Uncertain Macroeconomic Environment A Headwind For Halliburton Stock

[Updated 08/26/2021]

Despite OPEC easing production cuts in the coming months, oil field service firms including Halliburton (NYSE: HAL) are likely to observe slow top line recovery due to an uncertain macroeconomic environment as upstream companies remain committed to cash preservation and capex curtailment measures. Moreover, the company’s cash conservation policy limits economic returns, leaving investors to bet on rig count numbers to realize capital gains. We highlight Halliburton’s stock performance with its peers and broader markets in an interactive dashboard analysis, Halliburton Stock Return.

- Up 7% This Year, Will Halliburton’s Gains Continue Following Q1 Results?

- What To Expect From Halliburton’s Q3 After Stock Up 10% This Year?

- What To Expect From Halliburton’s Stock?

- Can Halliburton Stock Return To Its Pre-Inflation Shock Highs?

- Halliburton Stock Likely To See Higher Levels Post Q1 Results

- What to Watch For In Halliburton’s Stock Post Q4?

[Updated 06/09/2021] – Halliburton Stock Looks Overvalued

The shares of Halliburton (NYSE: HAL) have reached pre-Covid levels in recent weeks assisted by higher benchmark prices and recovering demand. Along with a 35% contraction in the top line, the company’s net property, plant and equipment declined by 41% last year – reporting $3.8 billion of impairment and other charges. Despite a quick jump in benchmark prices, U.S. rig count numbers remain 43% below pre-Covid levels. Moreover, the EIA expects a slow improvement in rig count figures as benchmark prices are likely to observe a correction next year. Given the company’s ongoing capital preservation measures including capex cut and trimmed dividend (leading to lower dividend yield), Trefis believes that HAL stock is overvalued. We highlight the historical trends in revenues and earnings along with the full-year 2021 expectations in an interactive dashboard, Halliburton Valuation: Is HAL Stock Expensive Or Cheap?

Region-wise performance during the pandemic

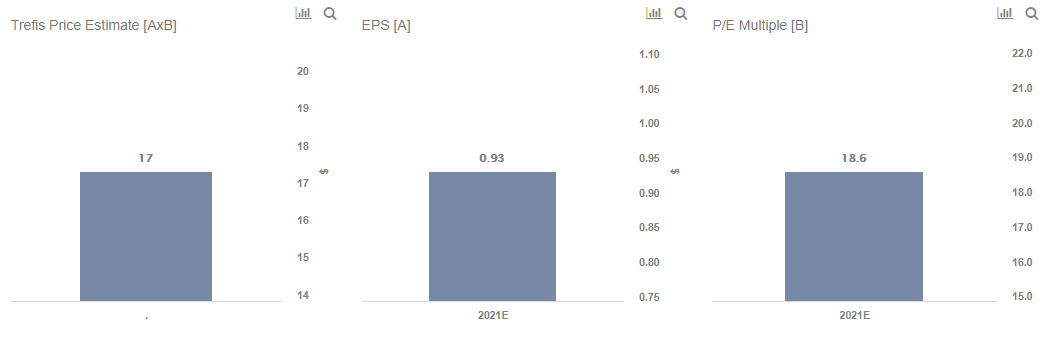

Halliburton provides exploration, drilling, completion, and production services to upstream oil & gas companies. In 2020, the company’s North America, Latin America, Europe & Africa, Middle East & Asia regions observed 52%, 30%, 14%, and 13% of revenue contraction, respectively. Per Q1 filings, North America’s contribution remains 43% below pre-Covid levels despite high benchmark prices. It is largely due to capex curtailment measures implemented by shale oil producers. As OPEC+ eases production during the latter half of the year, demand for well and completion activity in the U.S. is likely to reduce – impacting Halliburton’s revenues and margins. Notably, North American operations contribute 53% of the company’s top line. We expect Halliburton to report $15.4 billion of revenues and $1.00 of earnings per share in 2021.

Industry Outlook

Brent and WTI benchmarks surpassed $70/bbl mark in recent weeks as OPEC+ continued with previously announced production curtailments for July. Crude oil and petroleum product inventories have returned to historical levels in the U.S. and OECD countries. Given the supply restrictions by OPEC, benchmark prices are likely to remain high in the near-term as rising demand puts pressure on reserves. However, the EIA expects benchmark prices to decline by next year as OPEC+ increases production.

Is Schlumberger a better pick? Halliburton Stock Comparison With Peers summarizes how HAL compares against peers on metrics that matter. You can find more such useful comparisons on Peer Comparisons.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams