2015 Earnings Review: United Continental Posts Record Full Year Profits, Thanks To Lower Fuel Costs

Despite the frequent changes in top management, United Continental’s (NYSE:UAL) 2015 earnings more than doubled compared to last year, driven by the huge fuel cost savings realized during the year. However, currency tailwinds and lower surcharges in the international markets during the year, led to a sharp decline in the airline’s unit revenue, pulling down its top line. While the airline foresees the weakness in unit revenue to persist in the first quarter of 2016, it expects lower fuel costs to bolster its margins. The Chicago-based airline will continue to return higher value to its shareholders and revamp its fleet of aircraft to leverage the increased cash flows. Overall, the network carrier aims to improve its operational performance and control its non-fuel costs to maintain its profitability over the long term. In this note, we highlight the major trends witnessed in the airline’s latest earnings release.

Source: Google Finance

Currency Headwinds Drag Down Unit Revenue

- Spurred By Stellar Earnings, Can United Airlines Holdings Stock Extend Its Run?

- United Airlines Holdings Stock Looks Set For A Come Back

- Down 13% Last Week, Can United Airlines Holdings Stock Bounce Back?

- Is United Airlines Stock On The Move?

- Company Of The Day: United Airlines

- Will United Airlines Stock Rise After Recent Correction?

Due to the fear of an oversupply of seats in the market, United expanded its capacity by only 1.6% on a year-on-year basis, while its passenger traffic grew 1.5% during the year. However, its load factor (occupancy rate) dropped marginally to 83.4%, which is notably lower than its closest competitor Delta. Further, the US dollar strengthened against the other currencies in the last three quarters of 2015, creating a dent in United’s unit revenue, which, in turn, led to a steep fall in the airline’s international revenue. This, along with a fall in air travel due to the Paris attacks in the last quarter of 2015, caused the airline’s unit revenue to drop by 4.4% in 2015 compared to 2014. As a result, the airline saw a 2.7% reduction in its total revenue [1].

Fuel Cost Savings Continue To Boost Bottom Line

Due to the over 50% plunge in crude oil prices in 2015, United’s fuel expense fell approximately 35% resulting in cost savings of almost $4 billion for the full year. Also, the airline managed to reduce its non-fuel unit cost by 0.7%, augmenting the margins. However, the airline’s policy to hedge a portion of its fuel consumption, and labor contracts, marginally offset the impact of lower fuel costs. Yet, the network carrier delivered net income (excluding special items) of $4.5 billion, or $11.88 per share, which is the highest in the history of the airline. Thus, the year 2015 was a record year for the airline.

See Our Complete Analysis For United Continental Here

Returning Value to Shareholders

Given the fuel costs savings, United generated operating cash flows of $6 billion in 2015. In order to pass the benefit of falling fuel costs on to its shareholders, the airline spent $1.2 billion in buying back its shares. Further, the network carrier aims to spend $750 million on the share repurchase program in the first quarter of 2016 and plans to complete its $3 billion share buyback program during this year. In addition, the airline prepaid $1.2 billion of its long-term debt, reducing its long-term obligations to $17 billion. United also contributed close to $800 million to its pension fund in 2015 and targets to contribute at least $400 million to its pension fund in 2016.

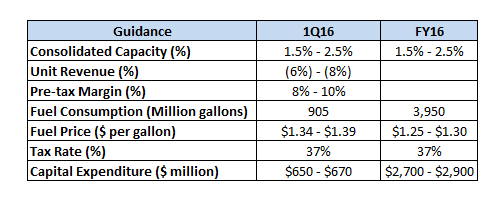

Guidance for 1Q16

United expects the currency headwinds to continue in the first quarter of 2016. Consequently, it anticipates a reduction of 6% to 8% in its unit revenue in the March quarter, with domestic markets causing a drop of 4% to 6%, with the international markets falling 8% to 10%. On the capacity front, the network carrier will continue to restrict its capacity additions to 1.5% to 2.5% in the next three months. United will re-position its capacity in markets that have strong demand, and generate higher margins and maintain its full year capacity target in the range of 1.5% to 2.5%. On the cost side, United plans to prevent its unit costs (excluding fuel, profit sharing, and special items) from growing more than 1% during 2016. Moreover, the airline has hedged approximately 17% of its fuel consumption for 2016 and is subject to hedging losses of approximately $225 million. While the hedging losses are likely to eat into the airline’s profits, the airline estimates its pre-tax operating margin to be between 8% and 10% in the first quarter of 2016.

In conclusion, we expect United to continue to ride high on the back of depressed fuel prices at least for the next few quarters. However, the airline’s operational performance and re-fleeting program will play a crucial role in driving its long-term value.

View Interactive Institutional Research (Powered by Trefis):

Global Large Cap | U.S. Mid & Small Cap | European Large & Mid Cap

Notes:- United Announced 2015 Results, 21st January 2015, www.unitedcontinentalholdings.com [↩]