Despite 75% Jump, Weight Watchers Stock Has Scope For More

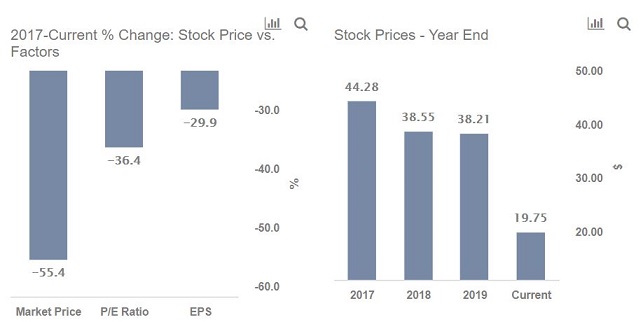

Despite a 75% rise since the March lows of this year, at the current price of around $20 per share we believe Weight Watchers stock (NASDAQ: WW) has more room to go. Weight Watchers’ stock has rallied from $11 to $20 off the recent bottom compared to the S&P which moved 48% over the same time period. Strong growth in the digital business, with digital subscribers reaching an all-time high in June as well as gradual re-openings of studio locations, has led to the stock beating the overall market. However, the stock is down 55% from levels seen in early 2018, over two years ago. Additionally, the company’s stock is down nearly 48% to the figure it was at in February before the drop due to the coronavirus outbreak becoming a pandemic. Despite the steady rise since the March 23 lows, we feel that the company’s stock still has potential as it will see an upswing in its studio business as the situation normalizes and its valuation implies it has further to go. Our dashboard ‘Why Weight Watchers Stock moved -55%?’ provides the key numbers behind our thinking, and we explain more below.

Some of the stock price decline over the last two years is justified given that the company’s earnings per share figure has shrunk nearly 30% due to a sharp reduction in margins. Moreover, a 4.4% increase in share outstanding further contributed to this share price decline. Notably, though, the company’s revenues have seen a healthy 8.1% growth between 2017 and 2019.

- Down 70% Since 2021, Can A Revival In Subscriber Growth Help WW International Stock Recover?

- Can WW International Recover To Its Pre-Inflation Shock Highs?

- WW International Stock Is A Buy Following Sequence Deal

- Is WW International Stock Still Good Value Post The Recent Rally?

- Down 75% This Year, What’s Next For WW International Stock?

- Is WW International Stock A Buy At $4.50?

Finally, Weight Watchers’ P/E multiple expanded from 17x at the end of 2017 to 22x by the end of 2019. While the company’s P/E has decreased to 11x, it seems to be undervalued when the current P/E is compared to levels seen in the past years – P/E of 22x at the end of 2019 and 17x as recently as late 2017. We believe the stock is likely to witness a steady upside despite the recent rally and the potential weakness from a recession-driven by the Covid outbreak.

How Is Coronavirus Impacting Weight Watchers’ Stock?

The outbreak of Coronavirus has rattled the stock market and the broader economy. The pandemic, coupled with a broader economic slowdown, has adversely impacted consumer spending in the wellness and fitness industry. As people stayed home and avoided public places, the company’s high-margin studio business took a hit. This was evident from the fact that the company saw a 27% decrease in the studio revenues while the company’s digital business remained robust, with digital revenues surging by more than 13% in Q2 2020 earnings (ending June). Further, the company’s digital member signup trends have remained upbeat, with digital subscribers reaching an all-time high of 3.9 million. Moreover, Weight Watchers has a strong retention rate, which is likely to mitigate the impact on the company’s top line. Despite a strong retention rate and a robust digital business, we expect Weight Watchers’ revenues to witness year-over-year declines in 2020 due to the steep fall in its studio business. To sum things up, although Weight Watchers’ revenues are likely to be lower in FY’20, Weight Watchers’ stock currently seems undervalued due to its upbeat digital business and a strong retention ratio.

Moreover, over the coming weeks, we expect continued improvement in demand and subdued growth in the number of new Covid-19 cases in the U.S. to buoy market expectations. Following the Fed stimulus, which set a floor on fear, the market has been willing to “look through” the current weak period and take a longer-term view, with investors now mainly focusing their attention on 2021 results.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio to beat the market, with over 100% return since 2016, versus 55% for the S&P 500. Comprised of companies with strong revenue growth, healthy profits, lots of cash, and low risk, it has outperformed the broader market year after year, consistently.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams