Why Cliffs’ U.S.-Centric Strategy Makes Sense

Cleveland Cliffs Inc. (NYSE:CLF) was historically a U.S.-centric company before its expansion into the Asia Pacific region, which largely enabled the company to cater to customers in Asia through the seaborne iron ore market. However, the APAC operations experienced an extended period of declining revenue from 2012-2015 as a result of declining prices amid a supply glut on the seaborne market. As a result of a change in management in 2014 amid the period of declining prices, the company decided to focus on the more predictable US market going forward. The recent change of the company’s name from Cliffs Natural Resources to its historical name of Cleveland-Cliffs Inc. is indicative of the change in the company’s priorities geographically. [1]

Favorable business prospects in the U.S.

Cliffs APAC operations face heavy competition from iron ore giants such as Rio Tinto, Vale, and BHP which have access to low-cost iron ore deposits and operate at large economies of scale. The supply side of the iron ore market in the APAC region is dominated by the production decisions of these mining giants, in contrast to Cliffs which is a relatively small producer in the APAC region. Large production increases by these companies adversely affected international iron ore prices between 2012 and 2015, with Cliffs’ Asia Pacific operations reporting losses over this period as a result of subdued pricing. Thus, Cliffs is largely at the mercy of its competitors in the seaborne iron ore market, particularly as concerns its ability to influence supply and pricing in the market.

- Will Cleveland-Cliffs Stock Move Higher Following Q1 Results?

- What’s New With Cleveland-Cliffs Stock?

- What’s Happening With Cleveland-Cliffs Stock?

- Why We Are Raising Our Price Estimate For Cleveland-Cliffs Despite A Weak Q4

- With Contracted Prices For 2023 Up, Is Cleveland-Cliffs Stock A Buy?

- Company Of The Day: Cleveland-Cliffs

In contrast to Cliffs’ position in the APAC region, the company has established a dominant position in the US market accounting for roughly 54% of the total U.S Iron Ore Pellet production capacity. [2] The company derives close to 72% of its revenue from its U.S Iron Ore operations. Further, in contrast to the pricing situation in the APAC region, Cliffs’ U.S. operations are characterized by pricing contracts that are more closely linked to demand-supply dynamics in the U.S. and are less influenced by international seaborne prices. These contracts are of longer duration which provides the company more stability in terms of pricing, in contrast to the APAC region where pricing is closely linked to spot prices.

Cliffs’ recent announcement of a planned $700 million investment in a Hot Briquetted Iron plant (HBI) plant, which is expected to make the company the dominant supplier to the 3 million metric ton Electric Arc Furnace (EAF) steel market in the Great Lakes region by 2020, is further evidence of the company’s commitment to the US market. [3] The EBITDA margins and cash flows generated by this planned capacity addition would most likely match the EBITDA margins and cash flows of the company’s Australian operations. [4]

Greater Upside Probability of Iron Ore Prices in the U.S.

Steady recovery in the U.S. economy coupled with the possibility of the legislative enactment of $1 trillion infrastructure plan by President Trump could give a significant boost to the demand for steel. This would also translate into an improved demand and pricing outlook for iron ore in the region since iron ore is used as a raw material for steel production. In addition, the outcome of the investigation pertaining to steel imports under Section 232 of Trade Expansion Act of 1962 initiated by the Trump administration could further boost the prospects of the domestic iron and steel industry.

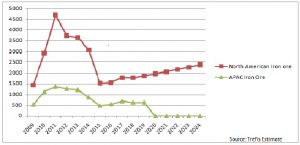

Given the favorable business environment in the U.S., focusing on the company’s U.S. operations is a sensible decision made by the company management. Since Cliffs has decided against developing its APAC reserves any further, the company’s APAC operations are most likely to cease operations by 2020 with the depletion of the company’s existing reserves, as illustrated by the chart shown below.

Revenue share by segment ($ million)

Thus, Cliffs is well on its way to becoming a pure-play U.S. iron ore producer.

Have more questions about Cliffs Natural Resources? See the links below.

- Cliffs Natural Resources’ Q2 2017 Earnings Review: Favorable Business Conditions In The U.S. Drive Earnings Growth

- Price Taker Versus Price Maker: The Perils Of Being An Iron Ore Producer

Notes:

See More at Trefis | View Interactive Institutional Research (Powered by Trefis)

Notes:- Cliffs Natural Resources Renames Itself Cleveland-Cliffs Inc., Cleveland-Cliffs news release [↩]

- CLF 2016 Annual Report, Cleveland-Cliffs website [↩]

- Cliffs Natural Resources Inc. Announces its First HBI Production Plant in the Great Lakes Region, Cleveland-Cliffs News Release [↩]

- Cliffs Natural Resources (CLF) Q2 2017 Results – Earnings Call Transcript, Seeking Alpha [↩]