Key Takeaways From Colgate-Palmolive’s Q3 Earnings

Colgate Palmolive (NYSE:CL) reported better-than-expected fiscal third quarter earnings, as its earnings per share were in line and revenue came in ahead of expectations. However, the company’s stock slid slightly after the announcement. Below we highlight some of the most notable items from the earnings release.

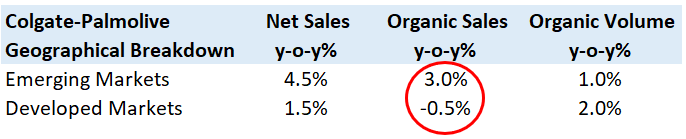

- Colgate’s net sales were up 3% year-over-year (y-o-y) in the quarter, with 1.5% volume growth, flat pricing, and a 1.5% foreign exchange benefit.

- The company’s organic sales growth grew 1.5% y-o-y in the third quarter, driven by healthy volume increases across Latin America, North America, and Europe.

- Almost 75% of Colgate’s net sales are generated from markets outside the U.S., with approximately 50% of the company’s net sales coming from emerging markets (which consist of Latin America, Asia (excluding Japan), Africa/Eurasia and Central Europe). In Q3, the company’s emerging markets grew 4.5% y-o-y, with organic sales up 3% y-o-y, driven by volume growth.

Relevant Articles

- Should You Pick Colgate-Palmolive Stock Over Monster Beverage After The Latter’s 2x Gains This Year?

- Should You Pick Colgate-Palmolive Stock After A Q3 Beat And 4% Gains This Month?

- Is Colgate-Palmolive Stock A Better Pick Over Marriott?

- Which Is A Better Consumer Defensive Pick – Kimberly-Clark Or CL Stock?

- Should You Buy Colgate-Palmolive Stock At $80?

- Should You Buy This Households & Personal Products Company Over Colgate-Palmolive Stock?

- On a GAAP basis, the company’s gross margin remained flat y-o-y at 60.4%, driven by cost savings from its Funding the Growth initiative and restructuring program, partially offset by higher raw material costs. Its operating profit margin was down 160 bps y-o-y to 24.8% in Q3, primarily due to growth in advertising investments and overhead expenses

- Going forward, Colgate-Palmolive continues to expect both its net sales and organic sales to increase at a low single-digit rate for the full year. The company also expects its full-year GAAP earnings per share to be down mid-single digits, and non-GAAP earnings per share to be down low-single-digit. In addition, the company expects its gross margin expansion to be in the range of 20 to 50 bps this year as compared to its previous outlook of the lower end of the 75 to 125 bps range. This reduction is due to a combination of higher raw material costs and less of a benefit from pricing in the first nine months of fiscal 2017.

Our $75 price estimate for Colgate-Palmolive is slightly ahead of the current market price.

See our complete analysis for Colgate-Palmolive

See More at Trefis | View Interactive Institutional Research (Powered by Trefis)