Ramp Up Of Oil Production Will Drive Anadarko’s Value In The Near Term

Anadarko Petroleum (NYSE: APC), the US-based independent exploration and production (E&P) company, has had a good first half of 2018. The company’s revenue has shown significant improvement backed by improving commodity prices and an oil-focused production mix. Further, the oil and gas producer witnessed an improvement in its cash flows, which enabled it to increase its quarterly dividend as well as share repurchase program for 2018. Going forward, the company will continue to focus on the three Ds in its portfolio — the Delaware basin, the DJ basin, and the deepwater assets in the Gulf of Mexico (GOM) — that will drive its value going forward.

We currently have a price estimate of $63 per share for Anadarko Petroleum, which is higher than its market price. View our interactive dashboard – Anadarko Petroleum’s Price Estimate – and modify the key drivers to visualize the impact on its valuation.

- How Will Anadarko Perform In 2019?

- Andarko 4Q: Andarko To See Improved Earnings But Cash Flow May Face Headwinds

- Anadarko Has Been Trading At A 52-Week Low. Where Will It Head Going Into 2019?

- Higher Oil Output And Improved Commodity Prices Will Drive Anadarko’s 3Q’18 Results

- Key Takeaways From Anadarko’s Second Quarter Results

- What To Expect From Anadarko’s Second Quarter Results

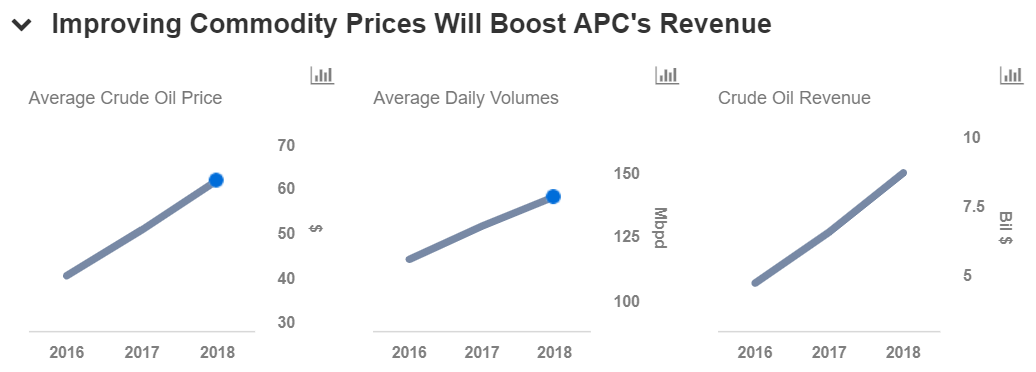

Anadarko aims to capitalize on the increasing crude oil prices by expanding its oil volumes. The company expects to grow its oil production by 12%-14% in 2018, with the Delaware basin, the DJ basin, and the deepwater assets in the Gulf of Mexico (GOM) driving this growth. With this, the oil and gas company also plans to alter its product mix and expand its liquids exposure from around 40% in 2010 to over 65% in the coming years. At the end of the 2Q’18, oil comprised 57% of the company’s total sales volume mix compared to about 52% in the second quarter of last year. Also, the company’s total liquids improved to 73% from 67% of the mix during the same horizon. Given the shift in its production portfolio, the company is likely to generate higher margins in the coming quarters, which will drive its value in the long term.

Further, Anadarko has divested a large portion of its non-core and low-margin assets to focus on expanding its oil production in its key basins and enhance its profitability. This will enable the company to achieve its objective of delivering shareholder value rather than focusing on volume growth. In fact, the company has been returning higher value to its shareholders by completing $3 billion worth of share repurchase and extending the program by $1 billion. Further, the company has announced its plans to retire $500 million of debt to reshape its capital structure. If Anadarko continues to execute well on its growth plans by focusing on high-margin oil assets, coupled with the recovery in commodity prices, we expect to witness a notable jump in the company’s earnings as well as valuation.

Do not agree with our forecast? Create your own price forecast for Anadarko Petroleum by changing the base inputs (blue dots) on our interactive dashboard.

Like our charts? Explore example interactive dashboards and create your own.