Return To Positive Growth For Tim Hortons Brand Not Enough For Restaurant Brands International To Beat Estimates

Restaurant Brands International (NYSE: QSR) posted its third quarter results on October 24, wherein a growth in both revenues and earnings was reported. However, the company missed on consensus expectations on both metrics, despite noting positive sales and comparable sales growth across all segments. Although the return to growth for Tim Hortons (TH) was a welcome change, the comparable sales growth at its other two brands – Burger King (BK) and Popeyes Louisiana Kitchen (PLK) – slowed when compared to the preceding quarter (Q2 2018) as a result of the softness in the U.S. The revenue, and consequently, the EBITDA improvement, was also driven by a change in the revenue recognition standards, which helped to push up the margins and therefore, the EPS. The company has in the past laid down its list of priorities for FY 2018, which included improving comps for TH, building momentum behind BK, and accelerating restaurant growth for Popeyes Louisiana Kitchen (PLK). While the initiatives implemented by the company seem to be working, there is still considerable work to be done.

We have a $70 price estimate for Restaurant Brands International, which is higher than the current market price. The charts have been made using our new, interactive platform. The various driver assumptions can be modified by clicking here for our interactive dashboard on Restaurant Brands International’s Performance In Q3 2018 And Estimating Its Fair Price, to gauge their impact on the earnings and price per share metrics.

- Will Q4 Results Help Extend The 20% Gain In Restaurant Brands’ Stock Since Early 2023?

- After A 9% Top-Line Growth In Q2 Will Restaurant Brands Stock Deliver Another Strong Quarter?

- What To Expect From Restaurant Brands’ Stock Past Q2 Results?

- Restaurant Brands Stock to Likely See Little Movement Post Q1

- What’s Next For Restaurant Brands Stock?

- What To Expect From Restaurant Brands Stock Post Q4?

Factors That May Impact Future Performance

1. “Winning Together” Plan: RBI detailed this plan during the first quarter earnings call webcast, through which it intends to improve the performance of TH and drive franchisee profitability. This plan focuses on “restaurant experience, product excellence, and brand communications” and is intended to stave off the negative press it has been receiving in the wake of the company’s issues with a group of dissident franchise owners. Resolving the issues with TH franchisees is critical for RBI’s future growth. Any growth in this segment in the future can be expected to come from international markets. In 2017, the company opened its first Tim Hortons restaurants in each of Asia, Europe, and Latin America, and has plans for additional openings in 2018 and 2019.

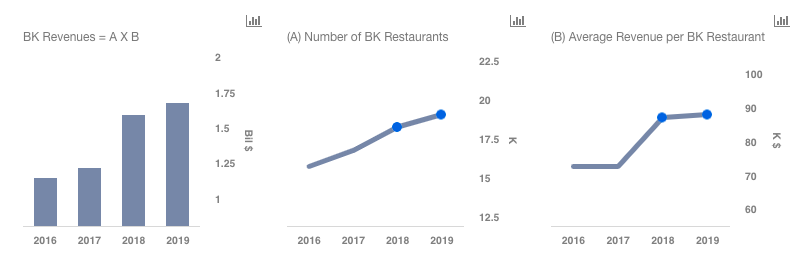

2. Expansion of Burger King: RBI is focused on expanding its Burger King chain and is entering into several franchisee agreements to fulfill this goal. The company has announced a financial agreement with private equity giant Bridgepoint to expand in the U.K. This agreement was followed by a master franchise agreement with Nexus Point in Taiwan and another master franchise agreement to expand its presence in the Netherlands. In Q3, the company grew its restaurant count by roughly 6.1% year-on-year, which reflects continued growth from its partners all around the world, although, given the slight deceleration in Q2 and Q3, an increased rate of restaurant growth can be expected in Q4. Faster growth of the Burger King chain can become a key driver of revenues for RBI.

3. Implementing Delivery: RBI began testing delivery for BK in the U.S. in the first quarter across several hundred restaurants and numerous markets. This strategy follows from the successful model seen in many of its international markets, including China and Spain. The company has now expanded its delivery facility to nearly 2,000 restaurants in North America and over 5,000 restaurants around the world. Moreover, a mobile order and pay app was launched in the U.S. this quarter, which may help to improve the customer experience. The company is also testing delivery for PLK in the U.S., and currently has several hundred restaurants in various markets across the country that are participating in the test.

4. Prospects of Popeyes Louisiana Kitchen: Revenue growth from this segment can be expected to come from a higher number of its restaurants. In Q3, the company had a net restaurant growth of 7.6%, helping in achieving system-wide sales of nearly 8%. The company has also signed a master franchise agreement for expansion in Brazil, which calls for opening 300 restaurants in the country over the next ten years. In the quarter, the company also announced a master franchise development agreement in the Philippines, marking its first major development agreement for the Popeyes brand in Asia.

5. Tim Hortons’ Poor Results In The U.S.: While comps returned to the plus side for TH in Q3, there is still plenty of work to be done. The global comparable sales improved just 0.6%, reflecting Canada comparable sales of nearly 1%, partially offset by continued softness in the U.S. Given the fact that, in general in Canada, the breakfast items are the fastest growing products sold even in the day, TH launched ‘Breakfast Anytime,’ in contrast with previously, when breakfast items were only sold till noon. This was done based on research conducted by the company, the results of which showed that this program appealed to roughly 75% of respondents and 60% of TH’s guests indicated they would likely buy a breakfast sandwich after 12 noon. Moreover, one-third of the guests indicated their frequency of visits would increase post the implementation of the program. This initiative can be considered to be the key driving factor behind the improvement in comps for Canada, and should continue to benefit the company in the forthcoming quarters.

6. Expansion of TH in China: QSR entered into a Master Franchise Joint Venture agreement with Cartesian Capital Group to develop and open over 1,500 Tim Hortons restaurants throughout China over the next decade. This represents a tremendous opportunity for growth for TH.

7. Higher Tax Rate: As a result of the implementation of the new Tax Act and due to a benefit from stock option exercises, the effective tax rate fell to -12.1% in FY 2017. In FY 2018 and FY 2019, we expect the metric to increase to 8.4% and 10.4%, respectively, which will pressure the net income margin. On the other hand, improving EBITDA margin in FY 2019, as a result of cost reductions, should help to offset this pressure next year.

See Our Complete Analysis For Restaurant Brands International

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.