Nvidia Stock’s Cheap 25x Multiple The Loudest Warning Yet?

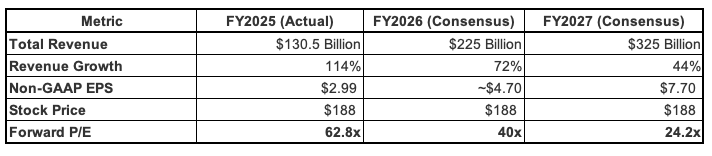

Nvidia’s revenue growth has been extraordinary. Sales surged 114% in FY’25. They are on track to grow another 72% in FY’26. For the coming fiscal year, FY’27, growth is projected at roughly 44% to over $325 billion. Few companies in history have sustained that kind of scale and expansion simultaneously. And yet, despite this, the stock trades at a mere 25x FY’27 earnings.

In most sectors, a company compounding revenue above 40% with net margins above 50% would command a premium multiple. Instead, Nvidia’s valuation has compressed from nearly 60x during the early Blackwell ramp to roughly 25x on forward numbers. The stock price has largely stayed in the $170 to $190 range in recent quarters. Earnings have not.

That being said, history shows that in semiconductor investing, the most dangerous time to buy is often when a company looks “cheap,” and the best time to buy is when it looks “expensive.” This could very well be the case for Nvidia, too.

Growth Is Outrunning Price

- FY2025: Revenue came in at $130.5 billion with adjusted EPS of $2.99, implying a P/E of about 62x at $188. This reflects strong enthusiasm around AI infrastructure spending and data center build-outs.

- FY2026: Revenue is expected to jump to roughly $225 billion, with EPS rising to $4.70. At the same $188 share price, the P/E compresses to about 40x, driven by scale, strong margins above 50%, and continued AI capex from Big Tech.

- FY2027: By January 2027, NVIDIA is projected to earn roughly $7.55 per share, driven by a gradual shift from Blackwell to Rubin and the $650 billion-plus Big Tech Capex wall—a good chunk of which will flow toward Nvidia—providing a high demand floor. With margins quite likely to hold up at 50% plus levels, consensus earnings for FY’27 are estimated at $4.70 for 2026 and $7.76 for 2027. If the stock price stays at $188, the P/E multiple stands at roughly 25x.

The Cyclical Ghost

While AI feels like a permanent shift, the industry has been defined by boom and bust cycles. To understand why the stock could still drop when it is trading at a cheap forward multiple, we have to look at cycles of the past.

In many respects, memory is the purest semiconductor commodity. Let’s take Micron for example. In 2019, after a record 2018, Micron’s EPS fell 53% from $12.27 to $5.67 as memory prices cratered. While earnings were cut in half, the stock stabilized and then climbed in anticipation of the next cycle. The P/E expanded from about 4x to 8x. Investors who bought at the “cheap” 4x multiple during the peak saw losses, while those who bought when it looked “expensive” actually rode the recovery.

Nvidia, too, has seen similar trends in the past. Before the AI boom, Nvidia had a classic cyclical moment where a low multiple preceded a crash. Nvidia was coming off record quarters driven by Ethereum mining. The stock looked “reasonable” at a P/E of around 20x—significantly lower than its high-growth average. The low multiple was the market signaling that the “crypto-demand” was a one-time spike. Within three months, the stock crashed 50%. The earnings did eventually fall as the inventory glut hit, indicating that the “cheap” 20x multiple was actually a “sell” signal.

Case 1: The Secular Growth Machine

Proponents argue that Nvidia has broken the traditional silicon cycle. This “secular” case rests on three pillars that create a permanent demand floor:

Big Capex: Big Tech (Meta, Microsoft, Amazon, and Google) committed to a collective $650 billion capital expenditure in 2026. This isn’t speculative; it’s the cost of re-architecting the global computing stack from general-purpose CPUs to accelerated GPUs, and one could argue that this is a multi-year trend. A large chunk of this capex commitment stands to flow toward Nvidia. Separately, nations like Saudi Arabia and Japan are building sovereign AI clouds to ensure data autonomy, adding a new layer of non-corporate, price-insensitive demand.

Frequent Upgrades: Nvidia has accelerated its roadmap to an annual “tick-tock” cycle. The transition from Blackwell to Rubin (launching H2 2026) forces an immediate upgrade cycle. If a customer skips a generation, they risk a sizable performance deficit against competitors. This could keep customers upgrading more frequently.

The CUDA moat: Over 5 million developers are locked into the CUDA software ecosystem. This makes it harder for companies to switch out of Nvidia’s ecosystem, as that could entail, rewriting large parts of the training stack and re-optimizing models, rebuilding distributed training infrastructure and reconfiguring networking, and revalidating the reliability of the overall system, at scale.

Case 2: The Cyclical Reality Check

Skeptics point to the history of Micron and 2018-era Nvidia, warning that even the strongest “moats” eventually face the reality of potential oversupply and shifting budgets.

ROI Focus: Shareholders of Nvidia’s biggest customers will eventually demand proof of return on the $650B spent. If AI applications (SaaS, agents) don’t generate proportional revenue, hyperscalers will pivot from essentially expanding GPU infrastructure at any cost to optimizing what they have. This could lead to a pronounced digestion period, hurting Nvidia’s sales.

ASIC and Custom Silicon Cannibalization: To escape the “Nvidia Tax,” Google (TPU), Amazon (Trainium), and Meta (MTIA) are aggressively scaling their own Application-Specific Integrated Circuits (ASICs), which excel at running AI models at scale. Companies such as Broadcom and Marvell stand to benefit from this shift. As these chips mature, they will eat into Nvidia’s market share for specific inference workloads.

Margin Mean Reversion: Nvidia’s 70% gross margins and 50%-plus net margins are an anomaly in hardware. Such profitability acts as a beacon for competition. Whether through AMD’s MI400 series or internal hyperscaler chips, pricing pressure is inevitable. This could very well impact earnings and ultimately the stock price.

Smart Wealth Management Means Diversifying Beyond Equities

Stocks are just one piece of the puzzle. To navigate shifting economic environments, you need a strategy that protects wealth through intelligent diversification across asset classes.

Would a portfolio with 10% commodities, 10% gold, and 2% crypto protect you better if markets crash 20%? In today’s volatile landscape, diversifying beyond stocks is critical. We’ve crunched the numbers and found that multi-asset allocation is key. Our wealth management partner helps HNIs implement these strategies, using tools like the Trefis High Quality Portfolio to optimize the equity portion.

Invest with Trefis Market-Beating Portfolios

See all Trefis Price Estimates