Should You Buy Walgreens Stock Over This Retailer?

We believe that Walgreens Boots Alliance stock (NYSE: WBA) currently appears to be attractive compared to its peer Target stock (NYSE: TGT), due to its comparatively lower valuation and better growth prospects. WBA trades at about 0.3x trailing revenues, compared to 1.1x for TGT. Although both the companies saw a rise in revenue over the recent quarters, the growth has been better for Target, aided by the overall economic recovery and a rise in consumer spending. Looking at stock returns, WBA, with 9% returns over the last six months, has outperformed TGT, which is down 5%, and it has performed in-line with the broader markets, with a 10% rise for the S&P500 index. However, there is more to the comparison, and we believe that both of these stocks are best avoided for now. We compare a slew of factors such as historical revenue growth, returns, and valuation multiple in an interactive dashboard analysis Walgreens vs Target: Which Stock Is A Better Bet? Parts of the analysis are summarized below.

1. Target’s Revenue Growth Has Been Stronger

- Target’s revenue growth over the last twelve month period was stronger than Walgreens (18% vs. 9%), given a sharp rebound in economic growth.

- Target saw an increase in spending in attractive categories like apparel, toys, and home furnishings. The company has also benefited from its drive-up, pickup in-store, and same-day delivery via Shipt services.

- For Walgreens, the revenue growth was partly driven by increased demand for Covid-19 testing as well as vaccine administration.

- Even if we were to look at the three-year average revenue growth, Target’s last three year CAGR of 9% is higher than just 0.5% for Walgreens.

- With the Omicron variant spreading across the globe, the demand for Covid-19 booster shots is on the rise, implying that Walgreens may benefit from vaccine administration in the near term.

- Looking forward, Walgreens revenue growth rate is expected to see a low single-digit rise in 2022, in-line with the growth estimates for Target’s sales.

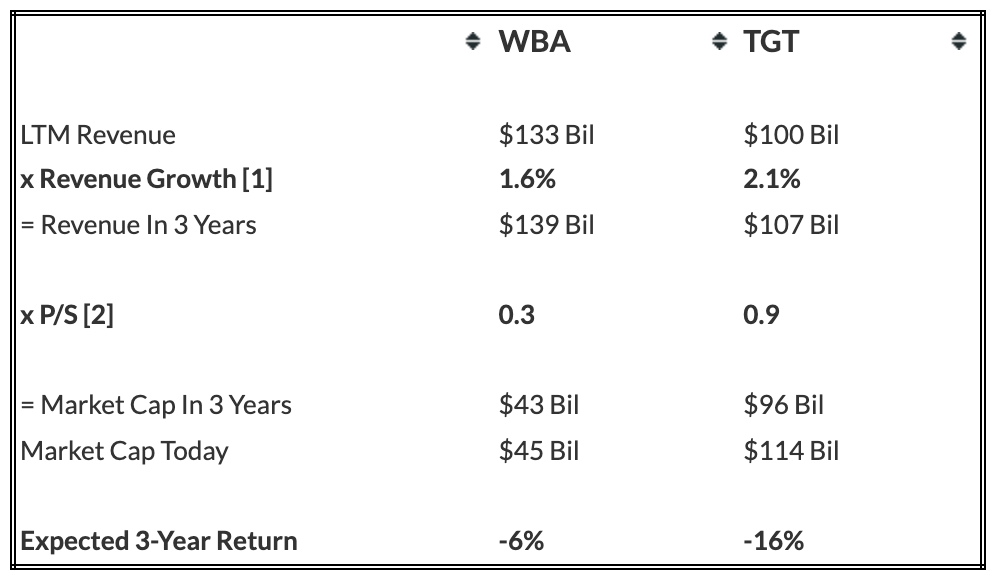

- The table below summarizes our revenue expectation for WBA and TGT over the next three years, and points to a CAGR of 1.6% for Walgreens, slightly lower than a CAGR of 2.1% for Target. Also, our Walgreens Revenues dashboard provides more insight on the company’s revenues.

- Should You Pick Walgreens Stock At $20?

- After A 4% Fall Last Year Is Target A Better Pick Over Walgreens Stock?

- Will Walgreens Stock Rebound To Its Pre-Inflation Shock Level of Over $50?

- What’s Next For Walgreens Stock After A 9% Fall Yesterday?

- Is Walgreens Stock Undervalued At $32?

- What To Expect From Walgreens’ Q2?

2. Target Is More Profitable

- Looking at profitability, similar to the trend seen in revenue growth, Target’s operating margin of 9% over the last twelve month period is much better than 2% for Walgreens.

- This compares with 6% and 4% operating margin seen in 2019, before the pandemic, respectively.

- Even if we were to look at the last three year average operating margin, Target’s 6% figure is better than just 3% for Walgreens.

The Net of It All

- Now that over 60% of the U.S. population is fully vaccinated against Covid-19, with overall economic activity picking up, the demand for Covid-19 vaccine administration may see slower growth, impacting the pace of revenue growth for Walgreens, in particular.

- That said, Covid-19 is proving more difficult to contain than initially thought, due to the spread of more contagious virus variants and infections in many geographies, including the U.S. and Europe, are higher than what they were a few months back.

- The concerns around Omicron have spooked the markets at large. If there is another large spike in Covid-19 cases from the new variant, it will disrupt economic recovery, but at the same time, it will likely result in a continued demand for Covid-19 testing and a rise in demand for booster shots, bolstering near term revenue growth for Walgreens.

- If we were to look at financial risk, Target’s 10% debt as a percentage of its equity and 14% cash as a percentage of assets are better than 20% and 1% for Walgreens, respectively, implying that TGT stock has lower financial risk compared to WBA.

- Despite better revenue growth, operating margins and lower financial risk for Target, we find Walgreens’ current valuation to be seemingly more attractive, with TGT stock trading at about 1.1x trailing revenues, versus just 0.3x for WBA stock.

- Overall, going by performance over the recent years, Target may appear to be a better bet. However, if we were to look at the future outlook, Walgreens seems to have better prospects with its revenue rising at a slightly faster pace compared to Target.

- That said, we believe that both the stocks are likely to see lower levels over the next three years, going by expected changes to the P/S multiple. The table below summarizes our revenue and return expectation for WBA and TGT over the next three years, and points to an expected return of -6% for WBA over this period vs. -16% for TGT, implying that both the stocks are best avoided for now. Our dashboard Walgreens vs Target has more details on how we arrive at these numbers.

What if you’re looking for a more balanced portfolio instead? Here’s a high-quality portfolio that’s beaten the market consistently since the end of 2016.

Invest with Trefis Market Beating Portfolios

See all Trefis Price Estimates