5 AI Fed Chairs on Wednesday: Hike or Hold?

Disclaimer: The following is a purely fictional macroeconomic thought experiment set in June 2026, designed to explore how the distinct monetary philosophies of five historical Federal Reserve Chairs might clash over a hypothetical policy dilemma. It does not reflect real-world events, current data, or financial advice.

Markets are on edge. It is June 2026, and a global energy shock has driven a sharp resurgence in headline inflation. Inside the Eccles Building, the FOMC is deeply divided; outside, the White House is publicly demanding a pause. Tomorrow morning, Fed Chair Kevin Warsh faces his first defining test: trigger a rate hike that could shatter the committee’s fragile unity and invite intense political blowback, or hold steady and risk letting inflation expectations unmoor. To navigate this complex policy dilemma, we imagine Warsh consulting the architects of modern central banking as investors hope that the Fed won’t kill the S&P 500’s relief rally.

The Debate

KEVIN WARSH: Thank you all for convening. Tomorrow’s decision could not be more tense: headline CPI is surging from energy shocks following the Iran crisis, while internal dissent is at historic highs. I am torn between taking aggressive action to anchor expectations and preserving a fragile committee consensus. Paul, how do you read this energy pressure?

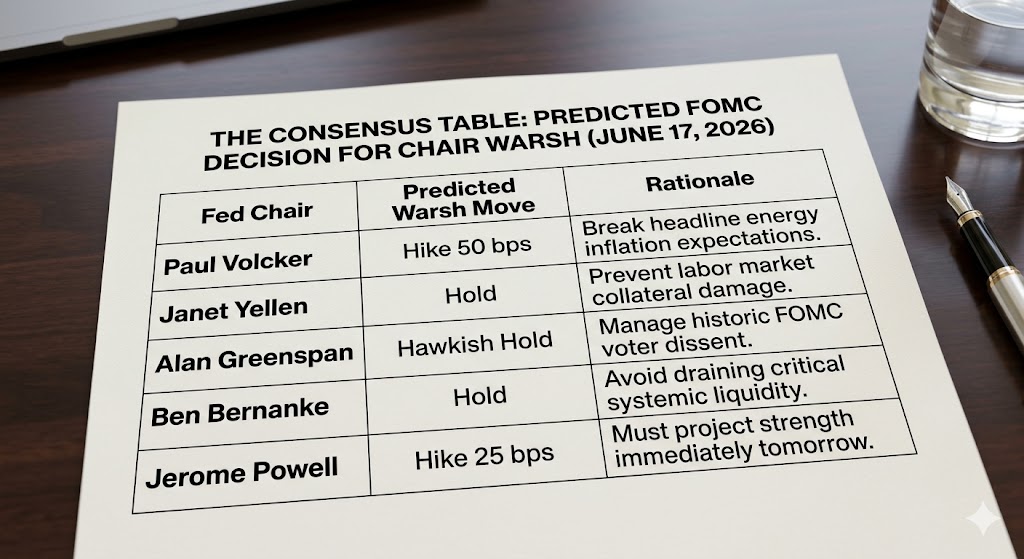

PAUL VOLCKER: Every time this committee treated energy shocks as structural exceptions rather than monetary problems, it metastasized. In 1973, Burns called it cost-push inflation and held off; by late 1974, CPI hit 12%. Energy shocks landing on top of pre-existing momentum quickly become systemic. Core PCE was already at 3.1% in January. Kevin, you cannot afford to wait. (see Market Crashes Compared)

KEVIN WARSH: I hear your urgency, Paul, but forcing a hike right now completely ignores the Board’s internal dynamics. The April minutes showed a staggering 8-4 split. If I force a tightening cycle on a divided room, the institutional fallout could be permanent. Alan, you’ve navigated these schisms – is the risk to our credibility worth it?

ALAN GREENSPAN: Paul is ignoring the damage of moving into a fractured committee. In October 1992, my FOMC split, and the market moved on the dissent signal before I even spoke. Kevin, you face the most divided room since then. Crucially, three of those dissenters opposed the easing-bias language, not the rate itself. Neutralize the easing bias in tomorrow’s statement and hold. September becomes your hike window if energy doesn’t cool.

