ConocoPhillips (COP) Dividend Stock Analysis

Submitted by Dividend Growth Investor as part of our contributors program.

ConocoPhillips (COP) Dividend Stock Analysis

ConocoPhillips (COP) explores for, produces, transports, and markets crude oil, natural gas, natural gas liquids, liquefied natural gas and bitumen on a worldwide basis. This dividend achiever has paid dividends since 1934, and has increased them for 12 years in a row.

- Will United Airlines Stock Continue To See Higher Levels After A 20% Rise Post Upbeat Q1?

- Up 8% This Year, Why Is Costco Stock Outperforming?

- Down 7% In A Day, Where Is Travelers Stock Headed?

- What’s Next For Johnson & Johnson Stock After Beating Q1 Earnings?

- Should You Pick UnitedHealth Stock At $480 After A Q1 Beat?

- American Express Stock Is Up 17% YTD, What To Expect From Q1?

Back on May 1, 2012 ConocoPhillips split in two separately traded companies – ConocoPhillips and Phillips 66 (PSX). The data presented below shows the ten year financial trends for legacy ConocoPhillips, as accounting records had not been updated going back 10 years for just ConocoPhillips. ConocoPhillips is the upstream operations, which are involved in exploration and production of oil and natural gas. Phillips 66 represented downstream operations such as operating refineries in US and abroad, as well as transportation assets such as pipelines.

The company’s peer group includes Exxon Mobil (XOM), Chevron (CVX)) and British Petroleum (BP).

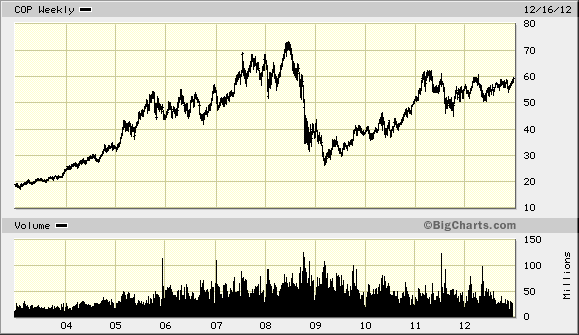

Over the past decade this dividend growth stock has delivered an annualized total return of 15.50% to its shareholders.

(click to enlarge)

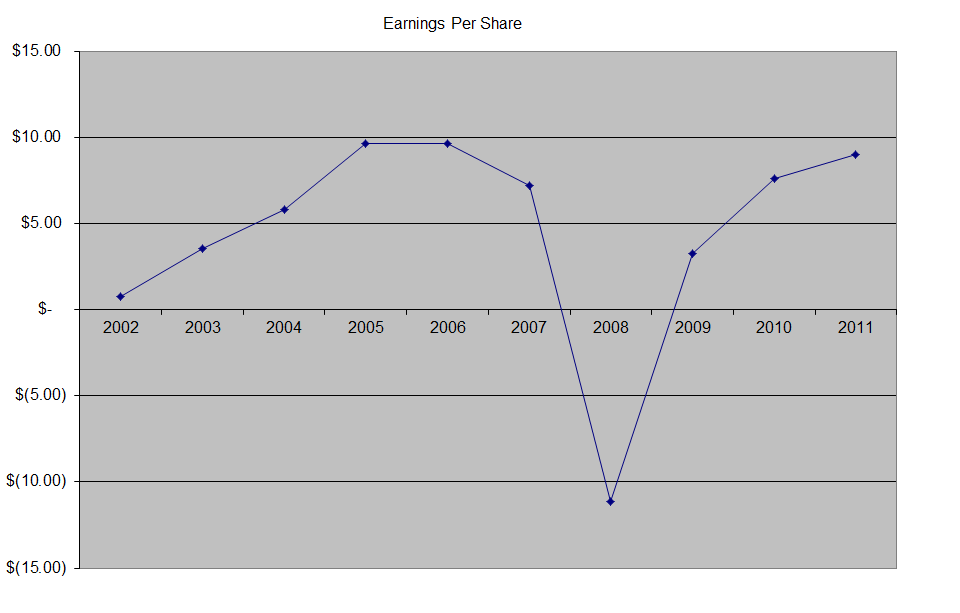

The company has managed to increase EPS from $0.74/share in 2002 to $8.97 by 2011. Analysts expect ConocoPhillips to earn $6.06 per share in 2012 and $6.26 per share in 2013.

