What Drove The Sell-off In Robinhood Stock?

Robinhood (HOOD) stock collapsed about 30% over the last five months, with its forward P/E multiple getting slashed from a lofty 60x to just about 41x. This happened even as total revenues grew over 25% in the same period.

So what’s happening?

The trigger was a Q4 earnings miss, fueled by weak crypto revenue and rising expenses. This gave bears the ammunition they needed, shifting the narrative from a growth story to a margin-pressure story.

We think this is a classic overreaction.

- Own Caterpillar For The Boom? Federal Signal Deserves A Look

- Oracle Stock at Support Zone – Bargain or Trap?

- How Long Could Bloom Energy Stock Stay Underwater?

- Seagate Stock’s Dip Looks Familiar, But The Price Tag Is New

- BSX, RMD Look Smarter Buy Than Stryker Stock

- S&P 500 Stocks Trading At 52-Week Low

Is Robinhood’s Profit Engine Broken?

Not exactly. To understand the fear, you have to see how they make money: from interest on your cash and by selling a premium subscription for advanced trading tools. This model is now under intense scrutiny.

The Q4 report showed a 38% year-over-year drop in crypto revenue, a key growth engine. Worse, operating expenses jumped 38%, crushing the profitable growth narrative and sending investors fleeing for the exits.

This short-term panic feeds a much larger fear. The market now sees a company whose largest profit center, Net Interest Revenue at 32.1% of sales, is directly threatened by potential Fed rate cuts.

So Why Is This A Calculated Buy?

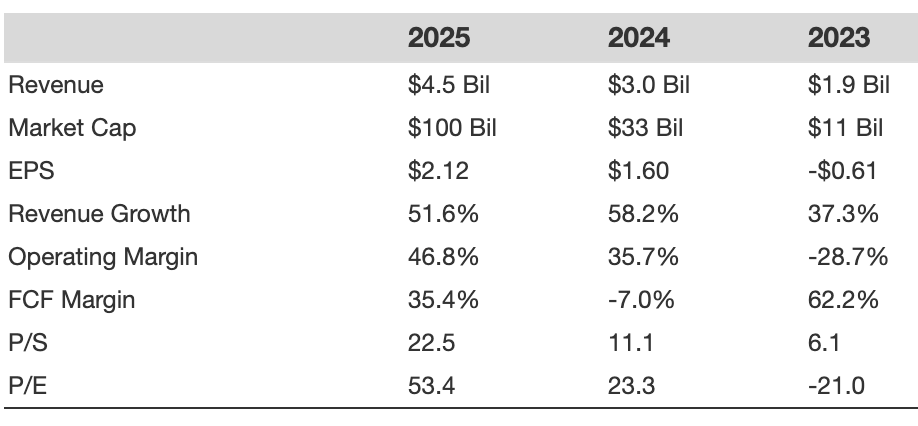

Look past the quarterly noise at the trailing twelve months. Revenue grew an impressive 51.6% with a powerful 46.9% operating margin. The only blemish is a negative free cash flow last quarter, a direct result of the expense surge.

That sell-off provides a margin of safety. The market has priced in the rate-cut apocalypse, but it’s ignoring the underlying strength of the platform’s pivot. A 41x P/E is far more reasonable for a company with this growth profile. (See HOOD valuation multiples)

The bull case is simple and powerful. Gold subscribers are up 58%, and net deposits grew at a 35% annual rate to a record $68 billion. This isn’t a fickle trading platform anymore; it’s becoming a sticky, high-ARPU financial service.

Robinhood also has an upside from wealth management services. Over the next two decades, an estimated $84 trillion is expected to pass from Baby Boomers to Millennials and Gen Z, the very cohorts that form Robinhood’s core user base.

The numbers tell the story of a company in transition, not in collapse. Review the historical data to see the pivot in action.

So, What Is The Real Bottom Line?

Robinhood is a buy, but it’s not for the faint of heart. The threat of margin compression from rate cuts is real and will cause volatility. However, the market has over-punished the stock, ignoring the successful pivot to a more durable, subscription-based model.

Your Next Move

Misreading this moment could be costly. Seeing Robinhood as just another meme stock broker means missing its transformation into a diversified financial firm. The window to buy into this narrative shift at a discount may be closing.

Don’t take our word for it; track the data yourself. The key event is the Q1 2026 earnings call, where guidance on net interest revenue will be critical. Keep a tab on it here.

Managing this kind of single-stock risk is tough. Our portfolios are built to capture upside while protecting against volatility. Consider the Trefis High Quality Portfolio (HQ) for a more balanced approach.