The 60/40 Portfolio Is Dead; Here Is Its Replacement

Submitted by Sizemore Insights as part of our contributors program

The 60/40 Portfolio Is Dead; Here Is Its Replacement

by Charles Lewis Sizemore, CFA

- A 3x Expected Rise In Mounjaro Sales Is Likely To Drive Eli Lilly’s Q1

- What Should You Do With Danaher Stock At $250 After Q1 Beat?

- Will A Macau Recovery Drive MGM Stock Higher Following Q1 Results?

- Lockheed Martin Stock Will Likely Remain In Focus After A Stellar Q1

- Up 17% YTD, What To Expect From eBay Q1 Results?

- Rising 21% This Year, What Lies Ahead For Exxon Stock Following Q1 Earnings?

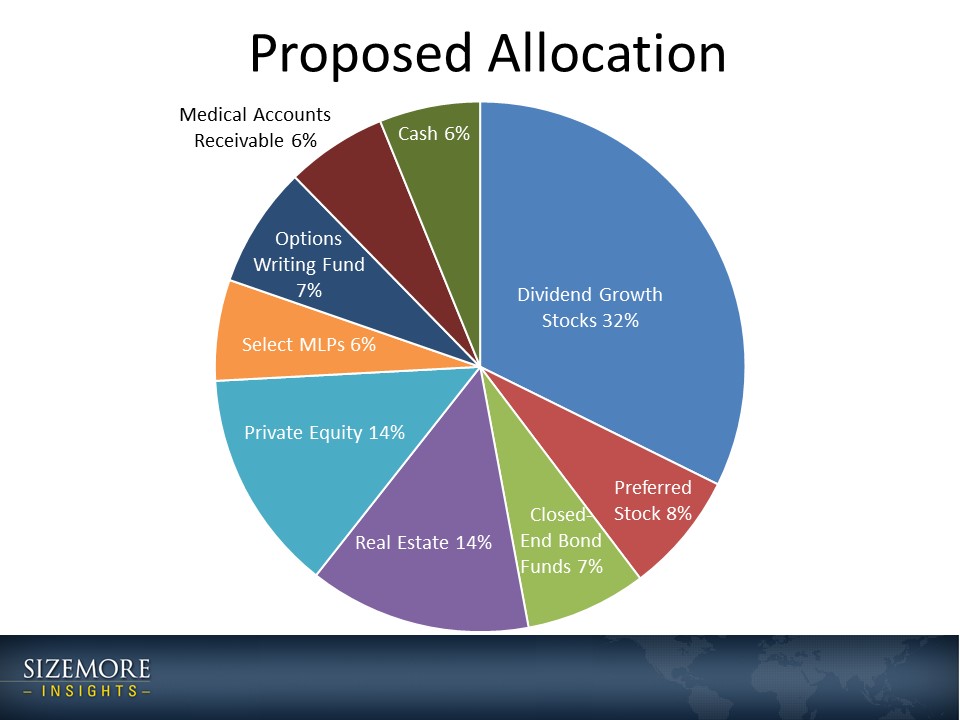

The following is a proposal I put together for a new client:

As you can see, we do things a little differently around here. Traditional stocks make up less than 40% of the portfolio, with the rest sitting in non-correlated assets outside of the stock market. We invest in everything from options-writing funds to medical accounts receivables and everything in between. The result is that we get most of the safety you would expect from a 60/40 stock/bond portfolio but without the loss of expected return. Our goal is to give you stock-like returns with the risk profile of a blended portfolio.

Why Invest in Alternatives?

You probably have a good grasp of why diversification is important. Throwing out the financial jargon, it essentially boils down to not putting all of your eggs in one basket. But it also gets a lot more sophisticated than that. Many investors feel that they have adequate diversification because their assets are spread across several stocks or mutual funds. And to an extent, they are right. Owning multiple stocks reduces the risk of downside from any single position.

But there is also a major problem with this: Correlation.

If Apple and Microsoft stock prices move together in lockstep, you’re not really getting much in the way of diversification by owning both. And in a real bear market, virtually all stocks drop together.

True diversification means owning assets that do not move together. Investment A can go up, down or sideways, and it should have little or no impact on Investment B.

This is where the beauty of an alternative portfolio comes into play. We can achieve “stock like” returns in the range of 7%-10% per year without the volatility that comes with stocks.