(click to enlarge)

ConocoPhillips plans to spend $15 billion per year through 2016. Some of its investments will be in oil rich fields in North America including Bakken Shale, Eagle Ford and Permian Basin. The goal is to reach a reserve replacement ratio of 100%. The nature of the oil business is such, that for every barrel of oil pumped out of the ground, your reserves decrease by one barrel. With advancements in technology however, it is possible to obtain more oil from existing and new wells than before. In addition, oil and gas companies spend large amounts of money on seismic activity studies, in order to increase their chances of striking oil. With the amount of funds spent to achieve a reserve replacement ratio above 100%, the company is also targeting production growth of 3% – 5%/year as well.

Over the past three years, the company has sold off a lot of assets, raising billions of dollars in the process. Examples include selling off its stake in Lukoil, the proceeds from which were used to repurchase stock. Currently, it is in the process of selling off its stake in the Kashagan project in Kazakhstan. ConocoPhillips expects to raise somewhere between $8 – $10 billion through 2013 by the sale of these non-core assets.

The average return on equity has remained around 20% for most of the time, with the exception of the 200 7 -2008 run up in oil prices, followed by the 2008 – 2009 decline. Since then, it has increased back up to 20% in 2011. I generally want to see at least a stable return on equity over time.

(click to enlarge)

The annual dividend payment has increased by 14.20% per year over the past decade, which is lower than the growth in EPS.

A 14% growth in distributions translates into the dividend payment doubling every five years on average. If we look at historical data, going as far back as 1982, one would notice that the company has actually managed to double distributions every ten years on average. Management has expressed willingness to distribute 20% – 25% of cashflows for dividends each year, which should be appealing to income investors.

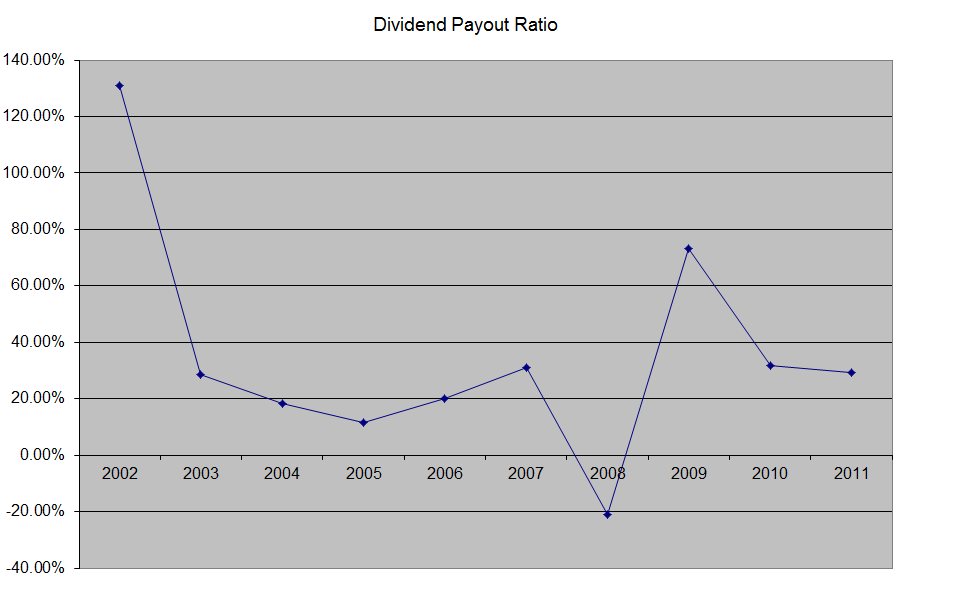

The dividend payout ratio has mostly remained below 50%, with the exception of 2002 and 2008- 2009 periods. A lower payout is always a plus, since it leaves room for consistent dividend growth minimizing the impact of short-term fluctuations in earnings.

(click to enlarge)

Currently ConocoPhillips is attractively valued at 8.10 times earnings, yields 4.40%, and has a sustainable distribution. In comparison Exxon Mobil trades at 9.70 times earnings and yields 2.50%, while Chevron trades at 9.50 times earnings and yields 3.10%. I have recently replacedExxon Mobil with ConocoPhillips.