Nvidia Stock: A Path To $10 Trillion?

Nvidia stock (NVDA) growth story is expanding beyond GPUs. Customers increasingly buy complete AI systems that combine computing, networking, software, and services, giving Nvidia a larger share of AI infrastructure spending. That broader role is now extending into adjacent markets, including CPUs, where the company is making its first serious push to become a major supplier taking on the likes of AMD (AMD) and Intel (INTC). This trajectory gives the company a real shot at boosting its market cap to close to $10 trillion over the next few years.

Two forces could drive Nvidia’s next phase of growth. The first is the shift from training AI models to running them. Training is a periodic expense, while inference occurs every time a user interacts with an AI application. As AI becomes more deeply embedded in software and agentic systems handle increasingly complex tasks, demand for inference computing could grow rapidly. Nvidia is well positioned to capture that demand. Companies built on its CUDA software ecosystem face significant switching costs, and the upcoming Vera Rubin architecture is designed to improve inference efficiency by delivering more output with less power.

The second growth driver is Sovereign AI. Governments are increasingly investing in domestic AI infrastructure to keep sensitive data within national borders and reduce reliance on foreign technology providers. Nvidia’s full-stack offering of chips, networking, systems, and software makes it a natural partner for these projects. The opportunity is already meaningful: sovereign AI revenue more than tripled to over $30 billion in fiscal 2026. Beyond hyperscalers, governments and state-backed organizations could become another major source of AI infrastructure demand.

Layer the new CPU opportunity on top, and the revenue story becomes even more compelling. If these engines continue to compound, the top-line implications are significant.

- What Could Push NVDA Stock Higher From Here?

- MU, NVDA Look Smarter Buy Than MACOM Technology Solutions Stock

- NVIDIA Earnings: New Segments And A $200B CPU TAM Reveal A Business Beyond Hyperscale

- Does NVIDIA Stock Have More Upside?

- NVDA Stock: The Setup Hiding In Plain Sight

- Why NVDA, MU Could Outperform Rambus Stock

How Compounding Builds The Upside

Revenue is on track to grow by 80% this year and by close to 40% next year per consensus analyst estimates. If growth comes in at about 25% the following year, we would be looking at about $680 billion in revenue in FY’29. That’s about 47% annualized growth. Margins ease from 63.0% to 57.6% as today’s LTM gives back a little to the longer-run average. Together that takes earnings from $159.6B to roughly $395 billion, an almost 2.5x jump.

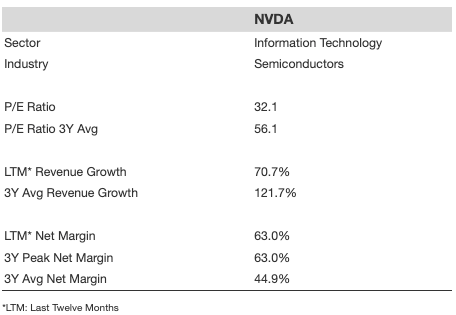

Here is where the stock and the earnings line diverge. NVDA’s P/E already sits at 32.1x, below its 3-year average of 56.1x. (See Nvidia’s valuation multiples) The scenario trims it further to 24.1x because a slower forward growth rate no longer supports even today’s multiple. That single move chews roughly 25% out of what the earnings growth would otherwise have delivered. Apply the lower multiple to the higher earnings, and the stock lands at over $390 per share, a market cap of $9.5 trillion against $5.1 trillion today. That is roughly 85% above where the stock trades now. The earnings line is doing the work; the multiple is taking a meaningful cut of it before it reaches the share price.

Has revenue compounding been the lever driving NVDA’s recent move? See the lever breakdown.

What Could Accelerate The Top Line

The new Vera CPU product line could push revenue growth beyond the current run rate. Management states Vera CPU opens a brand-new $200 billion TAM (Total Addressable Market) for the company. More concretely, the company already has visibility to nearly $20 billion in total CPU revenue this year alone. Combined with continued demand for AI GPUs, it gives Nvidia another lever to increase its share of overall data-center spending.

What Could Slow It Down

A significant geographic risk remains buried in the outlook. Management is explicitly not including any China data center compute revenue in its guidance. The company also concedes it has yet to generate any revenue from certain approved shipments to China-based customers.

Is The Compounding Real?

For the case to play out, the deceleration has to stabilize around 46% rather than continuing lower. The multiple is the other moving piece: the case trims it from 32.1x to 24.1x to reflect a slower forward growth rate, not any re-rating. If growth holds up better than projected, that compression reverses and the upside is larger.

The new revenue from the Vera CPU is a tangible catalyst that outweighs the already-excluded China data center business.

Should You Invest In NVIDIA?

A careful 3-year case on a single name is still a concentrated bet, as historical volatility across past market crises shows. Investors who build analyses like this on individual positions often want the same framework running across a diversified book, partly for discipline, partly because even the cleanest single-stock thesis can break for reasons the math does not capture.

The Trefis High Quality (HQ) Portfolio combines analytical rigor with a forward-looking view across 30 stocks, with a consistent selection framework and a sizing and rebalancing discipline designed to deliver upside without the single-name risk you just read through here.