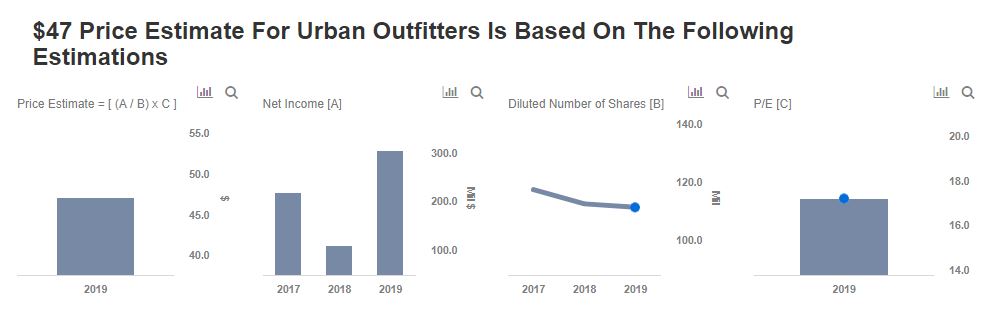

Why Urban Outfitters Is Worth $47

Urban Outfitters (NASDAQ: URBN) has reported robust top line and bottom line performance through the first three quarters of fiscal 2019, driven by solid comps sales growth – largely due to strong growth in the digital segment. The apparel retailer’s revenue grew by nearly 12%, while its earnings more than doubled to $1.92 (vs. 94 cents in the comparable prior year period). Further, the company reported substantial growth in all three of its brands, seeing positive comps for each of them in all three quarters reported in FY 2019, as a result of increased average unit selling price and higher units per transaction. Additionally, improved sales and reduced markdowns helped boost margins which, coupled with a substantial decline in tax rate, helped boost the earnings. Given the promising underlying trends and the robust holiday season, we expect a strong finish to URBN’s FY 2019.

We have a price estimate of $47 per share for the company, which is higher than its current market price. View our interactive dashboard – Urban Outfitters’ Outlook For 2019 – and modify the key drivers such as revenue and margins to gauge the impact on the company’s valuation.

- Up 52% YTD, Where Is Urban Outfitters Stock Headed?

- Urban Outfitters Stock To Likely See Little Movement Post Q2

- Urban Outfitters’ Stock To Likely See Little Movement Past Q1

- What’s Happening With Urban Outfitters’ Stock?

- Will Urban Outfitters Stock Move Lower Post Fiscal Q2 Results?

- What To Watch For Urban Outfitters Stock Past Earnings?

Factors That Should Drive Future Performance

1. Strong Sales Trend: URBN’s retail segment has been a consistent performer for the company and reported mid-single digit comps growth in the fourth quarter-to-date. This solid growth is attributable to strong comp sales growth across – Free People, Urban Outfitters, and Anthropologie brands. Further, a healthy economy, improved consumer confidence, and low unemployment, which has prompted positive sales trends in the first three quarters, should continue to benefit the company in the near term. Moreover, the factors that helped the gross margin – reduced markdowns and leverage in store occupancy costs – should spill over into Q4, helping the company post an improvement in the metric by a similar amount as in Q3.

2. Digital Segment Potential: URBN’s digital sales contribute about 40% of its total retail sales, highlighting a marked shift towards the online space. In addition, all three brands reported double-digit sales increases, with Free People and Anthropologie benefitting the most due to this shift. Digital penetration in these brands has increased to well over 50%. To leverage this online opportunity, URBN re-platformed its website, enabling better functionality for customers, including in-store pick-up capabilities, improved delivery options, a more responsive site, faster load times, and the addition of Apple Pay and Afterpay as alternative payment methods. Further, the company is also concentrating on enhancing its loyalty and rewards programs. We expect these strategic initiatives to drive URBN’s revenue in the near term.

3. Addition Of Anthropologie In Wholesale: Urban Outfitters, in partnership with Nordstrom, launched Anthropologie home wholesale in North America, following the success of Anthropologie wholesale in the U.K. last financial year. The brand is currently available in 19 Nordstrom stores and online, along with select assortment in an additional 60 stores and further expansion can be anticipated by the end of the year. This should help drive wholesale revenues. Further, we see significant opportunity for Free People wholesale to expand its presence in the domestic business through category expansions – FP Movement and denim. In Q3, the Urban brand also entered wholesale with the launch of its BDG collection through nordstrom.com domestically and Zalando in Europe. As a result, this should provide for decent medium-term opportunities.

4. International Growth Potential: URBN believes Anthropologie has the potential to derive half of its sales from outside the United States in the long term. Currently, almost all of the international sales are obtained from the U.K., and is in the process of expanding in other countries. The brand opened two new stores in the Q2 – one in Europe and one in North America – and a third franchise store in Ashdod, Israel. Further, URBN plans to open additional stores in Europe, as well as several additional franchised stores in Israel. For its Free People brand, the company opened its first store in Amsterdam early in the fourth quarter, and intends to open a store in London before the end of the financial year. In Europe, the retailer plans to open 10 to 20 new stores across all brands in each of the next two years. With a current base of 61 stores, the plan is for its European store count to exceed 100 in three years. We expect the concentrated efforts to expand its international reach should drive significant long-term opportunities.

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.