Accenture Stock: Oversold, Overlooked, and Still Building The AI Enterprise

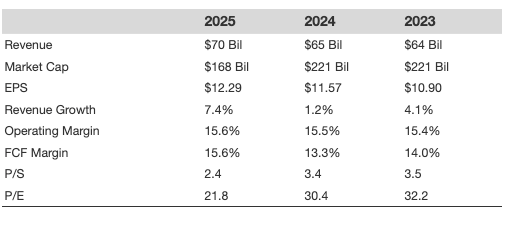

Accenture (ACN) stock has fallen over 30% the last twelve months, with its P/E multiple compressing from levels of over 22x to just about 15.3x. Yet, revenues still grew over 7% during that same period.

So what is happening?

The culprit was a lowered full-year revenue forecast, which spooked investors focused on near-term deceleration. Besides this, the market is rewarding companies that build AI infrastructure while rotating away from companies that deploy it – even though deployers like Accenture may ultimately capture value as enterprises actually put AI to work.

This reaction, however, overlooks a powerful inflection happening just beneath the surface. The market may be mistaking a strategic pivot for a structural decline.

- Could Accenture Stock’s Cash Flow Spark the Next Rally?

- Accenture Stock: Strong Cash Flow Poised for a Re-Rating?

- Could Accenture Stock’s Cash Flow Spark the Next Rally?

- Accenture Stock Pays Out $39 Bil – Investors Take Note

- Pay Less, Gain More: GIB Tops Accenture Stock

- Stress Testing ACN: Historical Drawdowns and Macro Risks

Is The Core Business Fundamentally Impaired?

No.

The trends point to a transition, not a collapse. Accenture is like a general contractor for a large company’s biggest tech projects, bringing in specialized teams to build and run complex new systems.

Investors fixated on the company lowering its full-year revenue growth forecast to a 3-5% range, a slowdown compared to last year. This single data point crushed sentiment.

Risk is in the eyes of the beholder. This connects to the structural fear that AI tools will let clients perform this work in-house, evidenced by the Consulting segment’s stagnant 1.0 book-to-bill ratio. The specific concern is that tools like GitHub Copilot or enterprise AI agents will compress the billable hours and shrink Accenture’s addressable market.

But as a quality compounder, Accenture’s scale and C-suite relationships provide a formidable moat. It is pivoting its offerings, not being replaced. Historically, technology that automates parts of knowledge work has expanded the scope of projects, not eliminated the need for integrators. AI adoption at the enterprise level is complex and messy, which is precisely where Accenture thrives.

Interestingly, software titan Microsoft (MSFT) too has been hit hard by AI-related headwinds this year. See how you can Buy Microsoft Stock At 30% Safety

So Where Is The Hidden Strength?

Look at the underlying financial health. Trailing twelve-month operating margins remain a solid 15.7%, and free cash flow margins are even stronger at 17.3%. The company is still a cash-generating machine despite the shifting growth narrative. See ACN margin metrics and how they compare to peers such as IBM (IBM) and Booz Allen Hamilton (BAH)

This robust cash flow provides a significant margin of safety. It allows the company to invest heavily in its AI transition while still returning capital to shareholders. This is the hallmark of a resilient stalwart, not a business in crisis.

The real story is in the forward-looking data. Advanced AI bookings hit $2.2 billion last quarter, nearly doubling, while overall new bookings inflected from negative growth to a positive 10%. The upcoming Q2 earnings call is the next test; if the consulting book-to-bill ratio moves above 1.1, it will validate the AI growth thesis.

A review of the key financial metrics reveals a much more stable picture than the stock price suggests.

So, What Is The Real Bottom Line?

Accenture is a quality compounder being mispriced during a technology transition. The fear of AI cannibalization is real, but the evidence of AI-driven growth in new bookings is stronger and more immediate. The scale tips decisively toward this being a compelling entry point for a high-quality business at a reasonable price.

Your Next Move

Misreading this moment means missing the inflection point in a market leader. Waiting for the narrative to become obvious could mean leaving significant returns on the table. The market is pricing in the risk, not the accelerating AI opportunity.

The key pivot metrics are the consulting book-to-bill ratio and management’s commentary on IT spending in the next earnings report. Don’t just take our word for it; track these catalysts yourself. Keep a tab on it here.

If monitoring single-stock catalysts isn’t your preference, there’s a more direct path. A managed strategy can navigate this kind of sector-wide transition for you. The Trefis High Quality Portfolio (HQ) is designed to hold resilient compounders like this through market cycles.