Would A Slowdown In The Aluminum Market Dampen Alcoa’s Q1 2019 Results?

Alcoa (NYSE: AA) will release its Q1 2019 earnings on April 17, 2019, followed by a conference call with analysts. We expect the company to report revenue of $2.82 billion for the quarter, which marks a decline of 8.7% on a year-on-year basis. Lower revenue would likely be driven by a sharp reduction in revenue from the company’s aluminum segment due to a significant drop in global aluminum prices. Market expectations are for the company to report a loss of $0.06 per share in Q1, driven by a decrease in revenue, lower shipments, decrease in price realization, and higher expenditure to improve the existing asset base.

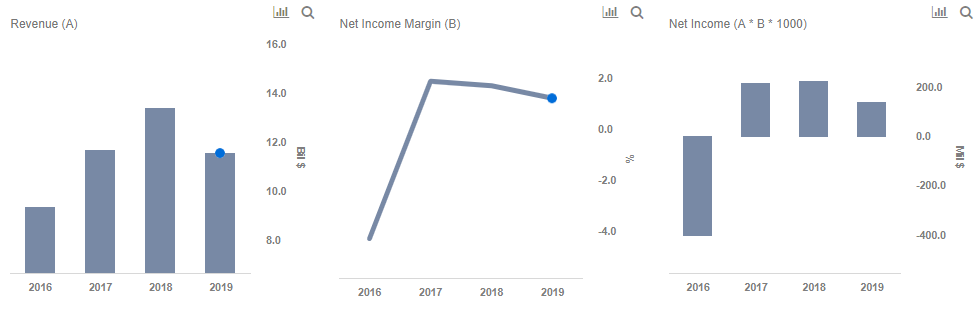

We have summarized our key expectations from the company’s earnings in our interactive dashboard – How is Alcoa expected to fare in Q1 2019 and what is the outlook for the full year? In addition, here is more Materials data.

Key Factors Affecting Earnings

Alumina Revenue

- Revenue from third-party alumina sales is expected to come in at close to $1 billion, which would be a decline of over 11.5% sequentially, driven by an 11.3% drop in price realization and lower shipments. However, on a year-on-year basis, alumina revenue is expected to increase by 9.2%, mainly due to a much lower price level during Q1 2018.

- Alumina shipments are expected to decrease from 2.38 million tons in Q1 2018 to 2.35 million tons in Q1 2019. Lower volume is expected to be driven by lower demand for alumina with many aluminum companies shedding capacity in China (alumina is a raw material for aluminum companies).

- With a year of being in deficit, alumina prices increased significantly during most of 2018. However, currently due to lower demand, alumina is expected to be in surplus (excess supply) from Q1 2019, which has in turn led to a sharp drop in prices. Thus, we expect price realized per ton of alumina to decrease to $425 in Q1 from $479 per ton in the previous quarter. However, the price would still be higher than $385 during Q1 2018.

Aluminum Revenue

- Revenue from third-party primary aluminum sales is expected to decrease by 23.3% (y-o-y) to $1.51 billion in Q1 2019, compared to $1.97 billion in the year-ago period. Decrease in aluminum revenue is expected to be driven by a drop of close to 24% in price realized per ton of aluminum sold. The decrease in price realization is in line with a sharp drop in global aluminum prices since December 2018.

- With aluminum exports from China being at record highs (exports exceeded 500kmt in seven of the last eight months) due to very low domestic demand driven by a drop in industrial and construction activity, the metal is in excess supply world-over. This has led to a sharp drop in the price of aluminum to below $1,900/ton in Q1 2019 from its high of over $2,620/ton in mid-2018. We expect Alcoa to realize $1,890/ton of aluminum in Q1 2019, significantly lower than $2,483/ton in Q1 2018.

- Such a sharp reduction in price is expected to completely overshadow a marginal increase in shipments to 800kmt for the quarter.

What Is In Store For The Year?

- For the full year, we expect revenue to decrease by close to 14% (y-o-y) to $11.5 billion in 2019, led by slowdown across all its operating segments for the year.

- A drop in total shipments is expected to adversely affect the company’s profitability as the total cost would be attributed to lower volume. Expectations of net income margin declining from 1.7% in 2018 to 1.2% in 2019 would also reflect increased expenditure from the company to improve its asset base, though this would provide benefits in the form of margin improvement in the long-term.

- Net income would likely be around $138 million on the back of lower revenue and drop in margins.

Trefis has a price estimate of $37 per share for Alcoa’s stock, which is higher than its current market price. Alcoa has been able to beat consensus estimates in each of the last four quarters. We believe that the company’s stock price could see a short term improvement if it manages to beat the consensus this time as well. Additionally, the company’s plans to focus on improving its asset base and reducing cost, along with the recently announced $200 million share repurchase program (of which $50 million worth of shares have been repurchased) would continue to support the growth in its stock price.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.