Should An Advisor Add 5% Bitcoin To A Retirement Account?

Bitcoin has been one of the strongest performing assets in global markets, and it’s no longer looking like just a millennial fad. Over the past year alone, the cryptocurrency has nearly doubled, trading around $119,000 today. Its rise has forced a serious question for long-term investors: does Bitcoin belong in a retirement portfolio? Looking at a capped 5% position, the data suggests that Bitcoin has not only boosted historical returns, but has done so with only a modest increase in risk, which is an unusually favorable trade-off in portfolio construction.

What’s Important For Retirement?

Younger clients with decades to invest can absorb the volatility of crypto. That’s not true for retirees, or for those near retirement. Here is what’s important for them:

- Capital preservation & income stability to cover living, healthcare and lifestyle costs.

- Lower volatility tolerance because of fewer working years left, which makes sequence of returns and drawdowns a major concern.

- Moderate growth to outpace inflation to sustain purchasing power over a potential 20-30+ year life expectancy.

Strategic asset allocation is critical to achieve retirement goals. We take a macro-conscious approach to asset allocation, even within equities – adjusting exposure across sectors and styles in the High Quality Portfolio. So considering these goals – does a volatile, risky asset like Bitcoin fit? Turns out, it actually fits perfectly.

Bitcoin Can Add A Lot Of Return, And Very Little Volatility To A Portfolio

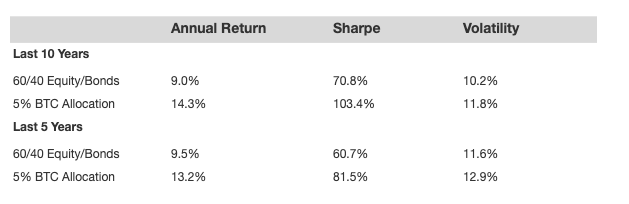

Let’s consider a portfolio that’s 60% equities and 40% bonds – using S&P 500 index fund and iShares Core U.S. Aggregate Bond ETF (AGG) as examples, and compare it with a portfolio that shifts 5% of the equity holding to bitcoin. And we consider both last 10 year and 5 year data, to understand if there is any shift in characteristics.

The analysis covers two periods: the last 10 years and the last 5 years, to see whether the relationship between risk and return has been consistent.

Return and risk comparison

Key Findings

- In both periods, introducing just 5% Bitcoin led to an annualized return increase of roughly 4 to 5 percentage points

- Volatility rose by only about 1 percentage point, meaning the extra risk was modest relative to the gain in returns.

- Sharpe ratios – which are a measure of risk-adjusted performance – improved considerably to 103% for 10 years and 81.5% for five years, suggesting that the portfolio became more efficient despite the additional volatility.

The fact that favorable risk-reward is maintained over a shorter time frame of 5 years is encouraging for retirement accounts – reducing a risk of liquidation (if need arises) during unfavorable drawdown periods.

Risks

While the numbers speak for themselves, there are some risks that investors should be aware of.

- High volatility: Bitcoin has experienced drawdowns of 70-80% multiple times, which can be uncomfortable even at small allocations.

- Limited historical track record: Our 10-year back test overlaps with Bitcoin’s strongest adoption and price growth period. As the asset matures, return and risk characteristics could very well differ.

- Correlation spikes in crises: Bitcoin can move in the same direction as stocks during sharp market sell-offs, reducing diversification benefits.

- Crypto specific risks: Counterparty, hacking, and custodial vulnerabilities are notable for crypto investors. Moreover, regulatory and policy uncertainty also exist for the evolving asset class.

The 5% Bitcoin allocation study shows how small, thoughtful adjustments can improve portfolio efficiency. The High Quality portfolio follows similar principles, outperforming the S&P 500 with over 91% total returns since inception through disciplined asset selection and risk management.

Invest with Trefis Market-Beating Portfolios

See all Trefis Price Estimates