KEVIN WARSH: Treating the easing bias as a sacrificial lamb to buy time makes sense, Alan. But managing a split is one thing; doing it during financial fragility is another. Ben, you’ve managed energy spikes right as severe credit vulnerabilities were emerging. Is a preemptive hike structurally systemic?

BEN BERNANKE: The 1992 parallel Alan mentioned is incomplete. Today, the system carries $340 billion in energy-sector commercial real estate loans rolling over through 2027. I held rates in August 2008 despite hike demands because a liquidity trap was forming beneath the inflation headline. A preemptive hike now raises rollover risks on those loans before we even know if this shock is durable.

KEVIN WARSH: So a hike threatens the credit channel. But if we hold for financial stability, what about the real economy? Janet, employment data has been softening. How does the labor market alter this equation?

JANET YELLEN: The labor market has been softening for three consecutive months. It looks stable at the headline level but is quietly losing its buffer. In 2016, I held rates in September despite three dissenters because the employment recovery wasn’t symmetric. The Fed’s asymmetric risk when labor is softening is real; a premature hike into Q4 will be very hard to walk back.

PAUL VOLCKER: You are both misreading the timeline. Janet, 1979 also had softening job gains right before inflation hit 15%. And Ben, your 2008 hold was different – energy was the tail of an unfolding financial crisis, not the cause. Today, energy is the originating shock, and core inflation is on a clear upward trajectory. Trajectories compound.

KEVIN WARSH: Paul, your history warns of inflation compounding. But if I hike, I trigger a massive political confrontation. The White House publicly insists there is no reason to raise rates, and the market prices in a 97.4% probability of a hold. Alan, how do I manage that executive pressure?

ALAN GREENSPAN: Kevin, you face a political constraint none of us dealt with on day one. I navigated our sharp 1994 tightening cycle by building absolute committee consensus first. You need to build that consensus before you move against public executive pressure. Otherwise, you risk the Fed’s independence.

KEVIN WARSH: So I need a unified committee to withstand the political heat. Ben, does the underlying data actually justify building consensus around a hold?

BEN BERNANKE: It does, if you look at the structure of the economy. Unlike Paul’s 1973 scenario, the U.S. now runs a net petroleum trade surplus, and energy’s share of consumer spending has declined. That structurally mutes the second-round pass-through. Core inflation is elevated but not spiraling. A hawkish hold with the easing bias removed is the most defensible call.

JANET YELLEN: Ben is right. And the committee’s own April minutes provide your cover: we agreed that firming is only appropriate if inflation runs persistently above 2%. One energy-driven spike doesn’t meet that bar.

KEVIN WARSH: So the consensus among Alan, Ben, and Janet is a hawkish hold. But Paul, a quiet pause will be read by the street as immediate capitulation to the White House, unmooring expectations entirely.

PAUL VOLCKER: Exactly. You must set September as an unyielding trigger. State clearly that core inflation above 3% by the August reading means an automatic hike in September. If you announce that conditional framework while stripping out the easing bias, your hold is credible. Hold and say nothing, and the market reads it as surrender.

ALAN GREENSPAN: That is the correct architecture. Remove the easing language, hold the fed funds rate, and let the dot plot show a rising September hike probability. You get your credibility signal, Kevin, without triggering the credit risks Ben outlined.

Conclusion: The Stakes for the Warsh Era

Ultimately, tomorrow’s decision is less about the immediate 25-basis-point delta and more about how the modern Federal Reserve defines its institutional boundaries. By steering toward a hawkish hold – removing the easing bias while laying down explicit, conditional triggers for September – Chair Warsh has an opportunity to synthesize these decades of conflicting central banking wisdom. It allows him to respect the structural shifts in energy pass-through highlighted by Bernanke, acknowledge the fragile labor dynamics cautioned by Yellen, and build the internal consensus championed by Greenspan. In doing so, he can project absolute independence against intense political noise without inadvertently pulling the trigger on a systemic credit shock.