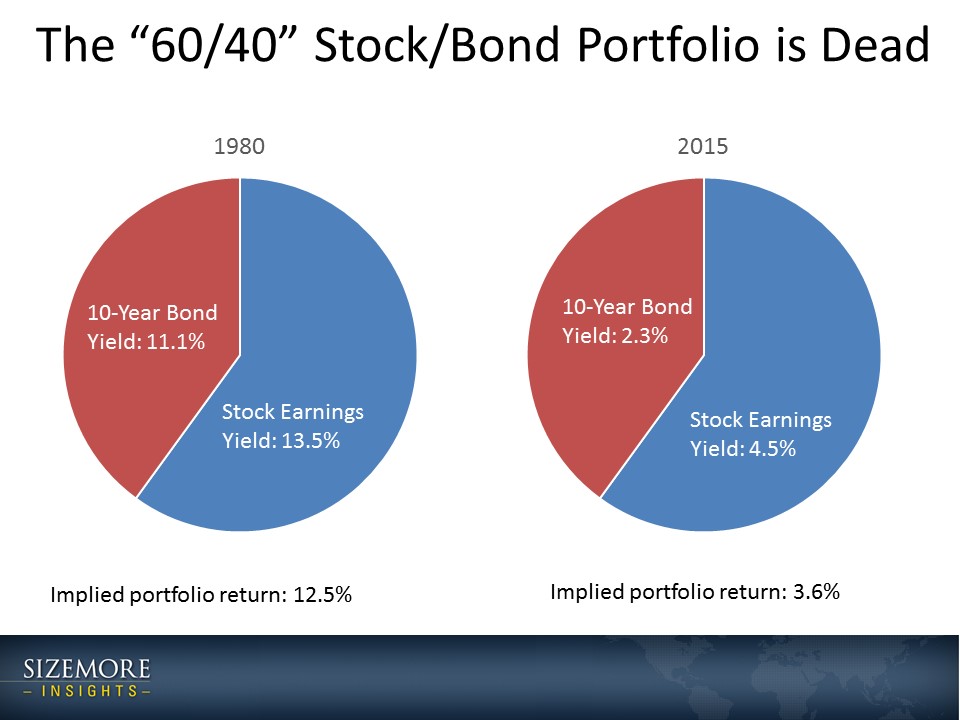

Why the 60/40 Portfolio is Dead

Alternative assets weren’t particularly popular in 1980. There is a reason for that. Back then, traditional bonds offered a respectable return. A blended 60/40 portfolio of stocks and bonds offered a solid expected return.

Flash forward to to present day. At current bond yields, investors will be lucky to get a 2% return in bonds. And compounding the situation, stocks are also expensive by historical measures and priced to deliver sub-par returns.

Accepting a traditional asset allocation is accepting disappointing returns in the years ahead. If you want better performance, we need to look elsewhere.

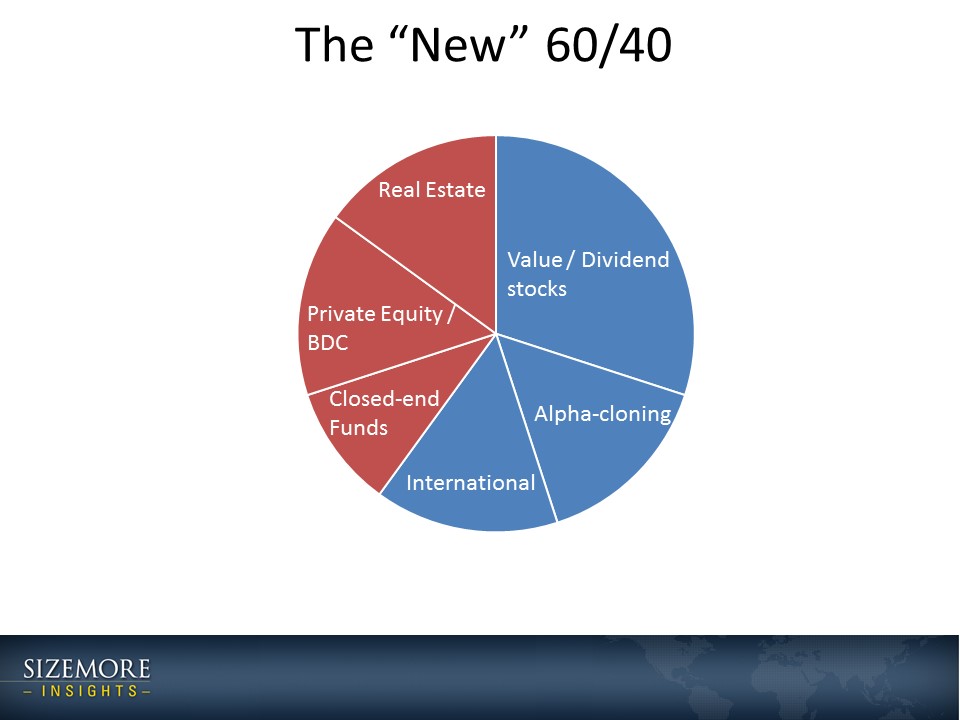

Introducing the New 60/40 Portfolio

Sizemore Capital Management custom builds portfolios based on the client’s preferences and eligibility. The following is a sample allocation:

