Ralph Lauren Stock: A Compounding Engine Facing Its North American Test

Ralph Lauren’s (RL) net income grew at a 21.5% average clip over three years. Yet its earnings per share grew even faster, at 25.7%.

Is this compounding machine built to last?

The company delivered a 253% total stock return over the last three years. (see reason for the move.) This performance is a dual-engine outcome. It reflects both fundamental profit growth and a boost to per share earnings via share count reduction.

What’s Driving This Growth?

- Is Ralph Lauren Stock Optimizing Returns Through the Denominator Effect?

- Stronger Bet Than Nike Stock: TPR, RL Deliver More

- Better Value & Growth: TPR, RL Lead Nike Stock

- TPR, RL Top Nike Stock on Price & Potential

- Better Value & Growth: TPR, RL Lead Nike Stock

- Better Value & Growth: TPR, RL Lead Nike Stock

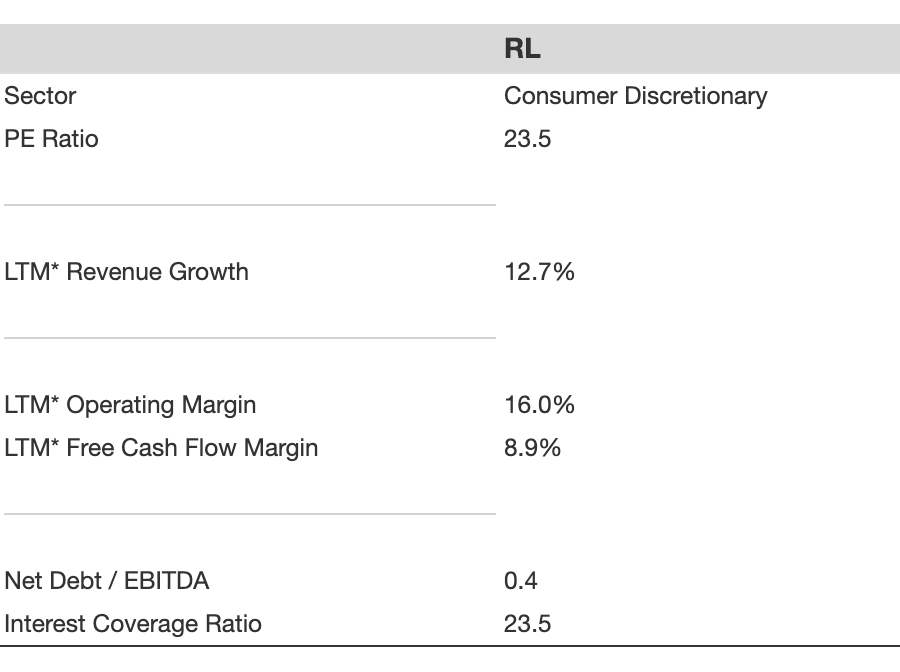

Revenue is up 12.7% over the last 12 months, with consensus expecting similar growth for FY’26. (See RL growth metrics.) But Ralph Lauren isn’t just selling more clothes – it’s selling them differently. The “Brand Elevation” strategy has systematically shifted volume away from promotional American department stores toward higher-margin direct-to-consumer (DTC) channels and fast-growing Asian markets. The payoff is visible: Q3 alone added 2.1 million new DTC customers, skewing heavily toward Gen Z as well as Millennials in Asia, which is arguably the most valuable long-term demographic the brand could be acquiring.

The next frontier is leather goods. By targeting the $200-$3,600 price tier, Ralph Lauren is moving into territory most high-end European competitors have surprisingly left underserved, opening a higher-margin category without competing head-on with the luxury giants. [1]

Funding all of this is a disciplined cash machine: $1.1 billion in operating cash flow last year, with $437 million reinvested in operations, and the remainder available for buybacks and dividends. Management’s recent upward revision to full-year revenue and operating margin guidance – despite near-term macro headwinds – indicates they see the international and DTC momentum as durable.

Ralph Lauren’s smart strategy has meant that it has outperformed peers such as PVH Corp (PVH) and Capri (CPRI). However, at the less premium end of the spectrum, American Eagle has been faring well, playing on a familiar playbook.

How Resilient Is This Engine?

The financial guardrails are strong, too. An interest coverage ratio of 23.5x means debt service is trivial. A funding ratio of 0.9 indicates its 3.0% net shareholder yield is almost entirely covered by annual cash flow.

This strong balance sheet, with net debt at just 0.4x EBITDA, provides considerable stability. It allows management to execute its long-term brand elevation strategy. They can absorb short-term market volatility without resorting to value-destroying promotions.

The primary risk remains a pullback from the North American consumer. This is the central debate weighing on the stock. The upcoming Q4 earnings report will be a critical test, with all eyes on North American sales figures to see if the engine can power through this headwind.

This strategic execution is not theoretical; it is visible in the company’s financial history. Review the key metrics below to see the compounding engine in action.

A Quick Look At Fundamentals

So What’s The Bottom Line?

Ralph Lauren’s compounding mechanics are sound, and the balance sheet is robust.

However, its performance now hinges on navigating the well-defined consumer headwind in its home market, making it a high-quality name to accumulate on macro-driven weakness.

Your Next Move

The market has priced in the risk, but the structural growth story remains intact. Understanding the key catalysts that could unlock value in the next six months is critical. The window to position ahead of these events is now.

The debate between the North American slowdown and international growth will be settled by data, not opinion. You can monitor the upcoming earnings reports and tariff rulings that will determine the stock’s direction. Keep a tab on it here.

If monitoring single-stock regulatory catalysts isn’t your preference, consider a strategy built on identifying these types of quality compounders before they face their big test. The Trefis High Quality Portfolio (HQ) is designed to hold resilient businesses with durable competitive advantages.

Notes: