A Closer Look At Tesla’s Q3 Delivery Figures And What They Could Mean For Its Earnings

Tesla (NASDAQ: TSLA) posted record deliveries of 97,000 vehicles in Q3’19, marking a sequential increase of about 1,800 units, although they came in below Street expectations. The Model 3 saw sales rise by about 2k sequentially to 79,600 units, premium vehicles continued to underperform, with deliveries dropping slightly to 17,400 units. This puts the company’s year-to-date deliveries at ~255k. For perspective, Tesla previously guided 360k to 400k units for 2019, indicating that deliveries over Q4 would need to grow 8% sequentially to meet the lower-end of the annual target. Below we take a look at some of the trends that likely drove deliveries and how it could impact Tesla’s Q3 earnings, which are likely to be published by the end of this month.

View our interactive dashboard analysis on A Look At Some Of The Trends That Drove Tesla’s Q3 Deliveries

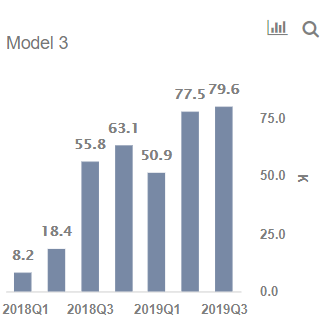

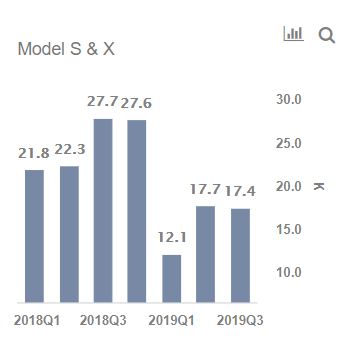

Model 3 Deliveries Grow 3% Sequentially While Model S&X See Declines

- How Will Tesla’s Earnings Trend After A Tough Q1 Delivery Report?

- With Deliveries Falling And Inventory Piling Up, What’s Next For Tesla Stock?

- Down Almost 20% This Year, Is Tesla Stock Good Value?

- Down 9% Year-To Date, Will A Q4 Earnings Beat Drive Tesla Stock Higher?

- With Delivery Growth Cooling, Is Tesla Stock Still A Buy At $250?

- Following A Lackluster Cybertruck Debut, Is Tesla Stock Overvalued At $240?

- Model 3 deliveries saw a 3% sequential improvement, with deliveries standing at 79.6k units.

- The growth is not very encouraging, given that the company now sells variants starting at under $40k before incentives.

- However, Tesla has indicated that it saw record net orders over Q3, with its backlog increasing.

- Model S & X deliveries continued to remain lackluster at 17.4k units, marking a 1.5% sequential decline.

- While Tesla recently lowered the base price and introduction of an upgraded drivetrain and suspension setup on these vehicles, it is likely that they are being impacted by saturation in the premium end of the market and cannibalization by the Model 3.

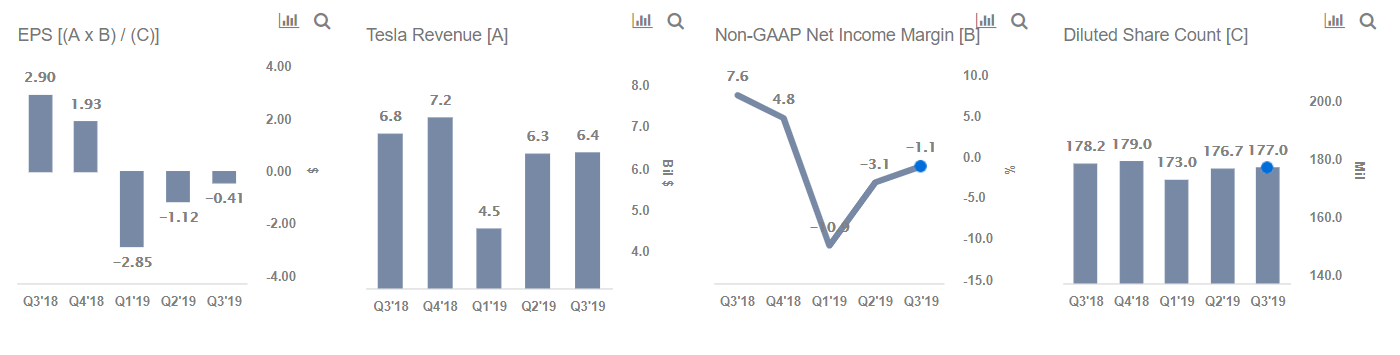

Tesla Automotive Revenues Could Remain Almost Flat, As Delivery Growth Is Offset By Potentially Lower Pricing

- We expect Tesla’s Automotive revenues to remain almost flat at $5.4 billion this quarter.

- While deliveries have grown marginally, we expect average revenue per vehicle to decline, on account of a higher-mix of Model 3s and lower starting prices.

Tesla’s Total Revenues For The Q3 Could Stand At $6.4 Billion

- Other revenues, which include revenues from Tesla’s service operations and renewable energy segment, are expected to stand at close to $1 billion.

- We expect Tesla’s total revenues to stand at about $6.4 billion for the quarter.

Tesla Likely To Remain In The Red Over Q3 As Well

- We expect Tesla’s EPS to remain negative, coming in at about -$0.40 per share over Q3, as it continues to see lower sales of its high-margin premium vehicles while offering lower variants of the Model 3.

- That said, we expect losses to reduce sequentially, driven by slightly higher volumes and also as the company carries out a more aggressive cost-cutting plan.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.