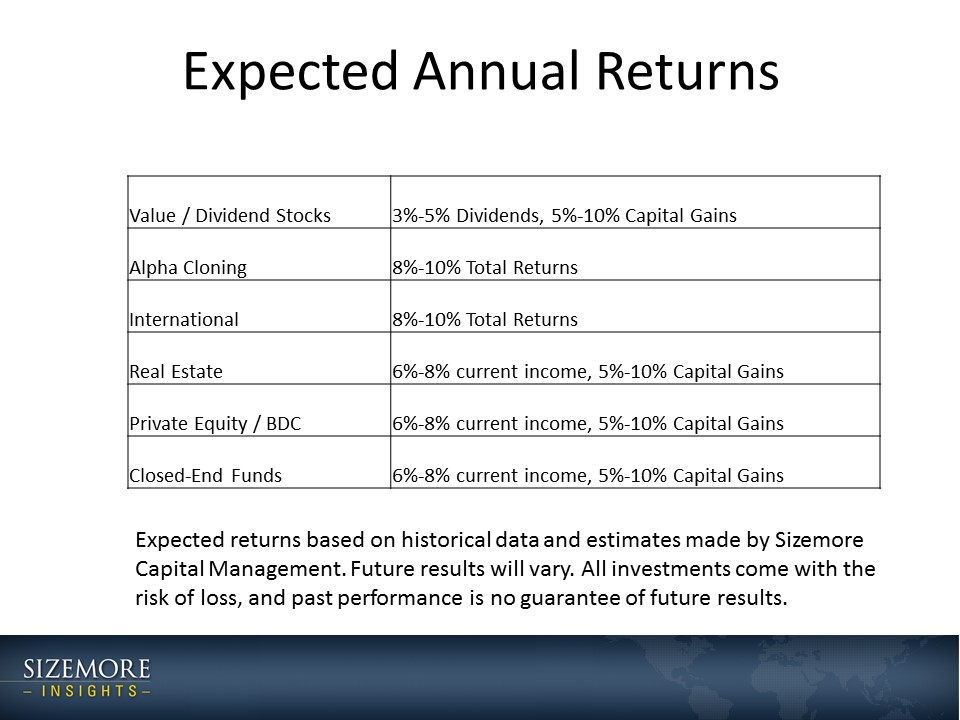

With the market looking overpriced and expected to deliver below-average returns, we need better alternatives. And thankfully, we have them. The following represent Sizemore Capital Management’s expected returns of the assorted asset classes in our model:

We should be clear that these are only estimates. Realized returns will vary and may be significantly higher or lower. But based on current valuations and historical performance, we consider these estimates reasonable.

We’re Not Alone

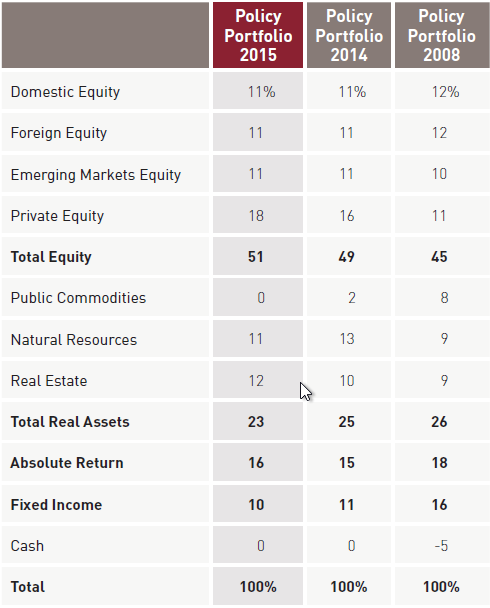

While ordinary investors have traditionally invested in stocks, bonds and CDs, wealthy investors and institutions have always had a broader allocation.Consider the case of the Harvard University endowment fund.

As of 2015, the Harvard endowment fund had only 3% of its funds in stocks. It has another 18% in private equity and 12% in real estate. The rest is spread across everything from timberland to absolute returns hedge funds. Let’s stop and ask an obvious question: If it’s good for trustees of Harvard, would it not also be good for you?

Not all of the alternative investments discussed will be appropriate for all investors. But we believe strongly that every investor can benefit from a proper allocation to alternative investments.

Charles Sizemore is the principal of Sizemore Capital Management.

This article first appeared on Sizemore Insights as The 60/40 Portfolio Is Dead. Here Is Its Replacement