Verisign’s Performance In 2017 So Far

Verisign (NASDAQ:VRSN) has had a decent 2017, with revenue of over $870 million in the first three quarters, an increase of nearly 2% year-on-year, primarily due to an increase in revenues from the operation of the registries for the .com and .net TLDs. This was driven by a 1% increase in the domain name base for .com, as well as the increase in .net domain name registration fees in February 2016 and 2017 by 10% each. With a contractual right to increase the fees by up to 10% each year during the term of its agreement with ICANN, through June 30, 2023, we expect Verisign to sustain its growth momentum going forward.

Our price estimate for Verisign is about 15% below the current market price.

Key Highlights:

- In the year so far, domain name registrations for .com and .net together grew 1% year over year to 145.8 million. VeriSign processed 27.6 million new domain name registrations for .com and .net, an increase from 0.7 million processed in the year-ago comparable period. Domain growth is primarily driven by the internet adoption rate, economic activity globally, e-commerce activity, and registrar go-to-market strategies.

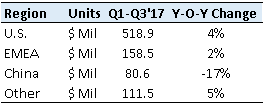

- In terms of geographical revenues, the U.S. and Europe, the Middle East and Africa (EMEA) regions continued their growth. However, revenues from China, which grew at a phenomenal rate over the past year owing to new registrations, slowed down in 2017. This was possibly driven by a lower renewal rate and unfavorable macro conditions.

- Despite 40% Rise This Year Is Akamai Stock A Better Pick Than VeriSign?

- Is FirstEnergy A Better Pick Than Verisign Stock?

- How Has VeriSign Stock Performed During The 2022-23 Inflation Shock?

- What’s Next For VeriSign Stock After A 20% Fall Since 2021?

- Forecast Of The Day: Verisign’s Number Of Domain Registrations

- Verisign Stock Has Underperformed Despite Steady Sales Growth – Here’s Why

The company holds a prime position in the highly regulated .com and .net domain industry. We expect the renewal of the .com contract and price hikes for .com and .net domain names will continue to push the top line going forward. Additionally, Verisign has the potential to greatly benefit from the significant growth opportunities in the Distributed Denial of Service (DDoS) security market.

For Q4 2017, the company expects to record revenues in the $291 million to $296 million range, while its non-GAAP operating margin is expected to be between 65.0% and 65.5% for 2017.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

More Trefis Research