Dunkin’ Brands Q3 Earnings Preview: All Eyes On International Segments

Dunkin’ Brands’ (DNKN) is scheduled to report its Q3 2015 earnings results on October 22, 2015. [1] Analysts are estimating that the company will deliver an EPS growth of 4% year-over-year (y-o-y) on $204 million in net revenues, up 6% y-o-y. [2] The parent company of two of the most iconic brands in the restaurant industry, Dunkin’ Donuts and Baskin-Robbins, Dunkin’ Brands has outperformed market EPS estimates in 3 of the last 4 quarters.

The company has been reporting positive revenue growth for the past 10 quarters, and a strong outlook by the company in its recent Investor & Analyst Day presentation somewhat indicates a robust growth in Q3 2015 as well. Furthermore, the recent drop in the company’s stock price could make it an attractive stock. Trefis is still bullish on the stock and here’s why:

- Is Dunkin’ Brands’ Stock Overvalued?

- 20% Upside For BJ’s Restaurants’ Stock When Pandemic Subsides?

- Can Dunkin’ Brands Survive A Covid Recession?

- Donuts Over Burgers: Why Dunkin’ Brands Stock Looks More Attractive Than McDonald’s

- Dunkin’ Brands Stock Looks Undervalued At $58

- Dunkin’ Brands To Meet Consensus Estimates For FY 2019?

Trefis estimates the company’s stock price at $48, which is roughly 14% above the current market price.

See full analysis for Dunkin’ Brands

Dunkin’ Brands: International Segments To Be The Highlight

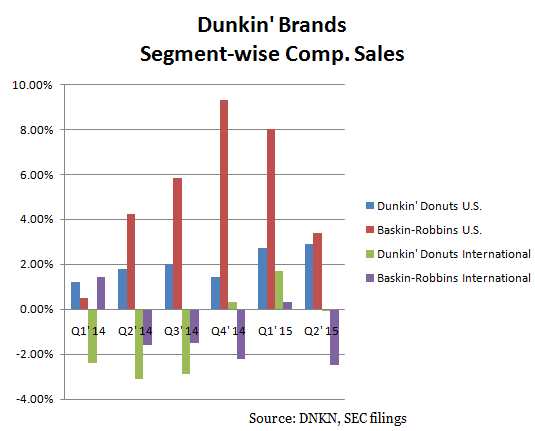

For a majority of the quarters in the past two years, the company’s U.S. segments have been reporting strong and prominent comparable store sales growth, whereas on the other hand, the international segments have been struggling with sales declines for most of the above mentioned period. According to Trefis estimates, the net EBITDA contribution of the international segments has declined from 17.9% in 2011 to 11.3% in 2014.

Now it is clearly visible from the above chart that Dunkin’ Donuts International segment showed some improvement in terms of same store sales during the last three quarters. Moreover, the Baskin-Robbins International segment lagged due to some temporary headwinds in the second quarter, such as an outbreak of MERS virus in South Korea. With new innovative menu items and strong restaurant development growth, the Dunkin’ Donuts international segment might deliver mid-single digit growth in the same store sales for Q3, whereas in the absence of those temporary headwinds, Baskin-Robbins International might post positive comparable store sales. A positive comeback from the international segments, coupled with already strong growth in U.S. segments, will boost the top-line results for the quarter.

Growth In Single-Serve Market Share

In a recent research report by UBS group, Dunkin’ Brands further gained some market share in the single-serve K-Cups segment from Keurig Green Mountain (NASDAQ:GMCR). [3] According to the report, the overall U.S. single-serve cup segment grew by 16% y-o-y, which was slower than the 18% figure over the prior 12 months. Dunkin’ Brands gained 80 basis points over the 4 week period ended September 5, 2015, and now has a 5.4% market share in this category, owing to the solid momentum of its K-Cups. The market expects the company to further improve this number in the coming few months. [4]

Furthermore, positive about its same store sales growth and a solid average check growth, the company is expecting its Dunkin’ Donuts U.S. segment to report 1.1% growth in the comparable store sales.

Accelerated Restaurant Expansion

Dunkin’ Brands is one of the fastest growing companies by unit count among the quick service restaurants. The company had 19,095 total restaurants, with 8,240 Dunkin’ Donuts U.S. restaurants, 2,490 Baskin-Robbins U.S. restaurants, and the remaining international stores, as of June 2015. In the recently held Investors & Analysts day presentation, the company mentioned that it plans to open around 5,000 Dunkin’ Donuts units in the western market, around 3,000 in the emerging markets, and only 400 in its core eastern market, to take the total Dunkin’ Donuts U.S. units to 17,000, as a long term plan.

The company is targeting a 6% growth rate, which is higher than what the company has achieved in the last 5 years, for Dunkin’ Donuts U.S. stores development, and has already picked up pace by opening its Dunkin’ Donuts stores in California.

To summarize, with these positives and no surprises, we might see a solid Q3 earnings result, which might increase investor confidence in this situation.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes: