Bank Stocks Ended 2018 On A Bad Note, Leaving Most Of Them Quite Under-priced

The U.S. equity market started the year 2018 on a strong note, with optimism surrounding the U.S. economy in the wake of the Tax Cuts and Jobs Act fueling the rally that began in late 2017, over the first quarter of the year. While the equity market remained volatile over the second and third quarters as the U.S.-China trade row unfolded, investors maintained their positive outlook till late September – as is evident from the fact that the S&P 500 rose to an all-time high then. But the 10-year bull run that began in early 2009 ended for good in October with a precipitous drop in value across sectors. The key factor behind the decline over the last three months has been the growing fear of a recession given the overall slowdown in economic growth globally, even as the Fed accelerated its rate hike process with four rate hikes in 2018 (as opposed to its original guidance in late 2016 of three rate hikes a year through 2019).

It, then, comes as no surprise that the only two sectors constituting the S&P 500 that reported an increase in value over 2018 were the non-cyclical healthcare and utilities sectors. While the S&P 500 index shrunk by 6.2% over the year, the financial sector fared worse with a decline of almost 15%. More specifically, the banking sector took a bigger hit with the KBW Bank Index falling almost 20% for the year. In comparison, the bank-specific index gained almost 15% in 2017 and nearly 24% in 2016.

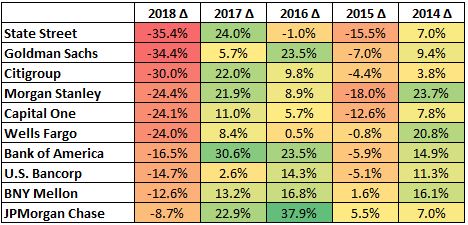

Notably, 6 of the 10 largest U.S. banks saw their share price slide by more than 24% over 2018. While State Street’s shares tanked by more than 35% in the year, Goldman Sachs came in at a close second with a decline of over 34% (making it the worst performer for the year among the 30 constituents of the Dow Jones Industrial Average). On the other hand, JPMorgan Chase fared much better than its peers with a decline of less than 9% in its share price. We detail the changes in share price for the largest U.S. banks over recent years below, while also explaining why we believe these stocks will rally considerably over the coming months.

- Trailing S&P500 By 14% YTD, What To Expect From State Street Stock?

- Down 6% Since The Beginning Of 2023, What Should You Expect From State Street Stock?

- State Street Stock Has A 45% Upside To Its Pre-Inflation Shock

- What To Expect From State Street Stock In Q2?

- State Street Stock Is Undervalued

- Where Is State Street Stock Headed?

See our full analysis for State Street | JPMorgan | Bank of America | U.S. Bancorp | Goldman Sachs

A Quick Summary Of Changes In Share Price For The Largest Banks Over Recent Years

Investor confidence in the banking sector has improved considerably since 2011 despite several obstacles along the way in terms of tightening regulatory requirements, several high-profile scandals, as well as poor internal risk-control frameworks at the largest global banks. While improving economic conditions played a key role in restoring investor confidence in the industry, the banks also put in considerable efforts over 2012-14 to clear their legal backlogs and to strengthen their balance sheet as well as their internal governance systems. With the largest U.S. banks being at a considerably stronger condition than what they were several years ago, the sharp sell-off over recent months definitely cannot be attributed to any weakness in the U.S. banking system as a whole.

The table below summarizes the change in prices for major bank stocks for each of the last five years.

Notably, 2018 was the first time since 2008 when each of the largest U.S. banks saw their share price decline over the year. It must be noted here that the decline in share price for most banks in 2015 can be attributed to the negative impact of near-zero interest rates on the banks’ results. In sharp contrast, 2018 saw the Fed hike interest rates on 4 separate occasions – something that has had a positive impact on the net interest margin (NIM) figure for the U.S. banking industry. But potential losses stemming from a recession in the U.S. economy outweighed these gains in investors’ minds over the last three months of 2018. After all, if the U.S. economy falters in the near future then the banks will see their loan portfolio shrink and also incur sizable losses from loans turning bad.

But Are The Current Levels For These Banks Justified?

A key metric that highlights how undervalued most of the bank stocks are is the price-to-book (P/B) ratio. The P/B ratio compares the share price with the bank’s underlying financial condition (captured by the book value per share), and can indicate whether the shares are being priced too cautiously or too aggressively. Marked differences between the price of a company’s shares compared to its book value are often a sign of under- or over-valuation. That said, it must be remembered that very low P/B ratios may actually be because of problems with the company’s business model, while high P/B ratios could be due to optimism about the future potential of a company’s business model.

The table below highlights the current P/B ratio for the largest U.S. banks, and also includes the average P/B figure for these banks over the last five years.

Notably, the current P/B ratio for four of the banks (State Street, Wells Fargo, Goldman Sachs and U.S. Bancorp) is at least 33 percentage points lower than the average for the last five years. Part of the difference for State Street can be explained by the fact that it is perceived to have overpaid for its acquisition of Charles River last year, and Wells Fargo’s P/B ratio will understandably remain under pressure due to the Fed’s growth restriction on it. But all four of these banks look considerably under-valued when you take into account their historical P/B ratios.

While Bank of America and JPMorgan stand out with a current P/B ratio that is much higher than their 5-year average, it must be remembered that Bank of America has made sizable changes to its business model since 2012 to mitigate the impact of its acquisition of Countrywide. Also, JPMorgan’s significant premium to book value is primarily because of its dominance across banking services ranging from consumer and commercial banking to investment banking as well as custody services, and is justified.

Given the unusually low price-to-book ratio for many of these banks, we expect their share prices to normalize in the near future – reversing most of the losses seen in the last three months.

What’s behind Trefis? See How it’s Powering New Collaboration and What-Ifs

For CFOs and Finance Teams | Product, R&D, and Marketing Teams

Like our charts? Explore example interactive dashboards and create your own.