Does United Rentals Stock Qualify As A Top-Tier Capital Compounder?

United Rentals (URI) has grown net income at a 6% average clip over the past three years. Yet earnings per share have expanded by a much faster 9.3% over the same period.

This denominator effect is a powerful wealth creator, contributing to a 125% total stock return in three years. The performance is a dual-engine outcome. It is driven by fundamental profit growth combined with a meaningful boost from systematic share repurchases.

Is The Core Business Actually Growing?

Absolutely. Imagine a massive rental yard for construction giants; United Rentals provides everything from bulldozers to portable power generators for America’s biggest building projects.

- Salesforce Stock Can Sink, Here Is How

- Is Philip Morris International Stock Undervalued Stock Or Value Trap?

- Is LLY Stock Setup For A Rerating?

- Is Tenet Healthcare Stock an Under-Analyzed Capital Compounder Opportunity?

- 5 Catalysts to Monitor Over In The Next 2 Quarters For LLY Stock

- Could Accenture Stock’s Cash Flow Spark the Next Rally?

While residential construction has softened under persistent high interest rates, URI has pivoted toward mega-projects: semiconductor fabs, battery plants, and data centers that require specialized, large-scale equipment that smaller rental houses can’t provide. This is a business of immense physical scale and logistical precision.

Caterpillar (CAT) is also a big beneficiary of the datacenter buildout. See Why CAT Stock Is 2026’s Accidental AI Play

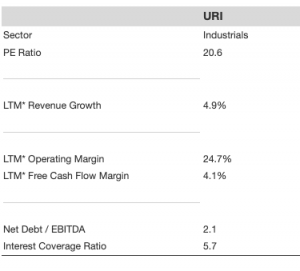

The company’s operational engine is formidable, generating $5.2 billion in operating cash flow last year. After a disciplined $4.5 billion capex reinvestment program to maintain its fleet, it still delivered a total shareholder yield of over 5%. (See URI growth and margins)

This is the mechanical core of the compounder.

However, the engine is showing signs of moderation. While 2026 guidance points to continued growth in revenue and cash flow, the pace is decelerating. Critically, planned share repurchases are guided lower, signaling a more cautious capital allocation stance.

Can The Balance Sheet Withstand A Downturn?

The company’s financial guardrails appear robust.

An interest coverage ratio of 5.7x provides a substantial cushion for servicing debt obligations. Furthermore, a funding ratio of just 0.3x indicates that total shareholder returns are covered more than three times over by operating cash flow.

This financial reality provides significant stability. It allows management the flexibility to navigate a cyclical slowdown without jeopardizing its capital return program or core operations. The balance sheet is a source of strength, not a point of failure.

The primary risk remains a slowdown in non-residential construction, evidenced by fleet productivity moderating to just 0.5% in the last quarter. This cyclical pressure is the central debate. Commercial construction such as office buildings, retail strips, and warehouses has hit a wall. The upcoming Q1 2026 earnings call will be critical for investors to see if that key metric has stabilized.

This dynamic between operational strength and cyclical pressure is not theoretical. A review of the company’s historical performance reveals the tangible results of this compounding engine in action.

A Quick Look At Fundamentals

So, What Is The Real Bottom Line?

United Rentals is a contested engine. The internal mechanics of cash generation and shareholder returns are sound, but they are fighting against significant external headwinds. Investors should trust the machine’s design but remain highly vigilant of the challenging operating environment.

Your Next Move

The market is actively debating whether the company’s specialty growth can offset its cyclical challenges. Understanding the next pivot point is critical before the narrative solidifies.

The key catalysts, from fleet productivity metrics in the next earnings report to monthly construction data, will determine the stock’s direction over the next six months. Keep a tab on it here.

If monitoring single-stock cyclical indicators isn’t your preference, a professionally managed strategy focused on durable businesses may be a better fit. The Trefis High Quality Portfolio (HQ) is designed to identify resilient compounders built to perform across economic cycles.