Is Dell Stock An Under-Analyzed Capital Compounder Opportunity?

Dell Technologies (DELL) operates as a capital compounder, a business model defined by the systematic reduction of shares outstanding. Over the last twelve months, the company reduced its share count by 6.0%, funded by a record $7.5 billion returned to shareholders in FY2026.

While Dell’s underlying net income grew at roughly 34.5% annually over the last three years, earnings per share expanded at 39.1%. This “denominator effect” – essentially dividing the profit across fewer shares: ownership percentages grow even during periods of flat earnings. Over three years, that dynamic has produced 429% in price appreciation, approximately 74.2% annualized.

Dell’s compounding is supported by two big drivers, which should be durable over the medium term. The first is AI infrastructure: Dell’s AI-optimized server backlog reached $43 billion in early 2026, with AI revenue projected to reach $50 billion by FY2027. The second is the commercial PC refresh triggered by the end of Microsoft support for Windows 10 in October 2025, which has stabilized the Client Solutions Group and provided consistent base-layer cash flow to fund buybacks.

The AI boom has driven up semiconductor stocks like AMD (AMD) and Nvidia (NVDA) to record highs. Is it too late to enter AMD stock?

How Does Dell Compound?

Dell operates a negative cash conversion cycle, collecting payment from customers before it settles obligations with suppliers. The cash conversion cycle measures the time between paying for inventory and receiving customer payment; a negative cycle means the company is effectively funded by its supply chain.

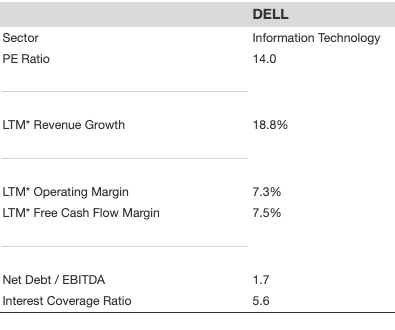

With accounts payable currently covering 3.2x inventory, Dell holds $34 billion in interest-free supplier financing to subsidize its capital allocation. An interest coverage ratio of 5.6x confirms operating earnings cover debt obligations by a substantial margin, keeping the structure well-supported. This advantage produces an operating-cash-to-net-income ratio of 1.9x, allowing share retirement to exceed reported accounting profits in any given year.

A Look At The Fundamentals

What To Monitor

Two metrics determine whether the model continues to perform at its current rate.

First is the AI backlog. At $43 billion in early 2026, the backlog is the leading indicator for future revenue conversion. Investors should track whether it continues to grow and at what pace orders are converting to recognized revenue. High-value infrastructure, including the PowerEdge XE9680, commands higher price points and reinforces the supply chain dynamics that sustain the negative cash cycle. It’s also important to track how Dell’s margins and growth compare with peers such as Super Micro Computer (SMCI) and HP Enterprise (HPE)

The second is capital discipline. The model holds as long as accounts payable coverage remains near its current level. A recent $10 billion increase in the share repurchase authorization, paired with an 80% free cash flow payout policy, reflects continued balance sheet discipline. A funding ratio of 1.1 confirms buyback commitments are fully covered by annual cash generation, with a modest buffer intact. Both metrics are reported each quarter, giving investors clear and observable benchmarks.

Is DELL The Right Investment For You?

Identifying a capital engine like DELL is only the diagnostic phase; the critical “so what” for the sophisticated investor lies in how such a machine is integrated into a resilient, multi-cycle strategy.

While the data highlights DELL as a premier compounder, all individual equities carry idiosyncratic risks that can expose a portfolio to unmanaged drawdowns if held in isolation. Trefis High Quality Portfolio (HQ) is designed to look past the surface-level narratives to surface these hidden mechanical opportunities, weaving them into a holistic framework designed to prioritize both capital preservation and consistent compounding.