Is Walt Disney Stock Undervalued Even After 100% Recovery?

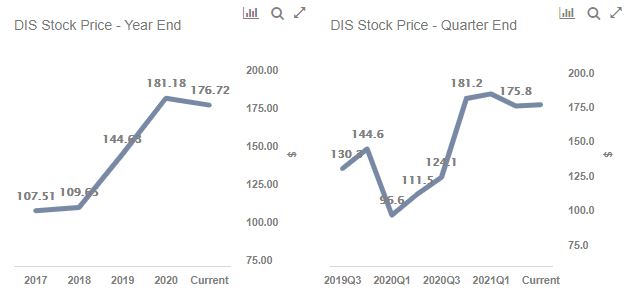

Despite more than doubling from its March 2020 lows, at the current price of $177 per share, Walt Disney stock (NYSE: DIS) still looks undervalued. Disney stock has increased from $86 to $177 off its 2020 bottom, compared to the S&P 500 which has increased more than 90%. The stock has been able to outperform the market due to an extremely strong performance of its streaming business, Disney+, as streaming demand surged during the pandemic. Along with continued strong demand for streaming, with gradual lifting of lockdowns and a successful vaccine rollout, Disney’s traditional businesses like cable and theme parks are also seeing gradual recovery. Though the recent surge in Covid-positive cases is a cause of concern for these traditional businesses, the widening vaccination coverage is expected to see further recovery in business in the coming quarters. Thus, despite such a sharp recovery recently and the stock being more than 60% above its 2017 level, we believe expectations of higher revenue and earnings in 2021 and 2022 will provide Disney’s investors with a potential gain of around 15%. Our dashboard Walt Disney (DIS) Stock Has Gained 64% Since 2017 has the underlying numbers.

Some of the stock price rise between 2017 and 2020 can be justified by the P/S multiple rising from 3.5x to 5x. During the same period, Disney’s revenues increased almost 20% from $55.1 billion in 2017 to $65.4 billion in 2020 on account of acquisitions. However, with the number of shares rising sharply on account of these acquisitions, on a per share basis the revenue increased only marginally from $35 in 2017 to $36 in 2020. Thus, the rise in the P/S multiple was entirely driven by expectations of continued strong growth in streaming and the revival of traditional business segments. The P/S multiple, which currently stands at around 5.5x, is likely to remain elevated at the current level as revenue and earnings expectations remain strong for the near term.

- Disney Stock Has 2x Upside If It Rises To Pre-Inflation Shock Highs Of $202 Per Share

- Disney Stock Could Rise Over 2x If It Recovers To Pre-Inflation Shock Highs

- Will Slowing Streaming Growth Impact Disney’s Q3 Results?

- Disney Stock Could More Than Double If It Recovers To Pre-Inflation Shock Highs

- A Deep Dive Into Disney’s Streaming Operations After A Tough Q2

- What To Expect As Disney Reports Q2 Results?

Outlook

The global spread of coronavirus led to lockdown in various cities across the globe, which affected industrial and economic activity. Due to lockdowns in almost all major cities over the globe, film shooting halted while amusement parks also remained shut for months. The company’s traditional key revenue sources – theatrical, theme parks, etc. – had come to a virtual stop due to the pandemic. Additionally, the cord-cutting led to a drop in Cable TV and advertising demand. This was evident in the Q3 2020 results of the company where Disney’s revenues declined 42% y-o-y. This began to improve a bit in FY2021, as the revenue decline during the first six months of FY2021 was 18% y-o-y.

There have been signs of reopening of the economy and lifting of lockdowns which led to a surge in the stock price. The successful vaccine rollout has also led to expectations of faster demand revival, with theatrical releases and reopening of theme parks likely to get back on track soon in the coming months. Any further recovery and its timing hinge on the broader containment of the coronavirus spread. Our dashboard Trends In U.S. Covid-19 Cases provides an overview of how the pandemic has been spreading in the U.S. and contrasts with trends in Israel. The company is currently focusing on streaming, with Disney+ having a subscriber base of 103.6 million in just one and a half years of operations. To put things in perspective, Netflix achieved a subscriber count of 200 million after a decade of operations; at the current rate Disney is likely to reach that milestone is a much shorter time. Additionally, the company’s traditional businesses are also likely to see a turnaround in 2021 and 2022 as advertising, theme parks, and cable revenues get back on track. Thus, with investors’ focus having shifted to 2021 and 2022 numbers, strong revenue and earnings growth in the next two years will drive a further rise in the stock price. As per Trefis, Disney’s valuation works out to $205 per share, reflecting an upside of more than 15% from its current level.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market since 2016.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams