Visa Rally is Over

After a 40% rally off the March bottom, Visa’s stock (NYSE: V) looks fully valued based on its historic PE multiples. Visa’s stock has rallied from $136 to $189 off the recent bottom compared to the S&P, which moved by almost 45%. The stock is slightly lagging the overall market as investors are cautious about the impact of lower consumer demand on its transaction volumes. However, it is still up 10% from levels seen in late 2019.

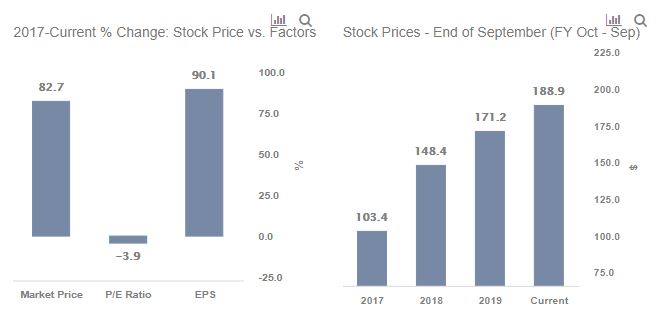

Visa’s stock has almost fully recovered to its all-time high of around $210 before the drop in February due to the coronavirus outbreak becoming a pandemic. While the company has steady revenue and earnings growth over recent years, its PE multiple has decreased. We believe the stock is unlikely to see a significant upside after the recent rally and the potential weakness from a recession that is driven by the Covid outbreak. Our dashboard ‘Why Visa Stock moved 82.7% between 2017 and now’ has the underlying numbers.

Some of this rise of the last two years is justified by the roughly 25% growth seen in Visa’s revenue from 2017 to 2019, which translated into an 80% growth in Net Income figure. Notably, the effective tax rate was around 43% in 2017 due to the one time impact of the U.S Tax Act, which weighed on the margin figure. However, the effective tax rates decreased to around 20% and 19% respectively in the subsequent years, improving the margin figure from 36.5% in 2017 to 52.6% in 2019.

Visa’s PE multiple changed from around 37x in 2017 to 32x at the end of 2019. While the company’s PE has improved to about 35.5x now, there is a possible downside when the current PE is compared to levels seen in the past years – PE of 32x at the end of 2019 and the high of 33.5x in late 2018.

So is an upside likely, and what’s the possible trigger?

Due to the possible impact that the outbreak and a broader economic slowdown could have on consumer spending and the global payments processing industry, Visa stock has suffered in recent months. The company derives around 27% of its revenues from international transactions; travel bans and widespread panic due to Coronavirus outbreak could severely impact this revenue stream. Further, lower consumer spending would result in lower transaction volume leading to lower data processing fees, which contributes around 35% of the company’s revenues. While the company’s result for the Q1 2020 saw some increase in revenues, we believe Visa’s Q2 results in July will confirm the hit to its revenues. It is also likely to accompany a lower Q3 as-well-as 2020 guidance.

However, over the coming weeks, we expect continued improvement in demand and subdued growth in the number of new Covid-19 cases in the U.S. to buoy market expectations. Following the Fed stimulus – which set a floor on fear – the market has been willing to “look through” the current weak period and take a longer-term view. With investors focusing their attention on 2020 results, the valuations vs. historic valuations become important in determining value. That said, market sentiment can be fickle, and evidence of an uptick in new cases could spook investors once again.

While Visa’s stock has limited upside potential, we found a lot of strength in Discover Financial’s stock.

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams