Seagate Has Been Outperforming Western Digital, But Is The Tide Turning?

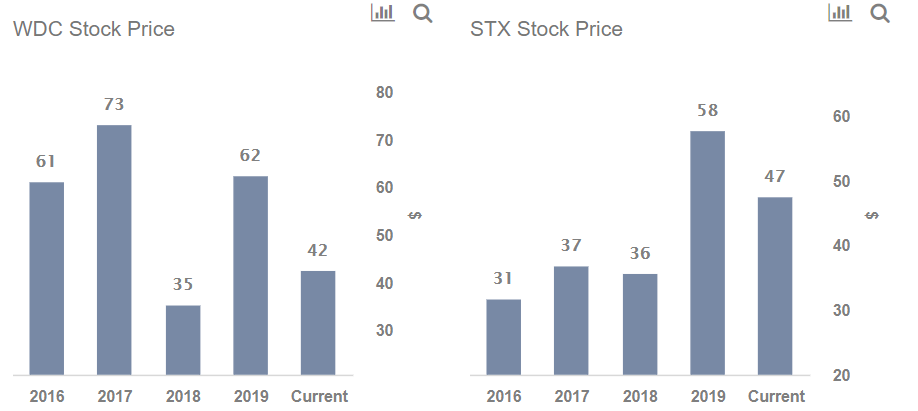

The stock price for Seagate (NASDAQ: STX) is up roughly 27% since the beginning of 2018. In comparison, Western Digital (NASDAQ: WDC) has seen its stock drop by 42%% during the same period. The difference in the stock price growth makes sense when we look at the net margin growth for Seagate, which went from 7.2% in 2017 to 19.4% in 2019. In comparison, Western Digital saw its margins fall from 2.1% in 2017 to -4.6% in 2019, largely due to a drop in gross margins owing to a slump in NAND memory demand.

However, NAND memory demand is back on track, and WDC could see better revenue growth over the next couple of years, especially in FY ’21. So what does this mean? We don’t think the discrepancy in returns for the two stocks will stay the same, and we believe Western Digital is a good investment at the moment compared to Seagate, as investors seek to ride the rally in technology stocks in the current Covid-19 crisis. Companies such as Western Digital and Seagate stand to benefit in the current crisis, as the demand for memory storage devices and platforms is on the rise, given that more people are staying indoors and working from home. Our dashboard, Seagate vs Western Digital: Does The Stock Price Movement Make Sense?, has the underlying numbers.

Western Digital Could Outperform Seagate Over The Next Couple Of Years

- Up 7% This Year, Will Halliburton’s Gains Continue Following Q1 Results?

- Here’s What To Anticipate From UPS’ Q1

- Should You Pick Abbott Stock At $105 After An Upbeat Q1?

- Gap Stock Almost Flat This Year, What’s Next?

- With Smartphone Market Recovering, What To Expect From Qualcomm’s Q2 Results?

- Will United Airlines Stock Continue To See Higher Levels After A 20% Rise Post Upbeat Q1?

Let’s look at both companies a little more closely. Both companies are primarily memory device manufacturers, selling internal and external devices such as hard disk drives, and also pen drives and flash drives in the case of Western Digital.

Seagate has seen a drop of 4% in revenue between 2017 and 2019, but net margins have more than doubled to almost 20% owing to the company’s efforts to cut costs, which saw operating margins rise from 9.8% in 2017 to 14.3% in 2019.

Western Digital saw a drop in revenue of around 13% over the same period, as the semiconductor supply glut of 2018-19 hit the NAND market worse than the DRAM market, harming WDC’s NAND memory device sales (pen drives and flash drives sold under the SanDisk banner). This hurt margins as well, as COGS came in at $13 billion in both 2018 and 2019, but revenues dropped from $20.6 billion to $16.6 billion.

However, with semiconductor and memory demand rising to pre-2019 levels, Western Digital stands to benefit more than Seagate over FY ’20 and 21. For the first 3 quarters of 2020 (fiscal year for both companies ends in June), Western Digital revenues came in at $12.5 billion vs $8 billion for Seagate, with both companies expected to replicate FY 2019 revenue performance, despite a dismal 1H ’20.

Given this, WDC seems a better bet, especially at current valuations, as Western Digital’s P/S ratio currently stands at 0.8x vs 1.25x for Seagate.

Looking for more technology stocks insights? See how Qualcomm could bounce back from the Covid-19 crisis in our interactive dashboard, 20% Gain Possible For Qualcomm Stock Post-Covid? In 2008 It Lost 18% And Then Gained 40%

Our dashboard forecasting U.S. Covid-19 cases with cross-country comparisons analyzes expected recovery time-frames and possible spread of the virus. Further, our dashboard -28% Coronavirus crash vs. 4 Historic crashes builds a complete macro picture.

The complete set of coronavirus impact and timing analyses is available here

See all Trefis Price Estimates and Download Trefis Data here

What’s behind Trefis? See How It’s Powering New Collaboration and What-Ifs For CFOs and Finance Teams | Product, R&D, and Marketing Teams