What To Expect From Tesla’s Full-Year 2019 Earnings

Tesla (NASDAQ: TSLA) will release its Q4 and full-year 2019 results on Wednesday, January 29. We expect the company’s EPS to come in at -$0.25, beating the consensus estimates of -$0.27, driven by relatively strong revenue growth and better cost management. Trefis estimates Tesla’s 2019 revenues at $24.6 billion, marginally ahead of the consensus estimate of $24.5 billion. Earlier this month, the company published its quarterly delivery figures, indicating that it sold a total of ~367k cars for 2019, making good on its promise of delivering over 360k cars for the year. Our interactive dashboard analysis for Tesla’s pre-earnings details our expectations from the company, parts of which we highlight below.

Revenues are expected to be slightly ahead of consensus

- Trefis estimates Tesla’s 2019 revenues to be $24.6 billion, slightly ahead of the consensus estimate of $24.5 billion

(1) Automotive $21.3 Bil (86%)

- How Will Tesla’s Earnings Trend After A Tough Q1 Delivery Report?

- With Deliveries Falling And Inventory Piling Up, What’s Next For Tesla Stock?

- Down Almost 20% This Year, Is Tesla Stock Good Value?

- Down 9% Year-To Date, Will A Q4 Earnings Beat Drive Tesla Stock Higher?

- With Delivery Growth Cooling, Is Tesla Stock Still A Buy At $250?

- Following A Lackluster Cybertruck Debut, Is Tesla Stock Overvalued At $240?

(2) Service Revenue $1.7 Bil (7%)

(3) Energy $ 1.6 Bil (7%)

———————————————–

TOTAL $24.6 Bil

Consensus $24.5 Bil

Surprise +$0.1 Bil

- Total Revenue is expected to increase by 15% from $21.5 billion in 2018 to $24.6 billion in 2019.

- The growth is likely to be primarily driven by the automotive business, with automotive revenues likely to grow from $18.5 billion in 2018 to $21.3 billion in 2019, driven primarily by higher Model 3 deliveries.

- We expect the energy and services businesses to also see a modest increase in revenues.

- For more details on Tesla’s revenues, view our interactive analysis: Tesla Revenues: How Does Tesla Make Money?

EPS likely to narrowly beat consensus estimates

- Tesla’s 2019 earnings per share (EPS) is expected to be -$0.25 per Trefis analysis, slightly better than the consensus estimate of -$0.27

Total Revenues $24.6 Bil

– Total Expenses $24.65 Bil

————————————————-

Net Income -$45 Mil

÷ Shares Outstanding 174 Mil

————————————————-

EPS ($0.25)

Consensus ($0.27)

Surprise +$0.02

* Numbers do not line up due to rounding

- Tesla’s EPS is likely to increase from -$1.33 in 2018 to -$0.25 in 2019, as Revenues are likely to grow slightly faster compared to total expenses.

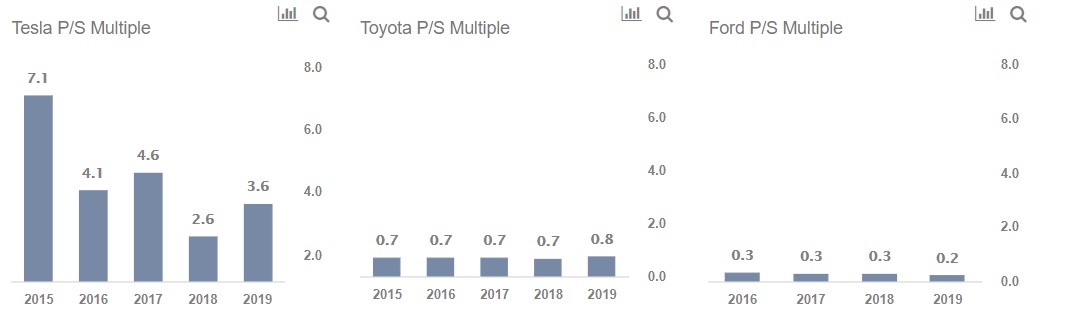

Trefis Stock price estimate for Tesla is significantly behind the market

- As we expect Tesla to remain loss-making for FY’19, we are valuing the company using a revenue multiple for the purpose of this analysis.

- Trefis’ forecast for Tesla’s 2019 revenue per share is slightly higher than the market estimates, although the P/S multiple is significantly lower and we value the stock at $348 versus the market price of about $510.

- Our stock price estimate is based on a trailing P/S multiple of 2.5x, which looks appropriate for Tesla’s stock. However, it is significantly lower compared to the implied P/S multiple of about 3.6x.

- For more details view our interactive analysis: Tesla Valuation: Expensive Or Cheap?

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams