In Spite Of Higher Revenue, Increased Storm Restoration Charges And Lower Tax Shield Affect Duke Energy’s Margins In 2018

Duke Energy Corp. (NYSE: DUK) released its Q4 2018 results on February 14, 2019, followed by a conference call with analysts. Though the company exceeded analysts’ expectations for revenue, it fell short of the consensus on earnings per share. Duke reported net operating revenue of $6.1 billion in Q4 2018, 5.4% higher than $5.8 billion in Q4 2017. Higher revenue was mainly driven by an increase in customer base on the back of a rise in housing starts and privately-owned housing completions. The company reported earnings of $0.84 per share in Q4 2018, 10.6% lower than $0.94 in the year-ago period. Lower earnings for the quarter were driven by increased depreciation and amortization expense on a growing asset base and higher storm-related costs, partially offset by higher rider revenues.

We have summarized the key takeaways from the announcement in our interactive dashboard – High Restoration Costs and Depreciation Affect Duke’s Profitability In 2018. In addition, here is more Utilities data.

Key Factors Affecting Earnings

- Duke Energy Jumps 10% On Takeover Rebuff News – What’s Going To Happen Now?

- Duke Energy Could Have 20% Upside. What Are The Catalysts?

- Duke, Southern, Dominion: Utility Stocks Continue To Underperform. Time To Buy?

- Is Ameren’s 2x Price Rise Compared To Duke Energy Justified?

- Why NextEra’s 5x Price Rise Versus Duke Energy Is Not Justified

- Duke, NextEra, Southern: Are Big Utilities Riskier Through This Downturn?

Higher consumption: Revenue from Electric Utilities and Infrastructure segment increased by 4.2% in 2018, mainly driven by higher energy consumption per customer, which increased by 3.4% during the year. Rising economic growth and higher per capita income has led to a pick-up in construction activity and an increase in housing starts and privately-owned housing completions for most of 2018. This has led to a higher customer base for the company, which, in turn, helped Duke enhance its pricing power, reflected in a slight increase in revenue per megawatt hour (MWh). Additionally, rising sales of electric vehicles is also contributing to higher consumption and revenue. As the economy moves further toward digitization, with retail moving online, increased use of wireless internet, higher demand for electric vehicles which, in turn, adds electric charging stations, it would help in Duke maintaining its segment revenue growth going forward.

Growth in renewables: Revenue from the renewables segment increased by 3.5% in 2018 as the share of renewable energy in the U.S. continues to rise. Official records show that 18% of all the electricity in the US was produced by renewable sources in 2017, up from 15% in 2016. Though official numbers for 2018 are yet to be announced, early estimates point out that growth is better than what was recorded in 2017. Duke Energy has over 1000 MW of wind and solar projects in late stages of development. As additional consumers switch to renewable energy and with continuous decline in the cost of solar and wind energy generation, the segment is expected to be the fastest growing operating segment of the company.

Lower margins: Duke Energy saw its net income margin decline to 10.9% in 2018 from 13% in 2017, primarily driven by high storm restoration costs, higher depreciation expense, one-time severance pay, and a lower tax shield on holding company interest. In October 2018, Florida was hit by the most powerful storm – Hurricane Michael – in its recorded history, which led to over a million power outages in the Carolinas and 70,000 outages in Florida. This led to the company incurring huge storm restoration costs which adversely affected EPS to the tune of $0.07 in 2018. Additionally, depreciation expense increased by 15.5% during the year on the back of a growing asset base, eating into the company’s bottom line. Though the implementation of Tax Cuts and Jobs Act led to a lower tax outgo, this benefit of a lower tax rate was completely offset by a lower tax shield on holding company interest. This factor had an adverse effect of about $0.13 on the EPS for 2018. The bottom line was also hit by a one-time severance payment of $144 million made in Q4 2018 as a buyout package to employees to cut costs.

Outlook Remains Stable

Duke Energy’s stock has not seen much volatility over the last one year. We believe that the biggest support to the company’s stock comes from the company’s pricing power, which is derived from it being a regulated entity. Also, as the demand for renewable energy is growing at a fast pace, Duke Energy has realized this opportunity by expanding and diversifying in this segment with the acquisition of REC Solar and Phoenix Energy Technologies. Duke is hedging its bets with renewable energy as the world moves toward having a cleaner environment. The commercial renewables segment is expected to drive the company’s overall revenue growth in 2019 and beyond. Additionally, the grid modernization and improvement initiatives of the company are expected to lead to a strong revenue growth in the Gas Utilities segment as well. Though net income margin is expected to be more or less flat at the current level as the company is likely to incur additional maintenance and capital cost and take some time to cope with major natural disasters of 2018 along with higher depreciation as the asset base grows, higher revenues would most likely drive better earnings per share in 2019.

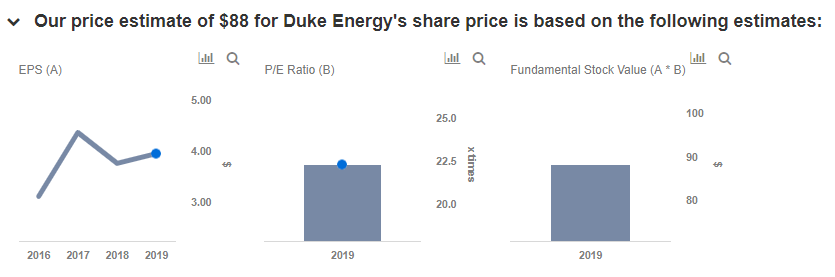

Concentrating on enhancing shareholder returns, the company increased the dividend by 4.2% in 2018. We believe that overall growth across all its operating segments without losing focus on enhancing shareholder returns would provide support to Duke’s stock price. We have a price estimate of $88 for Duke Energy’s stock.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.