Oil & Gas To Lead A 20% Drop In Union Pacific’s Energy Freight In 2020?

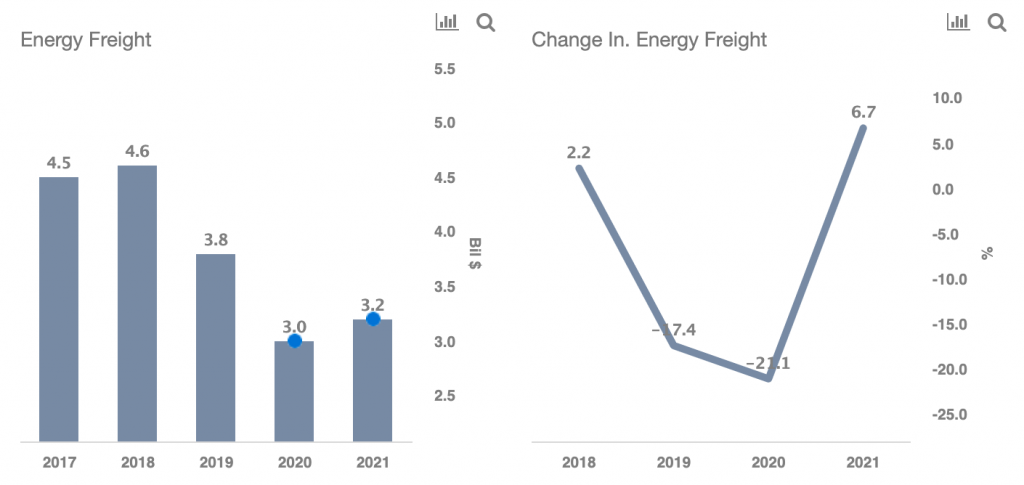

Union Pacific’s (NYSE:UNP) Energy Freight segment, which consists of the transportation of coal, crude oil, sand, and petroleum products, has seen revenues shrink from $4.5 billion in 2017 to $3.8 billion in 2019, and we expect these revenues to decline further in 2020 to around $3.0 billion, reflecting a 21% y-o-y decline, as we detail in our interactive dashboard, Union Pacific Revenues: How Does UNP Make Money?

There are several factors behind the revenue decline. Like most railroad companies, Union Pacific has seen its energy freight revenues shrink over the recent years, as lower natural gas prices weighed on the coal demand. Things are likely to only get worse over the coming months, as the coronavirus outbreak has disrupted global economic growth, and the demand for coal is expected to fall sharply. In fact, The U.S. Energy Information Association (EIA) predicts a 22% y-o-y decline in the U.S. production in 2020. Beyond coal, the oil & gas industry has also taken a hit, led by the oil price war. Oil prices (WTI) plummeted over 50% from $52 levels towards the end of January to sub $25 levels as of May 5. These multi-year low oil prices will likely result in lower production in the U.S., thus impacting the shipment of frac sand, as well as oil related products.

But then why is Union Pacific still in the energy freight business? Why doesn’t it focus more on its industrial commodities freight segment, where the segment revenue grew from $5.2 billion in 2017 to $5.8 billion in 2019? Despite falling revenues for energy freight, it is an important segment for Union Pacific. Coal is required for several power plants, along with steel, cement, and other industries. The U.S. oil & gas industry is also very large in size (the U.S. oil reserves are ninth highest in the world) with transportation requirement of crude, frac sand, and petroleum by-products. Railroads are the most efficient and cost-effective means of such transportation. And from Union Pacific’s point of view, the decline in energy freight over the recent years has primarily been due to lower shipments, while the company managed to grow its pricing. Even though the revenue share of the Energy Freight segment has shrunk from 21% in 2017 to 17% in 2019, and it will continue to shrink over the coming years, we believe that it remains an important part of the company’s business model, as we detail in our interactive dashboard on Union Pacific Revenues.

- Should You Pick Union Pacific Stock At $250 After 20% Gains Last Year And Q4 Beat?

- Up Over 2x In 2023 Is AMD A Better Pick Over Union Pacific Stock?

- Should You Pick Union Pacific Stock After An 18% Fall In Q3 Earnings?

