Earnings Review: Tesla Might Have One Too Many Balls Up In The Air

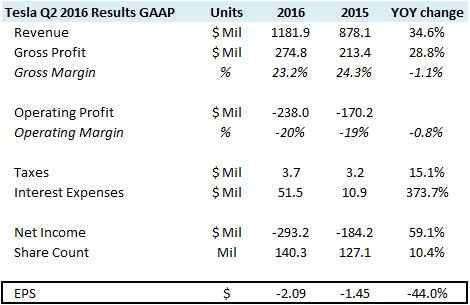

Tesla Motors (NASDAQ: TSLA) reported financial results for the second quarter of fiscal year 2016 on Wednesday, August 3rd. The Silicon Valley based automaker reported a loss of $ 2.09 per share, a 44% decline over last year’s loss of $ 1.45 per share. On an adjusted non-GAAP basis, the company’s earnings per share (EPS) stood at $ 1.29 compared to $ 0.62 from the second quarter of last year. These losses are mostly in line with our expectations.

Over the full quarter, the company produced 18,345 vehicles, an 18% increase over the first quarter and a 43% increase over the second quarter of the previous fiscal year. This was still lower than the company’s guidance at the end of the last quarter after a 30% increase in production for Q2 from 15,500 units to just over 20,000 units. However, according to the company, its production was significantly ramped up towards the end of the quarter and reached close to 2,000 units per week. For the first half of the year, the company delivered close to 30,000 vehicles. If the weekly production rate is already 2,000 units per week, it is possible that the company can achieve its full year production target of 80,000-90,000 vehicles for the full year. However, deliveries are expected to be quite a bit below that.

Something that is extremely important for the company is the build up of lithium ion production to support the volume of pre-orders for the Tesla Model 3. Tesla has already received close to 400,000 pre-orders for the vehicle, which is supposed to be priced around $35,000-$42,000 depending on feature mix. To this end, the company started production at its Nevada Gigafactory, which management says is on pace to produce lithium ion battery capacity of around 35 GigaWatthours by 2018. The acceleration of the Model 3 production target by two years raised Tesla’s need for cash. Its Capital Expenditure is set to go up by 50% in 2016 to $ 2.5 billion. To meet its cash requirements, the company issued equity worth $ 1.7 billion.

- How Will Tesla’s Earnings Trend After A Tough Q1 Delivery Report?

- With Deliveries Falling And Inventory Piling Up, What’s Next For Tesla Stock?

- Down Almost 20% This Year, Is Tesla Stock Good Value?

- Down 9% Year-To Date, Will A Q4 Earnings Beat Drive Tesla Stock Higher?

- With Delivery Growth Cooling, Is Tesla Stock Still A Buy At $250?

- Following A Lackluster Cybertruck Debut, Is Tesla Stock Overvalued At $240?

Towards the end of the quarter, there were two significant pieces of news for Tesla. The first was the announcement of the compay’s intent to acquire sister company Solar City for $ 2.6 billion in Tesla stock. And the second news event was the announcement of a new long term product plan. The jury is still out on the first announcemnt, though there are plenty of detractors. As a manufacturer, installer and finacier of consumer solar installations, Solar City is a business that is even more cash intensive than Tesla’s. Compared to Tesla, which uses 50 cents of cash for every dollar in sales it makes, Solar City uses 6 dollars in cash for every dollar in sale it makes. There is quite a bit of debt on Solar City’s balance sheet and it is undertaking the construction of a $ 750 million manufacturing facility for solar panels. More importantly, any combined offerings that Tesla and Solar City can make, such as a combined solar roof panel with a power storage battery, require a number of things to fall into place, making the plan extremely risky.

While announcing the Tesla Master Plan 2.0, Elon Musk said that the company is on the verge of completing Master Plan 1.0, but strictly speaking this is not true. According to Musk, the first plan was comprised of making an expensive sports to car to fund a more affordable luxury car which would then fund a more affordable mass market electric vehicle. Tesla has managed to accomplish the first two steps but it has yet to complete the most challenging part of the plan, i.e. of making an affordable mass market electric vehicle. Moreover, Tesla has not self-funded the production of subsequent models. It has had to issue new equity to raise cash, taken out debt, including on personal guarantees by Musk himself. While Tesla’s new product plan includes an affordable SUV, an autonomous cargo transport vehicle, a public transport vehicle and a competitor to ride sharing companies like Uber, all of these rest on the falling together of a number of pieces: improvements in autonomous technology, regulatory approval of autonomous driving, a drop in lithium prices, increase in production capacity to support Tesla’s volume and the supply of lithium to support the volume. Given all this, combined with the contentious Solar City acquisition and a plan that pushes Tesla’s fate even further into the future, the risk associated with the company becomes even higher.

Have more questions about auto companies? Click on the links below:

- How Do Automotive Luxury Brands Compare In Their Performance In China?

- How Does GM’s performance vary across geographies?

- How Do Auto Luxury Brands Compare In The US?

- What Is Driving Changes In Ford’s Annual Unit Sales?

- How Much Money Does Ford Make Per Car Sold?

- How Much Has GM Been Investing In Growth Opportunities?

- How Ford’s Unit Pricing Differs Across Geographies?

- How Much Has Ford Been Investing In Growth Opportunities

- Ford’s Overwhelming Dependence On North America

- How Much Profit Does Ford Make Per Unit Sold In Each Geography?

- How Different China Growth Projections Impact Ford’s Bottomline

- How Ford’s Poor Russia Performance Is Obscuring Gains Made In Rest of Europe

- How Careful Targeting of F-Series Sales Helped Ford Boost Its Profits

- How Honda’s Automotive Business Is Faring In Japan

- The Most Significant Trends For Honda Motor Company

- Honda’s Brand Image Is Changing In The U.S.

- How Honda’s Automotive Performance Differs Across Geographies

- How Much Has Honda Been Investing In Growth Opportunities

- How Differing Japan Growth Projections Impact Honda Motor Company

Notes:

1) The purpose of these analyses is to help readers focus on a few important things. We hope such lean communication sparks thinking, and encourages readers to comment and ask questions on the comment section, or email content@trefis.com

2) Figures mentioned are approximate values to help our readers remember the key concepts more intuitively. For precise figures, please refer to our complete analysis for Tesla Motors

See More at Trefis | View Interactive Institutional Research (Powered by Trefis) Get Trefis Technology