What’s Driving Our $165 Price Estimate For Motorola Solutions?

Motorola Solutions (NYSE:MSI) has seen its stock price rise by over 40% this year, driven by improving earnings, growing LMR business, and expanding software sales. Trefis is increasing its price estimate for the company to about $165 per share, which is slightly ahead of the current market price. Below, we provide our expectations of the company’s key divisions and the rationale driving our price estimate.

View our interactive dashboard analysis on What’s Driving Our $165 Price Estimate For Motorola Solutions?

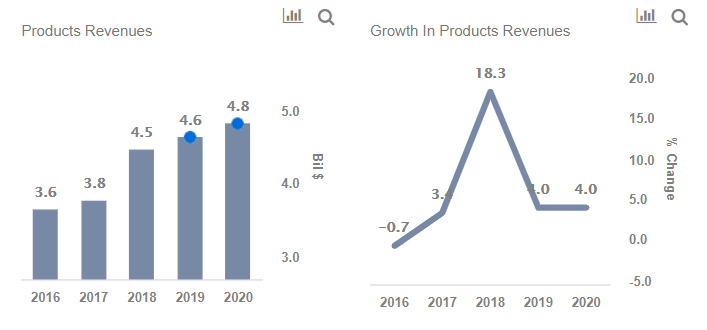

Products Division Will Benefit From LMR Growth, New Acquisitions

- The company’s products business has been expanding, driven by higher land mobile radio (LMR) sales in North America and the EMEA region, as well as due to its acquisition of video surveillance cameras maker Avigilon.

- We expect the LMR business to continue to expand, driven by the company’s increasing focus on software and platforms, which increase switching costs.

- The Avigilon business should also grow, as the company cross-sells these products to its commercial and government customers.

- Moreover, the current re-escalation of the trade dispute between the U.S. and China could give Avigilon a boost versus Chinese companies – who play a significant role in the North American surveillance hardware market.

- Up 30% In The Last 12 Months, Will Motorola Solutions Stock Rally Further Following Q4 Results?

- What’s Happening With Motorola Solutions Stock?

- What’s Happening With Motorola Solutions Stock?

- Motorola Solutions Stock Has More Than Doubled Market Returns Since 2018- Here’s Why

- Motorola Solutions Stock Has Almost Doubled The S&P’s Returns Since 2018- Here’s Why

- Motorola Solutions Inc. Stock Looks Set To Continue Its Rally

Software & Services Business Will Outgrow Products

- Motorola’s services and software revenues have been expanding driven by the company’s end-to-end offerings such as command center, its growing installed base of systems, and increasing focus on offerings such as command center.

- The company has also been making acquisitions to drive the software business. Earlier this year, it acquired VaaS, a provider of AI-driven image capture and analysis technology for vehicle location, in order to expand its command center software portfolio.

- The focus on this software could help the company cross-sell radio and video surveillance products as well, as it ties them together as a single platform, potentially also improving stickiness.

- MSI’s software business grew at a CAGR of about 13% over the last 3 years, versus a CAGR of under 7% for Products.

- We expect software sales as a % of product sales to be about 70% by 2020, up from 64% in 2018.

Estimating Net Income

- A growing mix of software sales could bode well for Motorola Solutions margins.

Estimating EPS

- EPS should grow to close to $9 by 2020, driven by expanding earnings and the company’s share repurchase program.

Calculating Price Estimate

- We are valuing the company at about 19x projected 2020 EPS.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.