Why DocuSign Stock Looks Like A Buy Despite 3x Rally

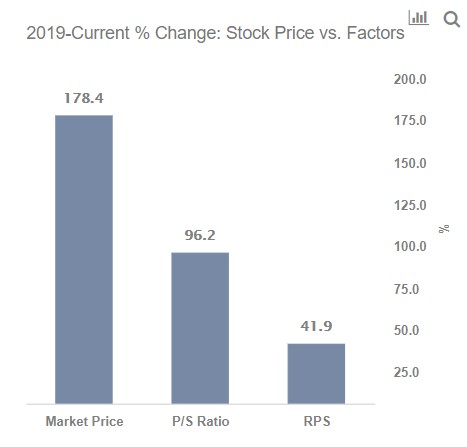

DocuSign (NASDAQ: DOCU), a company that provides online signature services, has seen its stock price rise by about 2.8x since the end of 2019 trading at levels of close to $205 per share, significantly outperforming the broader Nasdaq which was up by about 45% over the same period. The gains come on the back of a surge in demand through the Covid-19 pandemic, as organizations turned to the company’s software to sign and manage contracts and agreements digitally, instead of using a physical process, as employees worked from home. However, the stock has actually declined by roughly 22% from its February highs, driven by a broader correction in technology and “At Home” names. So is the stock a buy at current levels? We think so for a couple of reasons. Our dashboard What Factors Drove 2.8x Change In Docusign Stock Between 2019 And Now? provides the key numbers behind our thinking, and we explain more below.

What Has Driven DocuSign’s Stock?

DocuSign went public around mid-2018. Revenues rose from $701 million in 2019 (fiscal years end January), its first full year as a public company to about $974 million in 2020, an increase of about 39%. Growth rates accelerated to about 49% in FY’21, with sales rising to about $1.45 billion as the work-from-home trend caused demand to soar. Revenue per share also rose from around $5.20 in 2019 to $7.80 in 2021. DocuSign’s P/S (price-to-sales) ratio meanwhile rose from 14x in 2019 to levels of close to 40x in 2020, driven by stronger revenue growth in recent quarters, and higher valuations for software as service stocks. However, the multiple has declined to about 26x currently, driven by stronger revenue growth in 2021 and the recent correction in the stock price.

What’s the longer-term outlook for the stock?

DocuSign has a head start over the competition and has become synonymous with digital signatures. The company is also making inroads into areas such as contract management, enabling companies to manage the agreement process end-to-end digitally. The company’s revenues are also likely to be very sticky since they are largely subscription-based. DocuSign’s product is also easily integrated into existing business workflows, working with popular applications such as Salesforce, Slack, and SAP, potentially boosting customer loyalty. Although DocuSign trades at close to 20x projected 2022 revenues, we think the company’s strong growth outlook supports this valuation. Revenues are likely to expand by about 35% in 2022 and by about 30% in 2023, per consensus estimates. There are a couple of secular trends, such as greater levels of digitization and an increasing push toward the distributed workplace that could drive growth in the long run.

Looking for reasonably valued software stocks with big room to grow? Check out our theme on Mid-Cap SaaS Stocks

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams