Costco Rides Higher Comparable Sales To Solid Q3

Costco (NASDAQ:COST) announced solid third quarter results on Thursday, as both its revenue and earnings per share came in ahead of market expectations. However, the company’s stock was marginally down in after-hours trading as the company’s gross margins narrowed despite higher sales. This was largely due to the company’s investments to boost online sales through services like same-day delivery and automated fulfillment centers.

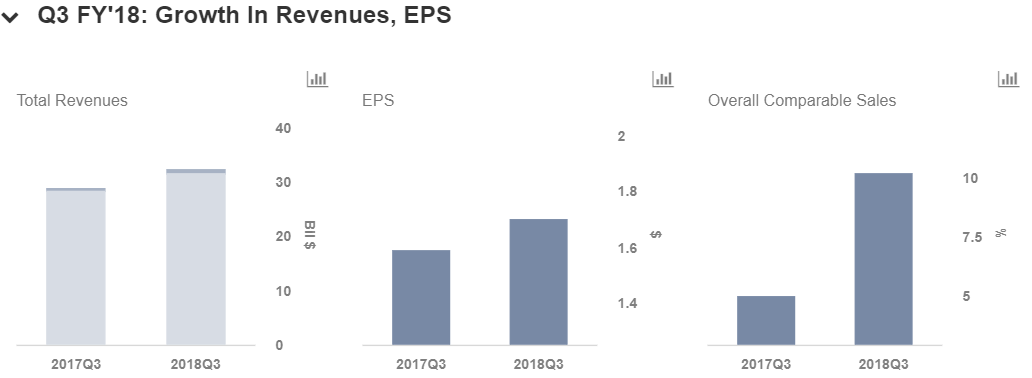

Overall, Costco’s revenue increased 12% year-over-year (y-o-y) to around $32.3 billion in the third quarter, driven by growth in membership fees and a 10% increase in comparable sales. The retailer reported net earnings of $1.70 per share, up 7% y-o-y. We have created an Interactive Dashboard which outlines our forecasts for the company and our expectations for its Q4 earnings. You can change expected revenue, operating margin and income margin figures for Costco to gauge how it will impact expected EPS for the current quarter.

Growth In Comparable Sales, Membership Fees

The company’s comparable store sales during the fiscal third quarter increased by 10%, including the impact of gasoline prices and currency effects, largely driven by a 10% comparable sales growth in the U.S. and 11% in Canada. Excluding gasoline and currency fluctuations, combined comparable sales increased by 7%, driven by 8% growth in the U.S., a 5% rise in Canada and 6% growth in other international markets. In terms of categories, foods and sundries were up slightly, while soft lines (apparel, housewares), fresh foods and hardlines (tires, hardware, health and beauty aids) declined marginally in Q3. Additionally, Costco’s growth was driven by both traffic and average transaction size growth. The company’s fiscal third quarter traffic was up 5.1% both worldwide and within the U.S. Overall, the company’s continued growth momentum confirms that it should be able to continue to see healthy traffic at its brick and mortar warehouses despite stiff competition in the grocery sector in the long run.

Costco’s membership revenue grew 14% y-o-y to $737 million, due to new sign-ups and increased penetration of the company’s higher-fee Executive Membership program. Currently, Costco’s member renewal rates are 90.1% in the U.S. and Canada and 87.5% worldwide. Meanwhile, on the e-commerce front, Costco’s online sales increased 37% y-o-y in the quarter. And on the cost side, the company’s selling, general and administrative (SG&A) expenses increased 9% y-o-y to around $3.2 billion due to increased payroll expenses, higher IT expenditures and growth in e-commerce initiatives. Going forward, the company plans to spend more in fiscal 2018 compared to fiscal 2017, owing to increases in manufacturing and e-commerce activities.

Looking Ahead

In fiscal 2018, the company plans to open nearly 23 net new warehouses, of which almost half will be located in the U.S. Consensus estimates for the company’s fiscal fourth quarter call for earnings of $2.32 per share and revenues of $42.9 billion, implying growth of about 11% and 1%, respectively. We also expect the retailer to report close to $43 billion in the fourth quarter.

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own