- What To Expect From Union Pacific’s Q3 After Stock Up Only 2% This Year?

- Should You Pick Union Pacific Stock Over McDonald’s?

- Earnings Beat Ahead For Union Pacific Stock?

Company Overview

Union Pacific is engaged primarily in freight transportation in the western two-thirds of the United States. Its rail network is over 32,340 route miles, and it serves many large population centers in 23 states. Its customers include chemical producers, industrial manufacturers, agricultural companies, coal, oil & gas, and mining companies, steel processors, and automotive companies, who pay Union Pacific to carry their goods. Union Pacific’s competitors include trucking companies, along with other railroad companies, such as Norfolk Southern, BNSF Railway, and CSX Corporation.

Union Pacific reported $21.7 billion in Total Revenues for full-year 2019. This includes 5 operating segments, of which the key 4 segments are:

- Agricultural Commodities Freight: Agricultural Commodities Freight refers to grains, fertilizers, ethanol, and biofuel related shipments.

- Energy Freight: Energy Freight refers to shipments related to coal, crude oil, sand, and petroleum products.

- Industrial Commodities Freight: The industrial product commodities freight refers to the transportation of industrial products and utilities like lumber, steel, and construction products, metals and minerals, paper, furniture and appliances, and waste products by rail.

- Premium Freight: Premium Freight includes intermodal freight, which refers to the shipment of containers that can be moved from one form of transport to another. The segment also includes automotive freight.

Our interactive dashboard highlights all the components of Union Pacific’s Revenues and compares the company’s top line with peers, Norfolk Southern and CSX Corporation.

Energy Freight segment revenues will likely decline 21% in 2020

- Energy Freight has decreased from $4.5 billion in 2017 to $3.8 billion in 2019 and we expect it to shrink 21% to $3.0 billion in 2020. This can be attributed to weak demand outlook for both the coal and oil & gas industries.

- There has been an overall shift to natural gas to meet the energy demand, as it is a cleaner form of energy. The demand for coal is linked to the pricing of natural gas. Natural gas prices have declined from around $5 levels in 2011 to $2 levels by the end of 2019, though they have been volatile in the range of $1.50 to $5.00 per MMBtu (million British Thermal Unit), and this has impacted the coal demand and its shipments.

- Looking at the trend in oil prices, it will likely have a significant impact on drilling activities, thereby resulting in lower sand volume for railroad companies.

- While Union Pacific’s energy freight shipments declined from 1.5 million carloads in 2016 to 1.4 million carloads in 2019, average revenue per energy carload grew from $2,460 to $2,671 over the same period. This trend could continue in the medium to long run.

Union Pacific’s Premium Freight on the rise, though 2020 will likely be challenging

- Premium Freight has increased from $5.8 billion in 2017 to $6.2 billion in 2019 and we expect it to shrink 10% to $5.6 billion in 2020.

- The key factor behind this growth is the pricing. While total volume hovered around 4.1 million units between 2016 and 2019, average revenue per unit grew over 10% from $1,385 to 1,537 over the same period.

- The segment revenues jumped 14% in 2018, as the company benefited from capacity constraints in the trucking industry, but now the trucking industry has added capacity, which weighed on the segment growth over the recent quarters. Apart from intermodal, automotive is expected to be sluggish in the near term. The current COVID-19 crisis is expected to have a significant impact on the automotive industry.

Overall, the Energy Freight segment is expected to face headwinds in the near term, though it remains an important business segment for Union Pacific. Additional details about how other components of Union Pacific’s Revenues have changed over the years and are likely to trend going forward are available in our interactive dashboard. Trefis estimates an outlier case of Union Pacific’s stock falling to levels below $100.

Union Pacific is not the only railroad company to face the headwinds. Given the current pandemic, and its impact on the economy, CSX’s stock can drop 30% from the current levels of $60.

Our dashboard forecasting US COVID-19 cases with cross-country comparisons analyzes expected recovery time-frames and possible spread of the virus.

Further, our dashboard -28% Coronavirus crash vs. 4 Historic crashes builds a complete macro picture. Additionally, the complete set of coronavirus impact and timing analyses is available here.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams