as compared to FY ’20, and this was primarily driven by a 24% rise in revenues from the Intelligent Cloud segment, a segment we expect to grow at a similar rate in the medium term. Additionally, for comparison, Microsoft reported operating income at $70 billion for FY ’21, a number higher than Cisco’s total sales in the same period.

2. EBIT margins: Microsoft Has Seen Stronger Growth

Microsoft’s operating margins stand at 42.1% on an LTM basis, higher than Cisco’s 24.4%. Microsoft’s EBIT margins rose from 34.1% in FY ’19 to 41.6% in FY ’21, and currently stand at 42.1%. This steady rise in profitability was driven by increased margins across all reporting segments. Meanwhile, Cisco’s EBIT margins have gone from 27.4% in FY ’19 to 25.8% in FY ’21, and currently stand at 24.4% While cost of services have dropped, higher SG&A expenses and restructuring costs have eaten into the company’s margins.

3. Microsoft Is Also In A Better Net Cash Position

Microsoft’s debt-to-equity ratio currently stands at 2.1%, less than half that of Cisco’s current debt-to-equity ratio that stands at 4.9%. Additionally, Microsoft’s cash as a % of assets, stands at 38.9%, higher than Cisco’s 25.1%. Clearly, Microsoft has a much better cash cushion compared to Cisco.

The Net of It All

Microsoft’s revenues are much larger than that of Cisco, and the former also has a higher EBIT margin and has seen higher historical revenue growth. Our comparison of the post-Covid recovery above, also shows that Microsoft has been performing better than Cisco lately. Despite Microsoft’s P/S ratio of 14x, compared to Cisco’s 5x, we believe that this gap is set to widen. Additionally, Cisco’s P/EBIT ratio currently stands higher at 36x, compared to Microsoft’s 34x. Given that Microsoft has seen stronger revenue and margin growth lately, we believe this isn’t justified and Microsoft could close this gap soon. As such, we believe that Microsoft stock is currently a much better bet compared to Cisco stock.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market consistently since the end of 2016.

| Returns | Dec 2021 MTD [1] |

2021 YTD [1] |

2017-21 Total [2] |

| MSFT Return | 2% | 51% | 439% |

| CSCO Return | -1% | 25% | 85% |

| S&P 500 Return | 1% | 24% | 107% |

| Trefis MS Portfolio Return | 0% | 45% | 295% |

[1] Month-to-date and year-to-date as of 12/1/2021

[2] Cumulative total returns since 2017