Here’s How Growth In The Chinese Online Video Market Will Impact Baidu

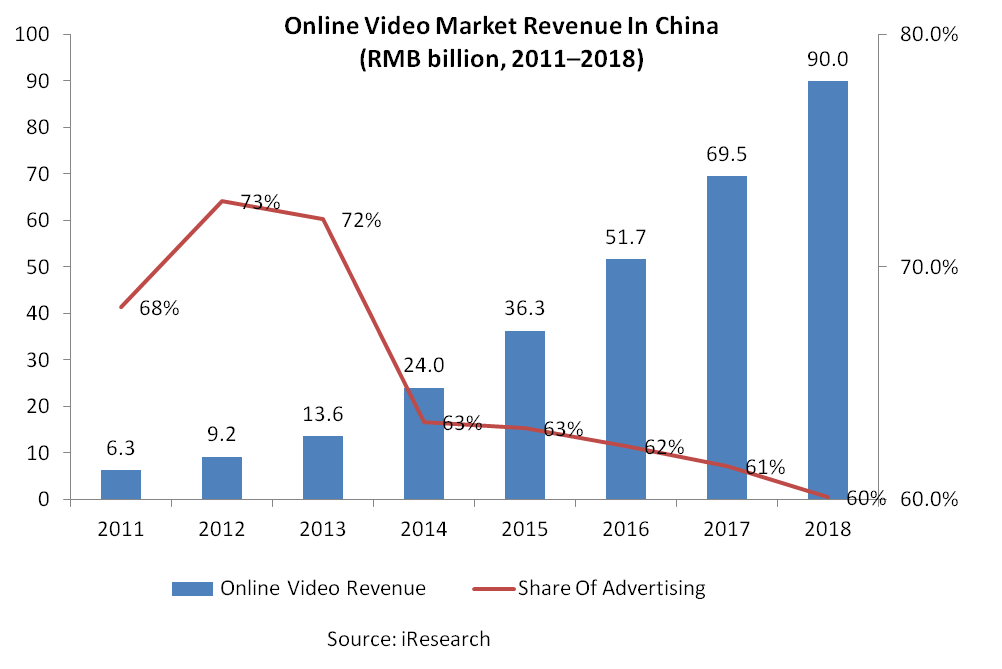

Baidu (NASDAQ:BIDU) is positioned among the key players in the Chinese online video market, as its Qiyi (online video) platform accounts for around 20% market share. Hence, we think the search-giant could capitalize heavily on future growth within the online video sector in China — where revenue is expected to rise 39% annually to reach $14 billion by 2018, according to iResearch (see below). As a result, we forecast online video segment to account for 10% of our valuation for Baidu, as revenues in this business could increase at around 25% annually over our forecast horizon.

See our complete analysis of Baidu here

China Online Video Revenues Could Reach $14 billion By 2018

As noted, according to iResearch (a Chinese market research firm), the online video market in China is estimated to rise at 39% CAGR during 2014-2018 to reach RMB 90 billion ($14 billion). While advertising will continue to remain the key driving force within this market, the share of other businesses (which includes value added services such as hardware sales and gaming revenues) in the overall market is expected to increase to 40% by 2018. [1] And though advertising revenues are presently derived mainly though copyrighted TV dramas and shows, the rapid surge in self-produced and mobile videos will also fuel this market, going forward, as per iResearch. The significant growth in video consumption across multiple devices (such as mobiledevices and tablets) in China is a key factor that will propel growth in this industry.

Competition Is Huge In The Online Video Market

According to Selerity Global Insight, the leading players in the Chinese online video market include Youku Tudou (Alibaba), iQiyi (Baidu), Tencent, and Sohu, with these participants having market shares of 21.7%, 19.6%, 14.1%, and 12.6%, respectively (as of Oct 2015). [2] Increased competition has contributed to substantial rise in content costs, as players generally bid aggressively for premium content. Moreover, companies including iQiyi are investing heavily in self-produced content to differentiate their services; during the third quarter of 2015, iQiyi had a 5.4% negative impact on Baidu’s overall non-GAAP margins. And, content costs accounted for 5% of Baidu’s revenues in Q3 2015, as compared to 3.7% in a similar period a year ago.

Online Video Comprises Around 10% Of Our Price Estimate

In our present valuation model, we estimate the online video business (including iQiyi) comprises about 10% of our $209 price estimate for Baidu’s stock. This is as we forecast revenues in this segment to rise from our $1 billion estimated for 2015 to nearly $5 billion by the end of our forecast period. Moreover, we think margins in this business could decline significantly in the near term due to a significant increase in content costs.

We encourage our readers to modify our estimates to see the impact on valuation. In the event revenues in this segment increase to $10 billion by the end of our forecast period (2022), it will take our price estimate around 10% higher to $227.

Our $209 price estimate for Baidu’s stock is broadly in line with the current market price.

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes:- 2015 China Online Advertising Report (Brief Edition), iResearch, May 25, 2015 [↩]

- Competition in China’s Online Video Market Intensifies, Selerity Global Insight, Oct 19, 2015 [↩]