After Lower Prices And Volume Proved To Be A Drag On Profitability In 2018, Will Barrick Gold Spring A Surprise In 2019?

Barrick Gold Corp. (NYSE: GOLD) released its Q4 2018 results on February 13, 2019 followed by a conference call with analysts. The company fell marginally short of analysts’ expectations for revenue, primarily due to lower shipments and a decline in average realized prices of gold and copper. Barrick Gold reported revenue of $1,904 million in the fourth quarter of 2018, which marks a decline of 14.5% on a year-on-year basis. However, the company met the consensus EPS estimates with an adjusted earnings per share of $0.06 in Q4 2018, 72.7% lower than $0.22 in Q4 2017. The lower earnings was a reflection of decreasing volume, lower grades and recovery rates, higher cost of sales, and increasing direct mining costs, driven by higher energy prices and consumption.

We have summarized the key takeaways from the announcement in our interactive dashboard – Will The Poor Performance Of 2018 Affect Barrick Gold’s Stock Valuation For 2019? In addition, here is more Materials data.

- Barrick Stock Trades Below Intrinsic Value Despite Firm Gold Prices And A Strong Production Outlook

- Why Barrick Stock Is Underperforming Despite Strong Gold Prices

- Will Barrick Gold Stock Recover From The Sell Off?

- With Gold Prices Firming, Is Barrick Gold Stock A Buy?

- Soaring Yields Hit Barrick Gold Stock. Is This An Opportunity To Buy?

- Should You Buy Barrick Gold Stock As Copper Production Soars?

Key Factors Affecting Earnings

Lower volume: Gold shipments declined by 5.8% to 1.26 million ounces in Q4 2018 from 1.34 million ounces in Q4 2017. Gold volume has witnessed a steady decline over the last couple of years, with shipments decreasing by 14.3% (y-o-y) in 2018, mainly driven by a 15% reduction in production volume during the year. Lower production reflected the impact of the 50% divestment of the Veladero mine in June 2017, along with lower grades and recoveries across most operations, lower throughput at Acacia as a result of reduced operations at Bulyanhulu, and lower tonnage processed at Lagunas Norte. A similar trend was observed in copper, with shipments declining by 5.7% in 2018 on the back of a 7.3% reduction in copper production for the year. The drop in copper production was driven by lower production at Lumwana – primarily due to mill shutdowns, crusher availability issues, and lower head grade and recoveries, coupled with lower throughput at Zalvidar.

Lower price realization: 2018 was marked with a lot of price volatility. After strengthening at the beginning of the year, gold prices saw a sharp decline after Q2 2018, mainly driven by rising interest rates in the US and the stronger dollar. However, gold prices staged a minor recovery in the fourth quarter of 2018, mainly driven by rising economic uncertainty which forced central banks around the world to buy more gold as a hedge against an economic slowdown. Thus Q4 2018 saw a sequential rise of 0.6% in gold prices. However, on a year-on-year basis, realized gold price declined by 4.5%, dominated by the decline in the initial part of the year. The US-China trade war had a significant impact on copper prices, which declined by 17.4% (y-o-y) in Q4 2018; whereas the realized price for the full year saw a drop of 10.7% to $1.34 for 2018. The price volatility adversely affected revenue growth for the both the segments in Q4 as well as the full year. However, prices of both the commodities have rebounded since January 2019 and we expect prices to remain elevated through the year.

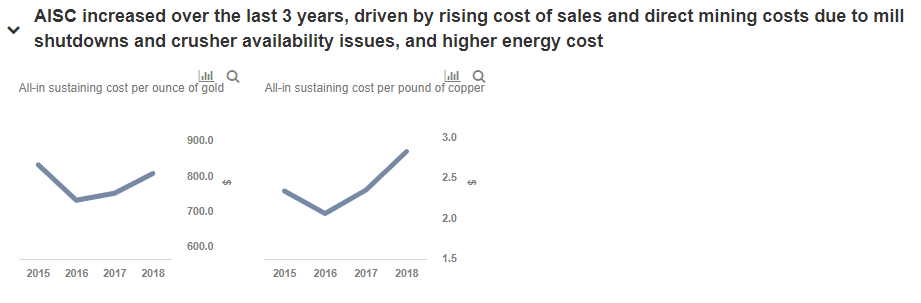

Rising cost of production: The all-in sustaining cost (AISC) per ounce of gold increased by 7.5% to $806 in 2018 compared to $750 in 2017, due to higher cost of sales, primarily driven by inventory impairment of $166 million at Lagunas Norte, exacerbated by the impact of lower grades and recoveries across most operations, coupled with higher direct mining cost due to a rise in energy prices and consumption. AISC per pound of copper saw a significant rise of 20.5% to $2.82 in 2018, compared to $2.34 in 2017, mainly attributed to a higher maintenance costs due to mill shutdowns and crusher availability issues, higher energy consumption to truck ore to the crusher, and tire costs due to road conditions at Lumwana. Additionally, depreciation expense was higher, mainly as a result of the impairment reversal recorded in Q4 2017 relating to Lumwana, resulting in higher non-current asset values to depreciate compared to the prior year.

Lower shipments and price realization of gold and copper led to total revenues decreasing by 13.5% to 7.2 billion in 2018, as against $8.4 billion in 2017. Rising cost of production during the year affected profitability. Additionally, the company reported a large impairment charge of $900 million in 2018, related to Lagunas Norte and Veladero operations, in contrast to $212 million of impairment reversal in 2017. These cost increases, along with lower revenues, dragged net margin into the red, which in turn translated into negative returns for shareholders.

Will 2019 be an inflection point?

We believe that after a dismal 2018, this year will prove to be much better for Barrick Gold. The driving force behind this optimism is the recent $6.5 billion merger with Randgold Resources (which took effect on January 1, 2019), with the combined entity having an annual revenue generating capacity of $10 billion. We expect revenue to rise by close to 16% to $8.39 billion in 2019, on the back of increased shipments and strengthening of gold and copper prices. Additionally, Randgold’s high grade ores, lower cost of production, efficient logistics framework and better supply chain, and inventory management is expected to help Barrick Gold improve its profitability, thus reflecting in a sharp increase in net margin to 10% in 2019. EPS would likely rise to $0.72 in 2019 from -$1.32 in 2018.

Expectations of higher margins and the recent announcement of a sharp rise in dividend pay-out would support growth in the company’s stock. However, the road in 2019 is not that smooth for Barrick Gold. The largest bump in its way is the planned merger of Newmont Mining and Goldcorp Inc (expected to conclude in Q2 2019) which would create the largest gold company, displacing Barrick Gold to the second spot. It would be interesting to see what additional steps the management at Barrick Gold takes to effectively counter the increasing scale of Newmont Mining and break the $14 share price ceiling in the near term.

We have a price estimate of $14 per share for Barrick Gold.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.