McKesson Stock: A Compounding Engine Facing Its Critical Test

McKesson’s net income grew at an average rate of 14.4% over the last three years, yet its earnings per share (EPS) increased by 19.6% annually during that same window. This 5.2% gap represents the additional value management captured for shareholders through a consistent strategy.

The result is a 144% total stock return over three years. This performance stems from two distinct drivers: steady fundamental profit growth and the compounding effect of systematic share repurchases.

The Cash Engine

McKesson operates as a vital infrastructure layer for the healthcare industry. By directing billions of pharmaceutical units to pharmacies and hospitals, the company achieves a scale that generates $10 billion in annual operational cash flow. See how McKesson’s operational cash flow margin compares with some of its peers, including Cardinal (CAH) and Henry Schein (HSIC).

With capital expenditures maintained at a disciplined $838 million, McKesson produces a substantial surplus. This cash supports a 2.7% net shareholder yield through a combination of dividends and buybacks. Recent guidance suggests this momentum remains intact, as management raised its full-year adjusted EPS growth outlook to a midpoint of 18%.

Financial Stability

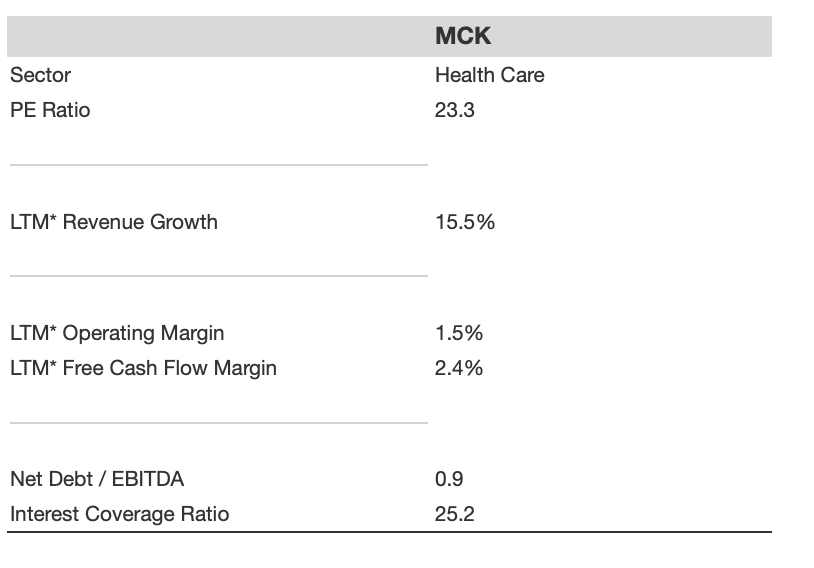

The company’s financial position is stable. Interest coverage is 25.2x, which indicates minimal risk in servicing debt. Furthermore, the payout funding ratio of 3.5 shows that annual cash flow covers shareholder returns three and a half times over.

This financial flexibility allows McKesson to navigate its current strategic shift from a position of strength. The company is aggressively investing in higher-margin segments to offset the inherent low-margin nature of its core distribution model.

The Strategic Pivot and Risks

The primary challenge is gross margin compression caused by the shift toward GLP-1 medications. While the high-margin oncology segment grew by 57%, it is currently tasked with balancing the lower margins of the popular weight-loss drug category. The upcoming Q4 earnings call on May 7 will serve as a checkpoint to see if the oncology growth is keeping pace with these margin headwinds.

McKesson’s 1.5% operating margin is a standard feature of high-volume pharmaceutical distribution. The investment thesis relies on this scale to continue generating the cash required for the company’s evolution.

A Quick Look At Fundamentals

Bottom Line

McKesson is a reliable compounding machine, but its future trajectory depends on management’s ability to execute the oncology pivot. While the mechanical drivers of the stock remain well-funded, investors should focus on how the company manages GLP-1 margin pressure.

The balance between high-margin services and the high-volume drug boom will define the next phase of growth. Keep a close eye on the consolidated gross margin percentage and any updates regarding antitrust scrutiny, as these variables will likely dictate the market’s next move.

The Bigger Picture: Strategic Engines

McKesson’s strategy of leveraging a core “engine” to fund a high-growth pivot isn’t unique to healthcare. In the technology sector, Broadcom (AVGO) is executing a similar playbook but from the opposite margin profile. While McKesson battles to expand margins, our analysis – How Broadcom’s 93% Margin Software Machine Is Powering Its AI Bets – details how a high-margin software annuity is providing the massive capital required to dominate the AI infrastructure race.

If you want to deploy high-conviction, data-backed strategies across your entire portfolio without managing the day-to-day execution yourself, we can help. Our Trefis High Quality Portfolio (HQ) strategy has outperformed its market benchmark (a combination of the S&P 500, S&P mid-cap, and Russell 2000) to produce over 105% returns since inception.