US Steel Overvalued At $7?

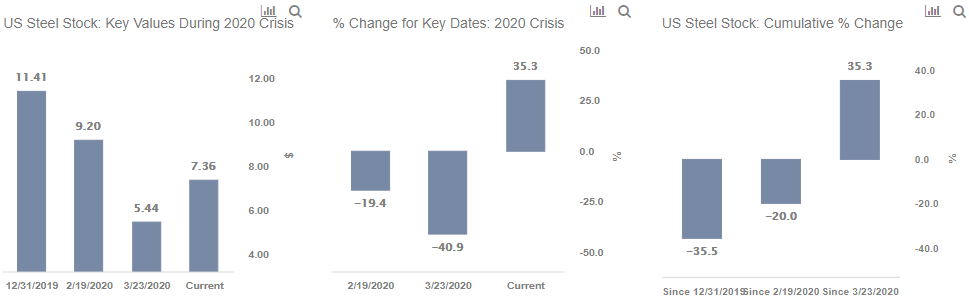

US Steel stock (NYSE: X) has rallied over 35% since late March (vs. about 42% for the S&P 500) to its current level of $7. This is after falling to a low of $5 in late March, as a rapid increase in the number of Covid-19 cases spooked investors, and resulted in heightened fears of an imminent global economic downturn. The stock is currently about 20% below its February 2020 high of $9.40. Are the gains warranted or are investors getting ahead of themselves? We believe that the stock has recovered more than its near-term potential, and think the stock price is likely to decrease from its current level. Our conclusion is based on our detailed comparison of US Steel’s stock performance during the current crisis with that during the 2008 recession in our dashboard analysis.

How Did US Steel Fare During 2008 Downturn?

- Can U.S. Steel Stock Return To Pre-Inflation Shock Highs?

- What’s Happening With U.S. Steel Stock?

- Will U.S. Steel Stock Continue To Outperform Despite Economic Headwinds?

- Is U.S. Steel Set For Tough Q3 Results?

- Why We Are Cutting Our Price Estimate For U.S. Steel Stock

- How Will U.S. Steel Stock Fare In An Uncertain Economy?

We see X’s stock declined from levels of around $107 in October 2007 (the pre-crisis peak) to roughly $17 in March 2009 (as the markets bottomed out) – implying that the stock lost as much as 84% of its value from its approximate pre-crisis peak. This marked a drop that was bigger than the broader S&P, which fell by about 51%.

However, X’s stock recovered post the 2008 crisis to about $58 in early 2010 – rising by about 243% between March 2009 and January 2010, as against the S&P which bounced back by about 48% over the same period.

In comparison, during the current crisis, X’s stock lost 41% of its value between 19th February and 23rd March 2020, and has already recovered 35% since then. The S&P in comparison fell by about 34% and rebounded by over 42%.

Is The Recovery Warranted & Can We Expect Further Gains?

The global spread of coronavirus has led to lockdown in various cities across the globe, which has affected industrial and economic activity. The steel demand from industry players affects global steel price levels, in turn impacting the company’s price realization for its products. Lower demand from construction and automobile players, has led to a drop in global steel prices recently, which had already seen a drop due to the ongoing US-China trade war. This as reflected to a certain extent in the company’s Q1 2020 results, where US Steel’s revenues saw 21% decline and margins of -14.2%. Q2 2020 is expected to be worse with the full impact of the crisis being felt during the quarter.

However, over the coming weeks, we expect continued improvement in demand and subdued growth in the number of new Covid-19 cases in the U.S. compared to the rate seen in April-May to boost market expectations. Additionally, the gradual lifting of lock downs is also giving investors confidence that developed markets have put the worst of the pandemic behind them. Following the Fed stimulus — which helped set a floor on fear — the market has been willing to “look through” the current weak period and take a longer-term view, with investors now mainly focusing their attention on 2021 results.

US Steel’s stock recovered recently on expectations of a rise in global steel prices as major economies started lifting lock downs gradually, which could likely lead to increased demand and lower supply bottlenecks. The US raw steel capacity utilization for the week ending 4th July 2020 was 56.6%, which is significantly lower than 80.1% recorded in the prior year period. However, this is an improvement over the 51% utilization in the beginning of May 2020, which indicates that there are signs of a rebound in activity in the steel sector.

However, company-specific operational challenges remain. Even if the steel market recovers anytime soon, we do not believe that US Steel would be able to reap as much benefit out of this recovery as its peers like ArcelorMittal. Even during such a difficult crisis, US Steel is burning a lot more cash than its peers. The company’s flat-rolled segment asset revitalization program, that aims to increase productivity and reduce cost in the long term, has led to a planned outage at its Great Lakes Works facility. The $2 billion program is expected to add $275-$375 million to the company’s EBITDA annually in the medium term, but is eating up a lot of cash currently. US Steel’s free cash flow decreased drastically from about $450 million in 2016 to -$470 in 2019, reflecting a net cash outflow. At the same time, the company’s cash balance halved from $1.5 billion to $750 million.

Though the stock rebounded due to broader sector and economic developments, we believe that the stock has reached its near-term potential and could see a marginal downside. As per US Steel Valuation by Trefis, we have a fair price estimate of $6 for the company’s stock, lower than its current market price of $7.

So, while US Steel seems to have a modest downside from its current level, which S&P 500 component stocks have the best chance of outperforming the benchmark index? Our 5 In the S&P 500 That’ll Beat The Index: TWTR, ISRG, NFLX, NOW, V look promising.

For further insight in the steel sector, see how ArcelorMittal compares with US Steel.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams