Why Is HIMS Stock Down 40%?

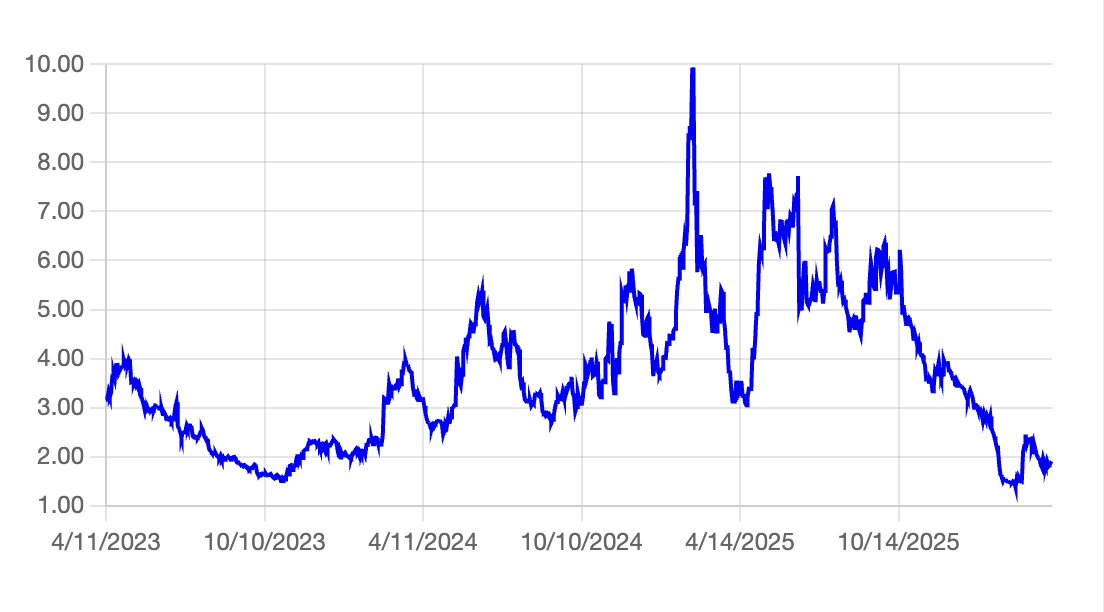

Hims & Hers (HIMS) stock is down roughly 40% YTD, a massive underperformance driven entirely by a sudden regulatory crackdown on its high-margin weight-loss business. At $20 per share, the stock has fallen over 70% from its 52-week high. That is a lot of pain baked in.

But is it deserved?

Some of it, yes.

In early 2026, Hims’ strategy for low-cost, copycat weight-loss drugs was effectively dismantled in a matter of days. In February, the FDA categorized it as “unapproved” forcing an immediate halt to the product. Furthermore, Novo Nordisk hit Hims with a patent infringement suit alleging illegal mass compounding. To cap it off, the HHS referred the company to the Department of Justice for a potential investigation into federal drug law violations. This was not a strategic pivot; it was an abrupt, forced halt. However, Hims and Novo Nordisk reached a settlement in March. Hims agreed to stop selling the compounded pill and instead became a distribution partner for branded Wegovy.

- Beyond the Rally: What Could Support Or Stall ArcelorMittal

- Same Intuit, Half the Price. What’s Actually Going On?

- How Oracle Stock Rises To $300

- At 175x Earnings, Palantir Isn’t Really As Expensive As It Looks

- What’s Really Fueling The Amazon Stock Rally?

- Where Could The Next Breakout for Oracle Stock Come From

Pixabay

The Financial Fallout

The financial impact materialized immediately. Even though Q4 2025 earnings beat estimates on February 23, the forward outlook rattled Wall Street. Management guided Q1 2026 revenue to $600M–$625M, missing the analyst consensus of $653M, and explicitly flagged a $65 million revenue hit tied to regulatory shipping changes.

More importantly, the unit economics are shifting. By pivoting in March to resolve legal disputes by selling FDA-approved Wegovy, Hims is transitioning from a high-margin manufacturer of compounded drugs to a lower-margin middleman for branded ones. Add in the intense pricing pressure from Amazon (AMZN) Pharmacy’s entry into the space, and the path to maintaining subscriber growth suddenly looks much steeper.

What the Market is Ignoring

However, the market seems to be pricing the stock as if the entire business is broken. It isn’t. Despite the GLP-1 overhang, the core operation remains structurally sound. Hims boasts 2.5 million subscribers and recently bolstered its international footprint with the Eucalyptus acquisition.

HIMS’ revenue has climbed steadily from $527M in 2022 to $2.35B in 2025 across a broadening set of verticals, including hair loss, mental health, sexual health, and dermatology. The compounded weight-loss drugs accelerated recent growth, but they did not create the foundation of the business.

The Valuation Reset

The valuation reset has been drastic. In early 2025, near its peak, HIMS traded at a price-to-sales (P/S) multiple of roughly 8-10x. Today, at $20 per share on $2.35B in trailing revenue, the P/S ratio sits at just 2x. For context, the stock’s historical P/S median is 3.3x. Even returning to a median 3.3x multiple implies a stock price above $30, representing roughly 50% upside from current levels.

The Verdict

The risk is real, and the margin compression is a genuine headwind. But at 2x sales on a business generating $2.35B in revenue with a massive, sticky subscriber base, the market is pricing in a near-worst-case scenario. As investors wait to see if the new international and branded pivots can replace the lost compounding revenue, the stock sits near a 52-week low. Historically, this is exactly where the best entry points emerge.

Sudden regulatory crackdowns and 40% drops are harsh reminders of single-stock risk. While catching an oversold bounce can be lucrative, a balanced approach is essential to weather unpredictable volatility and protect your capital. Why settle for average market returns? Our Trefis High Quality Portfolio (HQ) strategy has outperformed its market benchmark (a combination of the S&P 500, S&P mid-cap, and Russell 2000) to produce over 105% returns since inception.